PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063828

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063828

Agent Observability And Governance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

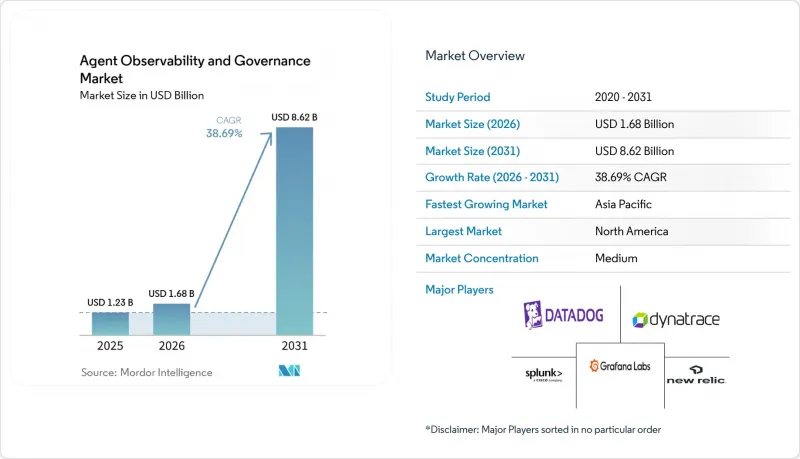

According to Mordor Intelligence, the agent observability and governance market size is expected to grow from USD 1.23 billion in 2025 to USD 1.68 billion in 2026 and is forecast to reach USD 8.62 billion by 2031 at 38.69% CAGR over 2026-2031.

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agent Observability And Governance Market Trends and Insights

Accelerating Adoption of Autonomous AI Agents in Enterprise Workflows

Fortune 500 deployment of autonomous agents climbed from 18% in early 2024 to 60% by December 2025, according to Microsoft investor disclosures. Agents now approve procurement, detect fraud, and review code, operating continuously without human checkpoints. Traditional monitoring captures latency and errors but fails to record reasoning chains or policy adherence. Salesforce responded by embedding decision-level telemetry in its Agentforce launch, setting a new market baseline. Financial regulators followed, with the Basel Committee's January 2025 proposal requiring real-time oversight of automated credit decisions. This convergence of commercial scale-up and regulatory pressure elevates observability from a dev-tool purchase to a boardroom compliance priority.

Increasing Regulatory Scrutiny Around Responsible AI Deployment

The European Union's AI Act, enforceable since August 2024, mandates technical documentation, human oversight, and audit trails for high-risk systems, with penalties up to 7% of global revenue. The United Kingdom adopted a sector-specific model in March 2025, assigning oversight to existing regulators. In the United States, the Office of Management and Budget memorandum M-24-10 requires every federal agency to inventory AI systems and assess their risks. Japan's privacy commission issued guidelines in February 2025 demanding explainability for automated decisions. These overlapping regimes fragment compliance, rewarding platforms that support multi-jurisdiction policy templates and real-time dashboards.

Lack of Interoperability Standards for Agent Telemetry

Agent-specific OpenTelemetry conventions remain in draft status as of March 2026, delaying cross-vendor compatibility. Enterprises, therefore, adopt proprietary libraries from Datadog, Dynatrace, or AWS, thereby increasing switching costs. A November 2025 CNCF survey showed 63% of multi-cloud AI users rank telemetry fragmentation among their top three pain points. Hybrid environments worsen the challenge when logs must be manually stitched across three platforms, extending mean-time-to-resolution and eroding confidence. Linux Foundation working groups launched in early 2026 aim to fast-track standardization, but consensus may take two years.

Other drivers and restraints analyzed in the detailed report include:

- Mainstream Shift to Cloud-Native Observability Toolchains

- Growing Complexity of Multi-Agent LLM Architectures

- High Total Cost of Ownership for Enterprise-Grade Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms represented 68.32% of 2025 revenue, reflecting enterprises that rushed to instrument AI agents with ready-made dashboards and OpenTelemetry collectors. Vendors such as Datadog and Dynatrace launched plug-ins for LangChain, AutoGPT, and Microsoft Semantic Kernel, shortening implementation timelines. Yet large organizations soon discovered that aligning telemetry with internal risk and legal workflows required customization beyond shrink-wrapped features.

The services segment is forecast to grow at a 36.93% CAGR through 2031, indicating a structural shift toward outsourced expertise. Global consultancies now embed certified AI governance professionals into multi-quarter engagements, driving premium billable rates. Managed-governance offerings gained traction among financial institutions that cannot tolerate observability gaps, signaling that the market for agent observability and governance services will expand faster than the software base. Skills scarcity reinforces this trend because most enterprises lack internal talent to map policy controls to agent decision paths.

Cloud deployments accounted for 71.44% of 2025 spending, as organizations increasingly opted for hyperscaler integrations that come pre-packaged with solutions such as Amazon Bedrock, Azure OpenAI, and Google Cloud Vertex AI Agent Builder. The ability to scale elastically and the availability of rapid feature releases have made public-cloud telemetry the preferred starting point for many businesses. However, strict data-sovereignty regulations and the specific needs of latency-sensitive banking systems continue to pose challenges to complete migration to the cloud.

Hybrid architectures are anticipated to grow at a compound annual growth rate (CAGR) of 37.13%, making it the fastest-growing deployment model. In these architectures, collectors are deployed on-premise to filter sensitive data payloads before forwarding sanitized metadata to a cloud-based control plane. Solutions such as Cisco AppDynamics and IBM watsonx are prime examples of this split-plane design. Enterprises have reported that hybrid models enable them to comply with regional data protection regulations while still benefiting from advanced cloud analytics. This combination is expected to drive the expansion of the agent observability and governance market share attributed to hybrid deployments.

Geography Analysis

North America led with 38.27% of 2025 revenue. Early-adopter technology companies, robust venture capital, and federal procurement mandates accelerate deployments. The Office of Management and Budget requires every agency to inventory AI systems, which funnels demand to observability vendors offering FedRAMP-ready solutions. Canada's proposed PIPEDA amendments mirror European transparency rules, while Mexico's manufacturing sector extends U.S. supplier observability requirements across the US-MCA corridor.

Asia-Pacific is projected to be the fastest-growing region, with a 41.53% CAGR. China's State Council directive forces state-owned enterprises to implement governance frameworks by the end of 2025, and draft generative-AI security rules elevate observability to a cybersecurity issue. Japan's March 2025 responsible-AI procurement guidelines accelerate adoption among electronics manufacturers and financial institutions. India's Digital Personal Data Protection Act prompts public-sector pilots that require agent tracing, and Southeast Asian nations leapfrog on-premise limitations by adopting cloud-native stacks, expanding the agent observability and governance market across emerging economies.

Europe grows at a moderate yet steady pace, underpinned by the AI Act and rapid uptake of ISO/IEC 42001 certification. Germany's technical guidelines require telemetry for high-risk public-sector AI, while the United Kingdom's sector-based oversight requires vendors to deliver vertical-specific modules. Although the region's overall spend trails North America, compliance complexity creates a durable revenue stream for full-stack governance suites. South America, the Middle East, and Africa maintain smaller bases but benefit from multinational rollouts that standardize observability policy templates across global footprints.

- Dynatrace Inc.

- Datadog Inc.

- New Relic Inc.

- Splunk Inc.

- Grafana Labs Inc.

- Honeycomb Inc.

- Observe Inc.

- OpenTelemetry Project (Cloud Native Computing Foundation)

- Cisco AppDynamics LLC

- LogicMonitor Inc.

- PagerDuty Inc.

- Snyk Limited

- Elastic N.V.

- Lightstep Inc.

- Harness Inc.

- ServiceNow Inc.

- IBM Corporation

- Microsoft Corporation

- Google LLC

- Amazon Web Services Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Adoption of Autonomous AI Agents in Enterprise Workflows

- 4.2.2 Increasing Regulatory Scrutiny Around Responsible AI Deployment

- 4.2.3 Mainstream Shift to Cloud-Native Observability Toolchains

- 4.2.4 Growing Complexity of Multi-Agent LLM Architectures

- 4.2.5 Emergence of Agent-Level Security and Compliance Mandates

- 4.2.6 Venture Capital Funding Surge in AI Agent Ops Start-ups

- 4.3 Market Restraints

- 4.3.1 Lack of Interoperability Standards for Agent Telemetry

- 4.3.2 High Total Cost of Ownership for Enterprise-Grade Platforms

- 4.3.3 Shortage of Talent Skilled in AI Governance Frameworks

- 4.3.4 Data-Residency and Sovereignty Barriers in Cross-Border Deployments

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deploymnt Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Retail and E-Commerce

- 5.4.4 Manufacturing

- 5.4.5 IT and Telecom

- 5.4.6 Government and Defense

- 5.4.7 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Dynatrace Inc.

- 6.4.2 Datadog Inc.

- 6.4.3 New Relic Inc.

- 6.4.4 Splunk Inc.

- 6.4.5 Grafana Labs Inc.

- 6.4.6 Honeycomb Inc.

- 6.4.7 Observe Inc.

- 6.4.8 OpenTelemetry Project (Cloud Native Computing Foundation)

- 6.4.9 Cisco AppDynamics LLC

- 6.4.10 LogicMonitor Inc.

- 6.4.11 PagerDuty Inc.

- 6.4.12 Snyk Limited

- 6.4.13 Elastic N.V.

- 6.4.14 Lightstep Inc.

- 6.4.15 Harness Inc.

- 6.4.16 ServiceNow Inc.

- 6.4.17 IBM Corporation

- 6.4.18 Microsoft Corporation

- 6.4.19 Google LLC

- 6.4.20 Amazon Web Services Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment