PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063822

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063822

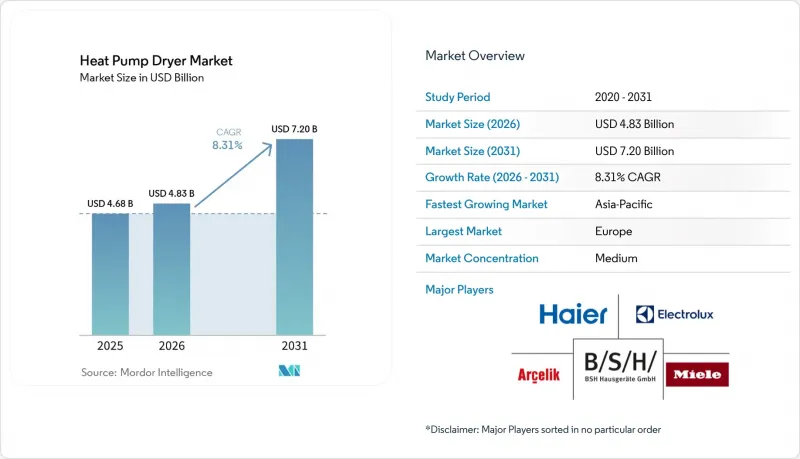

Heat Pump Dryer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the global heat pump dryer market size is expected to increase from USD 4.68 billion in 2025 to USD 4.83 billion in 2026 and reach USD 7.20 billion by 2031, growing at a CAGR of 8.31% over 2026-2031.

This report is Segmented by Product Type (Condenser, Vented, Integrated), Capacity (≤8 Kg, 9-10 Kg, ≥11 Kg), End User (Residential, Commercial, Industrial), Distribution Channel (B2C/Retail, B2B/Direct), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Heat Pump Dryer Market Trends and Insights

Efficiency Mandates and Labeling Accelerate Heat-Pump Adoption

From July 1, 2025, only tumble dryers using heat pump technology may be placed on the EU market, eliminating vented electric and resistance-heated condenser alternatives and channeling R&D toward high-efficiency, closed-loop drying system designs. The EU also rescaled labels to an A-G range that preserves the top classes for the most efficient models, resets shopper expectations, and improves signaling at the point of sale across the global heat pump dryer market. In the United States, the Department of Energy's direct final rule sets a March 1, 2028, compliance date with combined energy factor thresholds that pull lagging standard electric and compact ventless models toward heat pump or hybrid configurations, thereby supporting a low-carbon footprint at fleet scale. ENERGY STAR's draft version 2.0 specification proposes CEF thresholds above DOE minimums and a cycle time cap, making high-CEF, Energy-efficient dryer platforms the credible path to premium labeling and retailer prominence. Safety standards in IEC 60335-2-11:2024 define requirements for appliances using flammable refrigerants, including detection, tightness, and remote operation provisions, enabling broader use of R290 while protecting household environments in the global heat pump dryer market.

Utility Rebates and Incentives Shorten Payback

Point-of-sale rebates for ENERGY STAR-certified heat pump clothes dryers apply discounts directly at checkout, reducing decision friction and turning long-run savings into immediate price parity for a wide range of households in the global heat pump dryer market. State programs that permit do-it-yourself installation for electric-to-electric replacements expand eligibility and cut labor overhead, speeding adoption of ventless convenience where building conditions allow. Georgia's program adds a DIY pathway and wiring or panel allowances, which helps households with older electrical infrastructure reach energy-efficient dryer price points after incentives. Utility rebates from providers like Minnesota Power and DTE Energy stack with federal benefits, raising the combined value and broadening the pool of buyers who can switch to heat pumps without budget tension in the global heat pump dryer market. Multifamily-oriented programs, such as SMUD's incentives for gas-to-electric conversions, directly target shared laundry rooms and property portfolios, helping institutional owners standardize green technology and reduce operating costs.

Higher Upfront Price Versus Vented/Condenser Units

Initial price premiums versus vented or resistance-heated condenser dryers remain a barrier for cost-sensitive households, even as lifecycle savings and rebates narrow gaps in many regions of the global heat pump dryer market. Point-of-sale rebates and utility incentives that stack with federal programs convert long-term savings into on-receipt discounts for qualifying buyers, which raises the addressable base for Energy-efficient dryer adoption. Commercial buyers also weigh capital budgets and throughput needs against operating savings, which can defer replacements to coordinated budget windows. As more brands deliver value configurations that preserve core efficiency while trimming extras, the premium narrows further, and adoption improves across income tiers in the global heat pump dryer market.

Other drivers and restraints analyzed in the detailed report include:

- Urban Multifamily Housing Constraints Favor Ventless Dryers

- OEM Innovation Improves Cycle Time, Noise, and Reliability

- Longer Average Cycle Times in Certain Conditions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Condenser heat pump dryers held 76.91% of the global heat pump dryer market share in 2025, and the segment continues to lead due to a closed-loop drying system that simplifies retrofits and supports ventless convenience in a wide range of dwellings. With heat pump technology now the regulatory baseline in the European Union and the clear premium pathway in North America, leading brands feature auto-cleaning condensers, inverter compressors, and app-connected controls as standard, which aligns with Energy-efficient dryer expectations. Vented heat pump models remain a niche as energy labels and building practices across major regions reward closed-loop efficiency and condensation performance, directing shelf space and incentives toward condenser configurations.

Integrated (built-in) models are the fastest-growing type through 2031. They are projected to grow at a 8.72% CAGR as premium buyers align around sensor-based drying, moisture sensors, and hybrid drying systems that improve performance without compromising aesthetics. The global heat pump dryer market is moving toward portfolio convergence, with condenser and integrated lines sharing compressors, sensors, and control boards, while differentiation centers on finish quality, installation complexity, and acoustic targets. European Union labels set a clear bar, and ENERGY STAR's proposed criteria refine the United States' premium thresholds, together making efficiency achievements visible at retail and online. As a result, the global heat pump dryer market relies more on user experience, Fabric protection, and lifecycle service capabilities to differentiate beyond core efficiency claims.

The 9-10 kg bracket captured 42.83% of the global heat pump dryer market in 2025, reflecting the core demand for standard alcove fit, balanced throughput, and fabric protection for typical household loads under ventless convenience. With A-G labeling in the European Union and a rising share of ENERGY STAR-certified products in North America, this capacity range often delivers top performance without imposing space or power burdens, thereby sustaining its central role across the global heat pump dryer market. Compact ≤8 kg dryers and washer dryer combos play a key role in apartments and secondary units where 120V operation and small footprints outweigh maximum capacity. Across sizes, AI controls, and Hybrid Drying Systems are compressing cycles while keeping temperature envelopes gentle, preserving textiles, and increasing real-world satisfaction.

Large-format units rated ≥11 kg are the fastest-growing capacity group, projected to grow at a 8.41% CAGR, as North American households and light commercial users aim to process bulky bedding and high-volume mixed loads without extending total time on task. Inverter speed control reduces the warm-up penalty, and enhanced Moisture Sensors help prevent over-drying even when drum fullness varies, supporting efficiency and fabric protection. The 9-10 kg range remains the center of gravity for the global heat pump dryer market because it pairs top label outcomes with available space constraints, while compact models sustain penetration in buildings that cannot accommodate larger cutouts or power changes. This three-lane capacity structure underpins steady growth in the global heat pump dryer market through 2031.

Geography Analysis

Europe accounted for 44.93% of global revenues in 2025, underscoring the region's role as an early mover on ecodesign and labeling rules that direct the product mix of the global heat pump dryer market toward A-class, closed-loop drying System designs. Regulation (European Union) 2023/2533 and the rescaled A-G label, effective July 1, 2025, set explicit floors and clear consumer cues, which lift the share of energy-efficient dryer products on retail floors and e-commerce listings. With standards harmonization under International Electrotechnical Commission (IEC) 60335 2 11:2024 enabling R290 adoption and clarifying detection and tightness requirements, European manufacturers align refrigerant choices with safety while pursuing a low carbon footprint.

Asia-Pacific is the fastest-growing region, with a projected 9.57% CAGR, as policy frameworks and urban housing realities converge on compact, ventless convenience platforms across the global heat pump dryer market. Japan's TopRunner approach and South Korea's efficiency schemes continue to push domestic champions to release high-performing, Sensor-Based Drying products, often debuting domestically before wider rollout. Vertical integration in China speeds cost curve improvements and supports broader access to Energy-efficient dryer options, which then influence global pricing and feature expectations. With urban density shaping alcove standards and consumer expectations, capacities in the 7-10 kilogram band coupled with advanced moisture sensors help Asia-Pacific buyers match fabric protection to smaller spaces in the global heat pump dryer market.

