PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063739

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063739

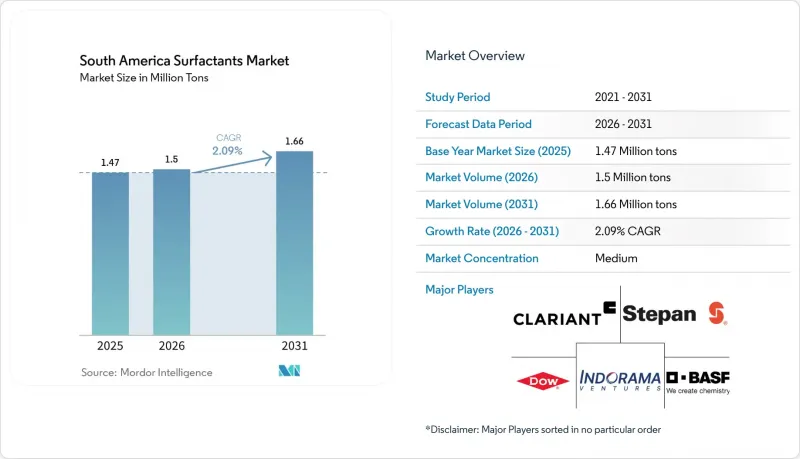

South America Surfactants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america surfactants market size is projected to be 1.47 Million tons in 2025, 1.5 Million tons in 2026, and reach 1.66 Million tons by 2031, growing at a CAGR of 2.09% from 2026 to 2031.

This report is Segmented by Type (Anionic Surfactants, Cationic Surfactants, and More), Origin (Synthetic Surfactants and Bio-Based Surfactants), Application (Household Soaps and Detergents, Personal Care, Institutional and Industrial Cleaning, and More), and Geography (Brazil, Argentina, Chile, Colombia, Peru, and Rest of South America). The Market Forecasts are Provided in Volume (Tons).

South America Surfactants Market Trends and Insights

Growing Personal- and Home-Care Consumption Boom

Latin America's cosmetics and personal-care sales totaled USD 24.74 billion in 2024, with Brazil alone contributing USD 9.83 billion. This growth highlights a shift toward premium products, such as liquid body washes and shampoos, over traditional bar soaps. Mild amphoteric surfactants like cocamidopropyl betaine command a 30-50% price premium over commodity LAS, ensuring price stability even amid fluctuations in crude-derived feedstock costs. Brazil's liquid laundry detergent retail value reached USD 697.81 million in 2024, driven by urban adoption of front-loading washing machines that favor alcohol ethoxylate and Alcohol Ethoxy Sulfate (AES) systems. In Argentina, powder detergents remain dominant due to high inflation limiting appliance upgrades. Colombia and Peru exhibit mixed adoption of detergent formats across urban and rural areas, complicating distributor inventory management.

Accelerating Agrochemical Capacity Additions

Brazil's pesticide-treated cropland expanded by 6.1% between 2023 and 2024, reaching 85 million hectares. BRANDT Consolidated invested USD 15 million in an adjuvant plant in Rondonopolis to supply alcohol-ethoxylate blends for soybean and corn crops. Argentine formulators depend on imports due to delayed greenfield investments, but revised spray-drift guidelines are driving demand for low-foam, high-temperature-stable nonionics. Brazilian regulators plan to phase out alkylphenol ethoxylates in crop-protection products by 2027, shifting demand toward fatty-amine ethoxylates and alcohol ethoxylates that meet ISO 14001 standards.

Tightening APEO and Phosphorus Effluent Laws

Brazil's Conselho Nacional do Meio Ambiente (CONAMA), 498/2024 limits industrial effluent alkylphenol content to 10 µg/L and restricts detergent nonylphenol ethoxylate (NPE) to 0.1% by mass starting January 2027. Argentina has added PFAS compounds to its POPs inventory and will ban PFAS-containing surfactants in firefighting foams by December 2026. Reformulating to alcohol ethoxylates and amine oxides increases raw material costs by 8%-12%, a challenge for tender-driven institutional channels.

