PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063741

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063741

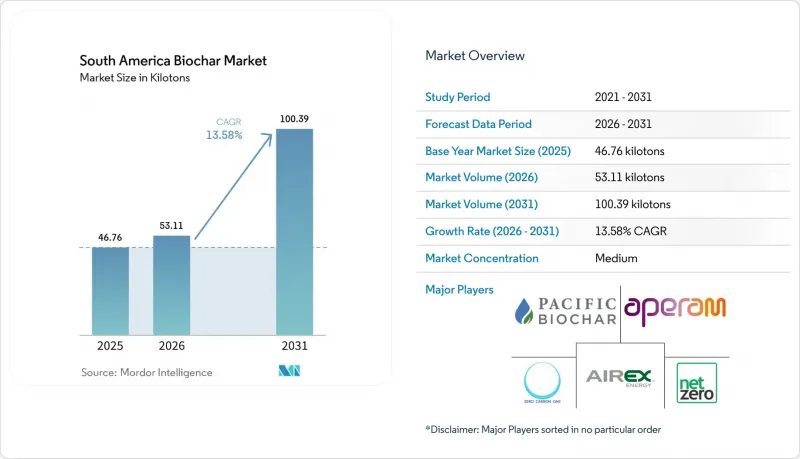

South America Biochar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america biochar market size was valued at 46.76 kilotons in 2025 and is estimated to grow from 53.11 kilotons in 2026 to reach 100.39 kilotons by 2031, at a CAGR of 13.58% during the forecast period (2026-2031).

This report is Segmented by Technology (Pyrolysis, Gasification Systems, and Other Technologies), Application (Agriculture, Animal Farming, Industrial Uses, and Other Applications), and Geography (Brazil, Argentina, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons).

South America Biochar Market Trends and Insights

Agricultural Soil-Fertility Improvement Demand

Tropical soils are acidic and low in cation-exchange capacity, hampering nutrient availability for soybean, maize, and coffee. Field trials showed that 5-10% biochar by volume raised Agave sisalana biomass by 60% in Brazil, while sugarcane-bagasse biochar lifted soil pH by up to 0.7 units and cut lime use by 40%. Coffee-husk biochar retained 25% more water in sandy soils, easing drought stress during Arabica flowering. With prices of USD 700-1,200 per ton, biochar competes with imported NPK when amortized across three seasons of nutrient-use savings. Brazil's Ministry of Development formed Study Commission 328 in 2024 to draft national pyrogenic-biocarbon standards, signaling policy readiness for scale.

Carbon Credits and Emerging Voluntary Carbon Markets

Biochar offsets command premiums because carbon remains stable for millennia. Puro.earth's CORCHAR index valued credits at R$600-1,000 (USD 120-200) in 2025, far above European allowance prices. Exomad Green's 1.24-million-ton contract with Microsoft priced removals near USD 200-250, financing a doubled Bolivian capacity. Altitude and Empacar's 1-million-ton deal in 2026 confirms rising corporate appetite for measurable, reportable, verifiable (MRV) carbon storage. Verra's VM0044 issuance of 161,507 CORCs to Aperam BioEnergia proves that industrial-scale biochar projects can monetize carbon while supplying agronomic markets.

Insufficient Regional Production Capacity and Fragmented Supply Chain

NetZero and Exomad Green together supply 60% of regional output, leaving many areas without commercial product within 300 km. Batch kilns in Colombia's Santander department turn out just 200-500 kg a week, while Argentina's rice-straw project remains pilot-scale. Transporting low-density biochar erodes margins, so farmers beyond 100 km rarely adopt. Fewer than 2% of Brazil's 6 million-ton charcoal sector meets agronomic-grade standards, delaying penetration.

Other drivers and restraints analyzed in the detailed report include:

- Adoption in Livestock Feed Additives for Methane Reduction

- Government Incentives for Sustainable Waste Management

- High Capital and Operating Costs of Advanced Pyrolysis Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pyrolysis supplied 73.37% of 2025 volume and is forecast to grow at a 15.96% CAGR through 2031, underpinning the South America biochar market size leadership through 2031. Slow pyrolysis at 300-400 °C leverages longer residence times to sustain functional groups that improve cation exchange, while fast modes at 600-700 °C increase carbon permanence for credit generation. NetZero's Gen2 units run 20-40-minute cycles at 450-550 °C and capture syngas for onsite heat, lowering cash operating costs. Gasification remains secondary because char yields are just 10-20% of feedstock mass, and other pathways such as hydrothermal carbonization are still pilot level. Verra's forthcoming VM0044 v2 will allow modular 500-2,000 ton systems into credit schemes, potentially unlocking mid-scale adoption and diversifying the South America biochar industry.

Demand for pyrolysis equipment stretches from municipal waste managers to mining firms. Brazil's Eco.Invest loans now cover reactor purchases that process coffee husks during off-season months. University groups adapt low-cost nested-drum kilns for acai seeds, giving cooperatives a USD 150 entry price at the expense of MRV precision. Equipment suppliers that integrate data loggers, cyclone gas cleaning, and condensate recovery may capture higher margins as buyers seek dual revenue from biochar sales and electricity.

List of Companies Covered in this Report:

- Airex Energy

- Aperam BioEnergia

- Biochar Solutions Inc.

- Blackwood Technology

- Carbo Culture

- Carbon Gold

- Diacarbon Energy Inc.

- NetZero

- Nova Analytics Biochar

- Pacific Biochar Benefit Corporation

- ZeroCarbon One

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Agricultural soil-fertility improvement demand

- 4.2.2 Carbon credits and emerging voluntary carbon markets

- 4.2.3 Adoption in livestock feed additives for methane reduction

- 4.2.4 Government incentives for sustainable waste management

- 4.2.5 Mining-tailings rehabilitation using biochar blends

- 4.3 Market Restraints

- 4.3.1 Insufficient regional production capacity and fragmented supply chain

- 4.3.2 High capital and operating costs of advanced pyrolysis units

- 4.3.3 Variable biochar quality causing inconsistent agronomic results

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Technology

- 5.1.1 Pyrolysis

- 5.1.2 Gasification Systems

- 5.1.3 Other Technologies

- 5.2 By Application

- 5.2.1 Animal Farming

- 5.2.2 Agriculture

- 5.2.3 Industrial Uses

- 5.2.4 Others Applications

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Airex Energy

- 6.4.2 Aperam BioEnergia

- 6.4.3 Biochar Solutions Inc.

- 6.4.4 Blackwood Technology

- 6.4.5 Carbo Culture

- 6.4.6 Carbon Gold

- 6.4.7 Diacarbon Energy Inc.

- 6.4.8 NetZero

- 6.4.9 Nova Analytics Biochar

- 6.4.10 Pacific Biochar Benefit Corporation

- 6.4.11 ZeroCarbon One

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Rapid Urbanization and Industrialization

- 7.3 Rising Demand for Renewable Energy and Carbon-Negative Materials