North America's growth path is defined by the harmonization of federal standards by March 1, 2028, expanding availability of 120V and combo platforms, and the execution of stacked incentive programs that bring energy-efficient dryer models to price parity for qualifying households in the global heat pump dryer market. ENERGY STAR's proposed criteria point premium buyers to high-Combined Energy Factor (CEF) products with cycle time caps, which guides retail stocking and online merchandising. State programs with point-of-sale rebates and DIY options for electric-to-electric swaps increase reach in older housing without full panel work, and compact combos unlock in unit laundry for many apartments. These elements provide durable catalysts for the global heat pump dryer market over the forecast window.

- BSH Hausgerate GmbH (Bosch, Siemens)

- Electrolux Group (Electrolux, AEG, Zanussi)

- Haier Smart Home (Haier, Candy, Hoover, GE Appliances)

- LG Electronics

- Samsung Electronics

- Whirlpool Corporation (incl. Indesit, Maytag, Hotpoint brands where applicable)

- Miele & Cie. KG

- Beko (Arcelik A.S.) / Grundig

- Gorenje (Hisense Europe) / Hisense

- Fisher & Paykel

- ASKO Appliances

- GE Appliances

- Electrolux Professional

- Alliance Laundry Systems (Speed Queen, Huebsch)

- Girbau

- Panasonic

- Vestel (selected OEM/brands)

- Smeg S.p.A.

- Candy Hoover Group S.r.l.

- Midea Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Efficiency mandates and labeling accelerate heat-pump adoption

- 4.2.2 Utility rebates and incentives shorten payback

- 4.2.3 Urban multifamily housing constraints favor ventless dryers

- 4.2.4 OEM innovation improves cycle time, noise, and reliability

- 4.2.5 Premium-to-mid price migration expands addressable base

- 4.2.6 Commercial laundry electrification and ESG targets

- 4.3 Market Restraints

- 4.3.1 Higher upfront price versus vented/condenser units

- 4.3.2 Longer average cycle times in certain conditions

- 4.3.3 Refrigerant transition (R290) adds redesign/certification burden

- 4.3.4 Electrical capacity limits in older buildings slow retrofits

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Insights Into The Latest Trends And Innovations in the Industry

- 4.7 Insights On Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, Etc.) In The Industry

- 4.8 Insights on Regulatory Framework and Energy-Efficiency Standards in Key Geographies

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Condenser Heat Pump Dryers

- 5.1.2 Vented Heat Pump Dryers

- 5.1.3 Integrated (Built-in) Heat Pump Dryers

- 5.2 By Capacity

- 5.2.1 <= 8 kg

- 5.2.2 9-10 kg

- 5.2.3 >= 11 kg

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial (Laundromats, Hospitality, Healthcare, Multi-housing)

- 5.3.3 Industrial (Light-Duty Laundry/Process Where Applicable)

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail Channels

- 5.4.1.1 Multi-brand Stores

- 5.4.1.2 Exclusive Brand Outlets

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B/Direct Sales

- 5.4.1 B2C/Retail Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East And Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East And Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 BSH Hausgerate GmbH (Bosch, Siemens)

- 6.4.2 Electrolux Group (Electrolux, AEG, Zanussi)

- 6.4.3 Haier Smart Home (Haier, Candy, Hoover, GE Appliances)

- 6.4.4 LG Electronics

- 6.4.5 Samsung Electronics

- 6.4.6 Whirlpool Corporation (incl. Indesit, Maytag, Hotpoint brands where applicable)

- 6.4.7 Miele & Cie. KG

- 6.4.8 Beko (Arcelik A.S.) / Grundig

- 6.4.9 Gorenje (Hisense Europe) / Hisense

- 6.4.10 Fisher & Paykel

- 6.4.11 ASKO Appliances

- 6.4.12 GE Appliances

- 6.4.13 Electrolux Professional

- 6.4.14 Alliance Laundry Systems (Speed Queen, Huebsch)

- 6.4.15 Girbau

- 6.4.16 Panasonic

- 6.4.17 Vestel (selected OEM/brands)

- 6.4.18 Smeg S.p.A.

- 6.4.19 Candy Hoover Group S.r.l.

- 6.4.20 Midea Group

7 Market Opportunities & Future Outlook

- 7.1 120V compact heat-pump dryers for North American retrofits (no panel upgrade)

- 7.2 Commercial heat-pump retrofits in multi-housing and hospitality with utility co-financing