Other drivers and restraints analyzed in the detailed report include:

- Bio-Based Surfactants Favored by Oleochemical Feedstock Growth

- Lithium-Ore Flotation Chemicals Demand Spike

- Crude-Oil Price Volatility Hitting LAB Feedstock

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anionic surfactants accounted for 46.85% of 2025 volume, with LAS dominating due to its prevalence in powder detergents. AES and AOS contributed additional volume through liquid detergent and shampoo applications. LAS price volatility, linked to kerosene-derived linear alkylbenzene, is prompting a shift toward MES in Brazil's Northeast, where localized oleochemical feedstocks narrow cost differences to less than USD 100/t compared to LAS. Specialty sub-segments, such as secondary alkane sulfonates in lithium flotation and sulfosuccinates in ultra-mild cleansers, offer niche but profitable opportunities.

Amphoteric surfactants and other types are projected to grow at a 3.05% CAGR through 2031, driven by personal-care brands emphasizing mildness and the phase-out of APEO co-surfactants by 2027. Nonionics, primarily alcohol ethoxylates, are transitioning from alkylphenol ethoxylates to straight-chain C12-C14 alcohol ethoxylates derived from Brazil's oleochemical industry. Regulatory pressures and premiumization trends are gradually reshaping the South America surfactants market by type.

List of Companies Covered in this Report:

- BASF

- Braskem SA

- Clariant

- Croda International plc

- Deten Quimica S.A.

- Dow

- Evonik Industries AG

- Godrej Industries

- Indorama Ventures Public Company Limited

- Innospec

- Kao Corporation

- Lonza

- Nouryon

- P&G Chemicals

- Sasol

- Solvay

- Stepan Company

- TENSAC

- YPF

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing personal and home-care consumption boom

- 4.2.2 Accelerating agrochemical capacity additions

- 4.2.3 Bio-based surfactants favoured by oleochemical feedstock growth

- 4.2.4 Lithium-ore flotation chemicals demand spike

- 4.2.5 Brazilian "green-chem" tax incentives

- 4.3 Market Restraints

- 4.3.1 Tightening APEO and phosphorus effluent laws

- 4.3.2 Crude-oil price volatility hitting LAB feedstock

- 4.3.3 Regional macro-economic instability

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Anionic Surfactants

- 5.1.1.1 Linear Alkylbenzene Sulfonate (LAS or LABS)

- 5.1.1.2 Alcohol Ethoxy Sulfate (AES)

- 5.1.1.3 Alpha-Olefin Sulfonate (AOS)

- 5.1.1.4 Secondary Alkane Sulfonate (SAS)

- 5.1.1.5 Methyl Ester Sulfonate (MES)

- 5.1.1.6 Sulfosuccinates

- 5.1.1.7 Other Anionic Surfactants

- 5.1.2 Cationic Surfactants

- 5.1.2.1 Quaternary Ammonium Compounds

- 5.1.2.2 Other Cationic Surfactants

- 5.1.3 Non-ionic Surfactants

- 5.1.3.1 Alcohol Ethoxylates

- 5.1.3.2 Ethoxylated Alkyl-phenols

- 5.1.3.3 Fatty Acid Esters

- 5.1.3.4 Other Non-ionic Surfactants

- 5.1.4 Amphoteric and Other Types

- 5.1.1 Anionic Surfactants

- 5.2 By Origin

- 5.2.1 Synthetic Surfactants

- 5.2.2 Bio-based Surfactants

- 5.3 By Application

- 5.3.1 Household Soaps and Detergents

- 5.3.2 Personal Care

- 5.3.3 Institutional and Industrial Cleaning

- 5.3.4 Oilfield Chemicals

- 5.3.5 Lubricants and Fuel Additives

- 5.3.6 Agricultural Chemicals

- 5.3.7 Food Processing

- 5.3.8 Textile Processing

- 5.3.9 Other Applications

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Braskem SA

- 6.4.3 Clariant

- 6.4.4 Croda International plc

- 6.4.5 Deten Quimica S.A.

- 6.4.6 Dow

- 6.4.7 Evonik Industries AG

- 6.4.8 Godrej Industries

- 6.4.9 Indorama Ventures Public Company Limited

- 6.4.10 Innospec

- 6.4.11 Kao Corporation

- 6.4.12 Lonza

- 6.4.13 Nouryon

- 6.4.14 P&G Chemicals

- 6.4.15 Sasol

- 6.4.16 Solvay

- 6.4.17 Stepan Company

- 6.4.18 TENSAC

- 6.4.19 YPF

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment