PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071382

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071382

Heat Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

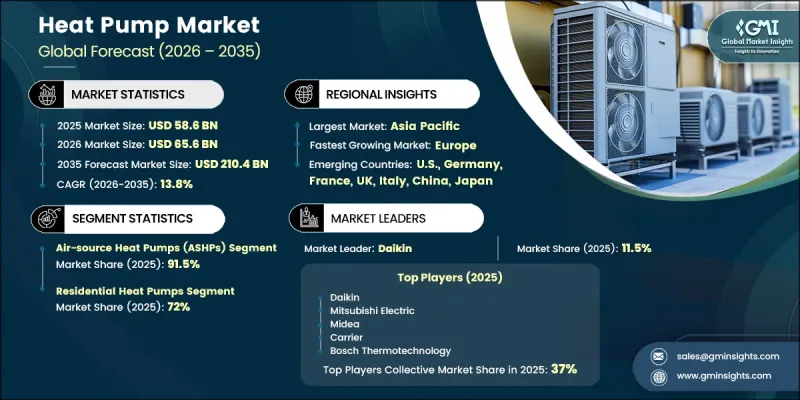

The Global Heat Pump Market generated USD 58.6 billion in 2025 and is estimated to grow at a CAGR of 13.8% to reach USD 210.4 billion by 2035.

Market expansion is fueled by increasingly stringent carbon reduction targets, rising concerns regarding energy affordability and supply security, and continuous advancements in heat pump efficiency. Governments across North America, Europe, and Asia Pacific are promoting building electrification through regulatory frameworks and energy-efficiency initiatives, creating a favorable environment for heat pump adoption. Technological progress in inverter-based and variable-speed compressor systems has significantly improved performance in colder climates, enabling reliable operation in regions that were previously considered unsuitable for heat pump deployment. Enhanced energy performance standards and stricter building regulations are accelerating replacement cycles for conventional heating systems. In addition, growing awareness of sustainable heating and cooling solutions, combined with ongoing investments in residential, commercial, and institutional infrastructure, is supporting long-term market growth. The industry continues to benefit from the transition toward electrified buildings, making heat pumps an increasingly preferred solution for efficient climate control across diverse geographic markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $58.6 Billion |

| Forecast Value | $210.4 Billion |

| CAGR | 13.8% |

Air-source heat pumps segment held a 91.5% share in 2025 and projected to grow at a CAGR of 14.4% through 2035, the highest growth rate among all product segments. The strong market position of air-source systems is attributed to their lower installation costs compared to alternative technologies, broad compatibility with existing building infrastructure, and simplified deployment requirements. Their ability to deliver efficient heating and cooling without extensive site preparation continues to support widespread adoption across residential and commercial applications.

The commercial applications segment held a 25.5% share in 2025 and is forecast to grow at a CAGR of 13.7% during 2026-2035. Demand within this segment is being driven by increasing focus on operational energy efficiency, sustainability objectives, and compliance with environmental performance targets. Businesses are increasingly integrating heat pump technologies with advanced building energy management systems and renewable energy installations to optimize energy consumption and reduce long-term operating expenses.

North America Heat Pump Market accounted for 18.5% share in 2025 and is expected to grow at a CAGR of 8.7% through 2035. The region continues to benefit from growing adoption of energy-efficient heating solutions, expanding electrification initiatives, and increasing penetration of advanced compressor technologies across residential and commercial buildings. Rising consumer awareness, supportive policy frameworks, and continued modernization of heating infrastructure are contributing to sustained market development throughout the region.

Key participants operating in the global heat pump market include Panasonic Corporation, Samsung, Trane, Carrier, Johnson Controls, LG Electronics, Bosch Thermotechnology Corp., Daikin Industries, Ltd., Mitsubishi Electric Corporation, and Midea. Companies operating in the heat pump market are strengthening their competitive positions through continuous investment in product innovation, energy-efficiency enhancements, and expansion of smart connectivity capabilities. Manufacturers are focusing on developing advanced inverter-driven systems, improving cold-climate performance, and integrating digital monitoring features to enhance user experience and system efficiency. Strategic partnerships with distributors, installers, and construction firms are helping companies expand market reach and improve customer access. Businesses are also increasing investments in regional manufacturing facilities and supply chain optimization to improve delivery capabilities and reduce costs. In addition, market participants are expanding their presence in emerging economies, introducing environmentally friendly refrigerants, and aligning product portfolios with evolving energy-efficiency regulations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Supply chain resilience & risk factors

- 3.1.3 Distribution network analysis

- 3.2 Regulatory landscape

- 3.2.1 North America

- 3.2.2 Europe

- 3.2.3 Asia Pacific

- 3.2.4 Middle East & Africa

- 3.2.5 Latin America

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of heat pumps (Solution Core)

- 3.8 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.8.1 By product (Driven by Primary Research)

- 3.8.2 By region (Driven by Primary Research)

- 3.9 Impact of AI & Generative AI on the market (Solution Core)

- 3.9.1 AI-Driven production optimization (Solution Core)

- 3.9.2 Predictive maintenance & fault detection (Solution Core)

- 3.10 Emerging opportunities & trends

- 3.11 Investment analysis & future prospects

- 3.12 Sustainability initiatives & industry 4.0 integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Key developments

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive positioning matrix

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 Air source

- 5.3 Ground source

- 5.4 Water source

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Austria

- 7.3.2 Norway

- 7.3.3 Denmark

- 7.3.4 Finland

- 7.3.5 France

- 7.3.6 Germany

- 7.3.7 Italy

- 7.3.8 Switzerland

- 7.3.9 Spain

- 7.3.10 Sweden

- 7.3.11 UK

- 7.3.12 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 Australia

- 7.4.4 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 Turkey

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 Bosch Thermotechnology Corp.

- 8.2 Carrier

- 8.3 DAIKIN INDUSTRIES, Ltd.

- 8.4 Finn Geotherm UK Limited

- 8.5 FUJITSU GENERAL

- 8.6 Glen Dimplex Group

- 8.7 Gree Electric Appliances

- 8.8 Johnson Controls

- 8.9 Kensa Heat Pumps

- 8.10 Lennox

- 8.11 LG Electronics

- 8.12 Lochinvar

- 8.13 Midea

- 8.14 Mitsubishi Electric Corporation

- 8.15 NIBE Industrier AB

- 8.16 OCHSNER

- 8.17 Panasonic Corporation

- 8.18 SAMSUNG

- 8.19 STIEBEL ELTRON GmbH & Co. KG

- 8.20 Trane

- 8.21 Vaillant Group

- 8.22 WOLF GmbH