PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063673

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063673

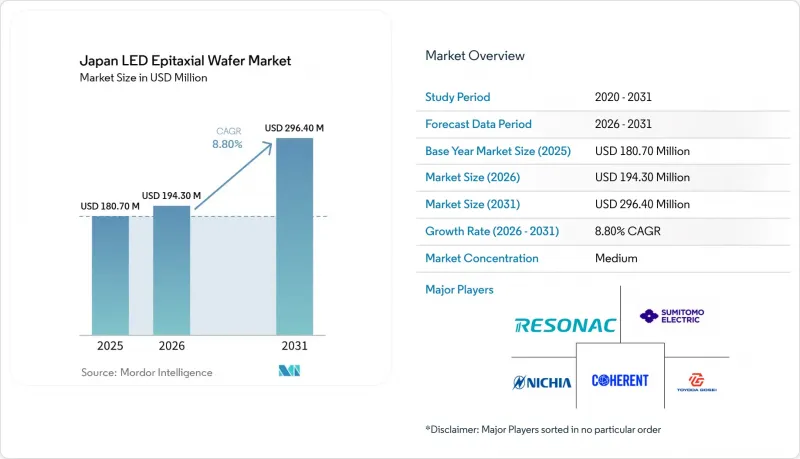

Japan LED Epitaxial Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan lED epitaxial wafer market size is expected to increase from USD 180.7 million in 2025 to USD 194.3 million in 2026 and reach USD 296.4 million by 2031, growing at an 8.80% CAGR over 2026-2031.

This report is Segmented by Material System (GaN-Based Epitaxial Wafers, Alingap Epitaxial Wafers, and More), Substrate Type (Sapphire, Silicon, Silicon Carbide (SiC), and More), Wafer Diameter (Up To 100 Mm, 150 Mm, and More), and Application (General Lighting, Automotive, Displays and Backlighting, UV Sterilization, and More). The Market Forecasts are Provided in Terms of Value (USD).

Japan LED Epitaxial Wafer Market Trends and Insights

Intensifying Demand for High-Brightness LEDs In Automotive Headlamps

Adaptive matrix headlamps require epitaxial layers with sub-1% in-plane wavelength variation to prevent color shift across the beam. Nichia's new automotive innovation center accelerates co-development cycles, giving Japanese suppliers early design-win opportunities.Tier-1 lamp makers validate domestic wafers against stringent PPAP tests, reinforcing long contracts that shield producers from commodity price swings. Silicon substrates improve thermal management inside compact headlamp housings. The growing pixel count per module lifts wafer demand despite price compression in conventional lighting diodes.

Government Incentives for Domestic Compound-Semiconductor Production

A JPY 101.7 billion (USD 0.64 billion) subsidy package, including JPY 70.5 billion (USD 0.44 billion) directed to SiC epi capacity, lowers capital hurdles for MOCVD line upgrades and broadens the precursor supply base. Shared infrastructure, such as bulk gas farms and clean-room expansions, indirectly benefits LED wafer fabs by cutting procurement lead times for NH3 and TMGa. Policy continuity signals a long-range commitment that de-risks private investment in next-generation reactors and metrology.

High Capital Expenditure for New MOCVD Reactors

State-of-the-art MOCVD units cost USD 1.5-3 million each, and domestic plants must retrofit multi-chamber configurations with in-situ metrology, straining balance sheets just as LED ASPs decline. Nichia's impairment of idle cathode tools illustrates the risk of misaligned capex. Smaller wafer houses lacking credit access face consolidation or exit. Equipment vendors' pricing power further limits negotiation room for Japanese buyers.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Penetration of MiniLED Backlighting in High-End TVs

- Surge In UV-C LED Adoption for Sterilization Equipment

- Supply Chain Disruptions for High-Purity NH3 Gas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AlGaN's share remains modest, but its projected 12.50% CAGR reflects heightened demand for sterilization and sensing devices that rely on deep-UV emission. The Japan LED epitaxial wafer market size for GaN remains dominant thanks to general lighting and automotive volumes, yet innovation energy is clearly shifting toward AlGaN, where lifetime gains secure premium margins. Research breakthroughs with 6-inch sapphire templates show only 1.6% variation in emission, confirming manufacturability at scale.

GaN maintains cost and defect-density advantages, but future revenue growth tilts toward AlGaN and niche AlInGaP. Emerging RGB color-conversion paths in micro-LED displays cap direct red AlInGaP demand. Consequently, the Japan LED epitaxial wafer market will likely bifurcate into a cost-sensitive GaN core and a high-margin AlGaN frontier catering to long-life UV applications.

Sapphire's 58.30% 2025 share underscores the inertia of established C-plane recipes and optical transparency. Nevertheless, silicon's superior 150 W m-1 K-1 thermal conductivity and compatibility with existing CMOS lines underpin its projected 12.80% CAGR. Automotive headlamp modules that operate above 150 °C favor GaN-on-Si designs, a shift that enlarges silicon's addressable slice of the Japan LED epitaxial wafer market.

Silicon carbide excels in heat removal at 490 W m-1 K-1, yet 8-inch wafer scarcity and elevated cost slow adoption. Gallium arsenide remains confined to specialty lasers. Consequently, sapphire holds volume leadership in mainstream LEDs, whereas silicon captures fast-growing segments that demand thermally robust, vertically structured chips.

List of Companies Covered in this Report:

- Nichia Corporation

- Toyoda Gosei Co., Ltd.

- Resonac Holdings Corporation

- Sumitomo Electric Industries, Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Sanan Optoelectronics Co., Ltd.

- Epistar Corporation

- Osram Opto Semiconductors GmbH

- Coherent Corp.

- SemiLEDs Corporation

- LG Innotek Co., Ltd.

- AIXTRON SE

- DOWA Electronics Materials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying Demand for High-Brightness LEDs in Automotive Headlamps

- 4.2.2 Government Incentives for Domestic Compound-Semiconductor Production

- 4.2.3 Rapid Penetration of MiniLED Backlighting in High-End TVs

- 4.2.4 Surge in UV-C LED Adoption for Sterilization Equipment

- 4.2.5 Expansion of Smart Manufacturing Lines for MicroLED in Japan

- 4.2.6 Emergence of GaN-on-Si Technology Partnerships with Foundries

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for New MOCVD Reactors

- 4.3.2 Supply Chain Disruptions for High-Purity Ammonia Gas

- 4.3.3 Competition from Low-Cost Chinese Epitaxy Suppliers

- 4.3.4 Limited Availability of 8-inch SiC Substrates

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material System

- 5.1.1 GaN-based Epitaxial Wafers

- 5.1.2 AlInGaP Epitaxial Wafers

- 5.1.3 AlGaN Epitaxial Wafers

- 5.2 By Substrate Type

- 5.2.1 Sapphire

- 5.2.2 Silicon

- 5.2.3 Silicon Carbide (SiC)

- 5.2.4 Gallium Arsenide (GaAs)

- 5.3 By Wafer Diameter

- 5.3.1 Upto 100 mm

- 5.3.2 150 mm

- 5.3.3 200 mm and Above

- 5.4 By Application

- 5.4.1 General Lighting

- 5.4.2 Automotive Lighting

- 5.4.3 Displays and Backlighting

- 5.4.4 UV Sterilization

- 5.4.5 Industrial and Specialty Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Toyoda Gosei Co., Ltd.

- 6.4.3 Resonac Holdings Corporation

- 6.4.4 Sumitomo Electric Industries, Ltd.

- 6.4.5 Shin-Etsu Chemical Co., Ltd.

- 6.4.6 Sanan Optoelectronics Co., Ltd.

- 6.4.7 Epistar Corporation

- 6.4.8 Osram Opto Semiconductors GmbH

- 6.4.9 Coherent Corp.

- 6.4.10 SemiLEDs Corporation

- 6.4.11 LG Innotek Co., Ltd.

- 6.4.12 AIXTRON SE

- 6.4.13 DOWA Electronics Materials

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment