PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063587

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063587

India Construction Consulting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

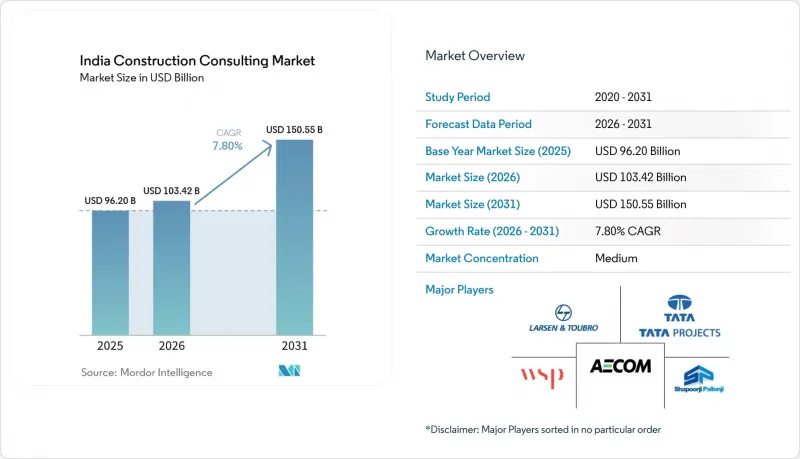

According to Mordor Intelligence, the india construction consulting market size is expected to grow from USD 96.20 billion in 2025 to USD 103.42 billion in 2026 and is forecast to reach USD 150.55 billion by 2031 at 7.80% CAGR over 2026-2031.

This report is Segmented by Service Type (Project Management Consultancy, Feasibility Studies, and More), by Sector (Residential, Commercial, Infrastructure/Civil), by Construction Type (New Construction, Renovation), by Investment Source (Public, Private), and by Geography (Mumbai, Delhi NCR, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Construction Consulting Market Trends and Insights

National Infrastructure Pipeline and Smart Cities push.

Federal allocations worth USD 2,684.82 billion across 14,569 projects have changed consulting from episodic advice to continuous program management. The completion of 7,741 Smart Cities projects and the roll-out of 100 Integrated Command and Control Centers have embedded digital-twin workflows into municipal briefs. The PAIMANA dashboard tracks 1,392 projects valued at USD 418 billion and rewards advisors who deliver live, validated data to city officials. The 2026 Union Budget earmarked USD 36.5 billion for roads and USD 34.5 billion for railways, locking in multi-year deal flow for the India construction consulting market. These factors are concentrating opportunities among full-service firms able to combine engineering, digital, and quality-assurance credentials.

Real Estate Investment Trust and private equity inflows

Private equity inflows rose 38% year-on-year to USD 2.4 billion during the first half of 2025. Brookfield's USD 156.3 billion office acquisition and Blackstone's USD 6 billion data-center pipeline show sustained institutional interest. REIT sponsors mandate third-party project controls, ESG reporting, and IGBC or GRIHA certifications, generating recurring assignments. Mindspace Business Parks alone committed USD 500 million to construction in FY 2026 while targeting 49% renewable energy use, compelling advisors to integrate green metrics from day one. Concentration of capital in Mumbai, Bengaluru, and Delhi NCR leaves secondary cities underserved, offering room for regional firms.

Volatile input costs are squeezing fees.

Steel prices fell 15-20% during 2024-2025, pushing developers to renegotiate and cut consultant margins by roughly 250 basis points. Cement quotes varied by up to 10% quarter-on-quarter in southern states, prompting clients to demand routine value-engineering audits in the Indian construction consulting market. The National Highways Authority of India capped consultant fees at 2.5% of project cost in 2025, down from 3-3.5% earlier, a policy that multiple state agencies have copied. Payment lags extending to 120 days are forcing firms without strong working-capital lines to exit complex infrastructure assignments.

Other drivers and restraints analyzed in the detailed report include:

- Semiconductor and data-center capital expenditure surge

- Digital construction mandates (BIM, Common Data Environment)

- Talent scarcity in certified project management and cost engineers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Project Management Consultancy held 38.5% of India's construction consulting market share in 2025, underpinned by oversight on the 26,425 km Bharatmala highway program and nearly 1,800 km of metro lines. Master Planning and other strategy-led services are on course to register an 8.5% CAGR, reflecting demand for integrated land-use, utilities, and digital twin blueprints across semiconductor corridors and hyperscale data center parks. The India construction consulting market size tied to feasibility studies remains about one-quarter of revenue. Still, basic drafting and quantity surveying are now being automated, squeezing margins. Advisors scale advantage through ISO 19650-compliant Common Data Environment platforms that reduce rework by 20% and lift realization rates on multidisciplinary briefs. Firms without such digital depth are losing share or partnering with software houses to defend positions.

Second-tier cities still rely on AutoCAD deliverables, giving mono-discipline outfits a foothold, yet program-based contracting via the PAIMANA portal is moving national clients toward single-window consortia. AI-driven quantity take-off tools are freeing senior staff for higher-margin dispute-resolution and lender-engineer mandates. As public tenders now require USD 60-120 million in indemnity cover, only well-capitalized firms can afford the premium, leading to a steady rise in concentration in the Indian construction consulting market.

Residential consulting accounted for 37.5% of the India construction consulting market in 2025, underpinned by affordable housing drives and rent-yield REIT platforms. Infrastructure and civil projects are projected to clock the fastest expansion at an 8.6% CAGR through 2031, fueled by USD 36.5 billion for roads and USD 34.5 billion for railways in Budget 2026. Transportation infrastructure remains the largest slice within this bucket, demanding corridor development plans, drone surveys, and AI-based quality control. Energy and utilities work, including solar and transmission corridors, is adding grid integration and battery storage feasibility to the scope. Commercial categories such as office, retail, and logistics account for roughly 30% of revenues, with hyperscale data centers as the star performer.

Data-center consulting pays margins of 30-40% above office work because of stringent Tier III/IV redundancy rules. REIT sponsors are dictating green metrics and stable rental yields, which oblige technical audits each quarter. Retail assignments face online-commerce headwinds yet pivot toward experiential malls that need entertainment and F&B layout choreography, a niche where design thinkers can shine inside the India construction consulting market.

List of Companies Covered in this Report:

- Larsen & Toubro (L&T-Sargent & Lundy / L&T Infra Engg)

- Tata Consulting Engineers

- AECOM India Pvt Ltd

- WSP India

- Shapoorji Pallonji Engineering & Construction

- Afcons Infrastructure Ltd

- Egis India

- Louis Berger (WSP) India

- Ramboll India

- Mott MacDonald India

- Jacobs Engineering India

- RITES Ltd

- Ircon International

- SMEC India

- Nippon Koei India

- Feedback Infra

- Voyants Solutions

- LEA Associates South Asia

- CP Kukreja Architects-PMC

- SGS India (Projects & Construction)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 National Infrastructure Pipeline & Smart-Cities push

- 4.2.2 Digital construction mandates (BIM, CDE)

- 4.2.3 REIT- & PE-backed real-estate wave

- 4.2.4 ESG / green-building compliance demand

- 4.2.5 PPP dispute-resolution reforms boosting Independent Engineers

- 4.2.6 Semiconductor & data-center capex boom

- 4.3 Market Restraints

- 4.3.1 Volatile input costs squeezing fees

- 4.3.2 Fragmented permitting inflating scope creep

- 4.3.3 Talent scarcity in certified PM & cost engineers

- 4.3.4 AI design-automation commoditising basic services

- 4.4 Government Initiatives & Consultant Empanelment Frameworks

- 4.5 Value / Supply-Chain Analysis

- 4.5.1 Overview

- 4.5.2 International Consulting Firms - Key Quantitative and Qualitative Insights

- 4.5.3 Domestic/Regional Consulting Firms - Key Quantitative and Qualitative Insights

- 4.5.4 Specialized Niche Consultants - Key Quantitative and Qualitative Insights

- 4.5.5 Technology Platform Providers (BIM, Digital PMC) - Key Quantitative and Qualitative Insights

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Industry Attractiveness - Porter's Five Force Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Comparison of Consulting Market Maturity: India vs. Other Countries

5 Market Size & Growth Forecasts (Values, In USD Billion)

- 5.1 By Service Type

- 5.1.1 Project Management Consultancy (PMC)

- 5.1.2 Feasibility Studies

- 5.1.3 Detailed Project Reports (DPR)

- 5.1.4 Design and Engineering Services

- 5.1.5 Master Planning and Other Services

- 5.2 By Sector

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.2.1 Office

- 5.2.2.2 Retail

- 5.2.2.3 Industrial and Logistics

- 5.2.2.4 Data Center

- 5.2.2.5 Others - Institutional, Hospitality etc.

- 5.2.3 Infrastructure/Civil

- 5.2.3.1 Transportation Infrastructure (Roadways, Railways, Airways, others)

- 5.2.3.2 Energy & Utilities

- 5.2.3.3 Social Infrastructure

- 5.2.3.4 Others

- 5.3 By Construction Type

- 5.3.1 New Construction

- 5.3.2 Renovation

- 5.4 By Investment Source

- 5.4.1 Public

- 5.4.2 Private

- 5.5 By Geography

- 5.5.1 Mumbai Metropolitan Region

- 5.5.2 Delhi NCR

- 5.5.3 Pune

- 5.5.4 Bengaluru

- 5.5.5 Hyderabad

- 5.5.6 Chennai

- 5.5.7 Kolkata

- 5.5.8 Ahmedabad

- 5.5.9 Rest of India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Larsen & Toubro (L&T-Sargent & Lundy / L&T Infra Engg)

- 6.4.2 Tata Consulting Engineers

- 6.4.3 AECOM India Pvt Ltd

- 6.4.4 WSP India

- 6.4.5 Shapoorji Pallonji Engineering & Construction

- 6.4.6 Afcons Infrastructure Ltd

- 6.4.7 Egis India

- 6.4.8 Louis Berger (WSP) India

- 6.4.9 Ramboll India

- 6.4.10 Mott MacDonald India

- 6.4.11 Jacobs Engineering India

- 6.4.12 RITES Ltd

- 6.4.13 Ircon International

- 6.4.14 SMEC India

- 6.4.15 Nippon Koei India

- 6.4.16 Feedback Infra

- 6.4.17 Voyants Solutions

- 6.4.18 LEA Associates South Asia

- 6.4.19 CP Kukreja Architects-PMC

- 6.4.20 SGS India (Projects & Construction)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment