PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063889

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063889

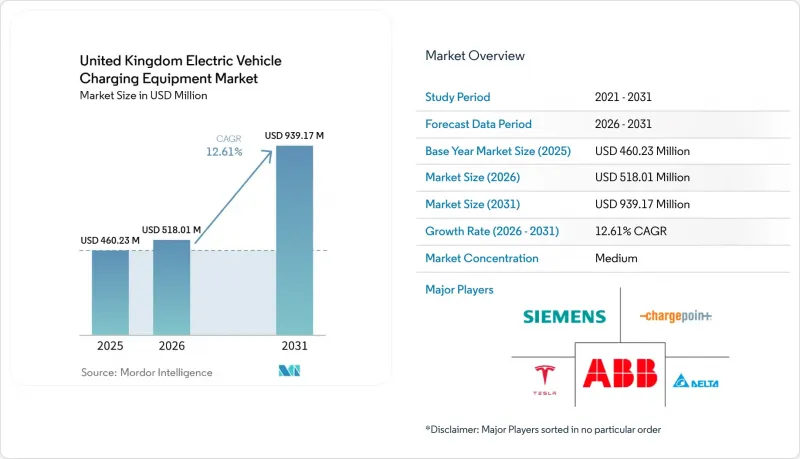

United Kingdom Electric Vehicle Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom electric vehicle charging equipment market size is expected to grow from USD 460.23 million in 2025 to USD 518.01 million in 2026 and is forecast to reach USD 939.17 million by 2031 at 12.61% CAGR over 2026-2031.

This report is Segmented by Charging Level (Level 1, Level 2, DC Fast, Ultra-Fast, and Megawatt Class), Installation Site (Residential, Commercial and Retail, Public Municipal, and Transportation Hubs), and Application (Home, Workplace, Public Urban, Highway Corridor/En-Route, and Fleet and Depot). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

United Kingdom Electric Vehicle Charging Equipment Market Trends and Insights

EV Adoption and ZEV Mandate Timelines

The Zero Emission Vehicle sales mandate requires 28% of new cars to be zero-emission by 2025, and 80% by 2030, escalating infrastructure demand as every percentage point rise in battery-electric penetration historically drives a 1.4-fold jump in public chargepoints within 18 months . Automakers face GBP 15,000 fines per non-compliant vehicle, prompting bundled home-charger offers with new EV sales. Scotland's earlier 2030 phase-out target triggered a 22% annual rise in ChargePlace installations in 2024. The mandate's flex-credit mechanism lets manufacturers bank surplus ZEV sales, creating uneven yearly installation spikes. Manufacturers, therefore, collaborate with charge-point operators to ensure capacity scales with vehicle deliveries, smoothing supply chain peaks .

OZEV Grants and Tax Incentives

The Office for Zero Emission Vehicles offers up to GBP 350 per residential chargepoint and covers 75% of workplace-charger costs to GBP 15,000, cutting the payback period on workplace hardware from 4.2 years to 2.8 years in 2024. Company-car benefit-in-kind rates remain at 2% for battery electrics through 2025, boosting corporate demand that comprised 54% of new EV registrations last year. Yet the grant excludes detached-home owners with private driveways, concentrating public funds in multi-unit dwellings and widening a rural-urban gap. Salary-sacrifice schemes further tip economics, saving employers nearly GBP 4,800 annually per vehicle. Combined, these incentives accelerate uptake but skew deployment toward high-density postcodes.

High Installation and Grid-Connection CAPEX

Rapid chargers cost GBP 40,000-80,000 installed in urban zones because grid upgrades absorb 50%-60% of budgets. Ultra-fast units climb to GBP 180,000 due to dedicated 11 kV feeds and DNO-mandated transformers . Civil works add GBP 15,000-40,000, where congested utilities complicate trenching in historic centers such as Westminster. Residential units cost GBP 800-1,500, but multi-unit dwellings need GBP 3,000-8,000 load-management systems that grant only partial offset. These economics deter private investment in lower-traffic areas, skewing installations toward motorway corridors with higher utilization.

Other drivers and restraints analyzed in the detailed report include:

- Public-Sector Funding (LEVI and Rapid Charging Fund)

- Corporate Fleet Electrification Targets

- Power-Electronics Supply-Chain Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Megawatt-class chargers exceeding 350 kW will expand at a 24.9% CAGR through 2031 as the ZEHID program funds heavy-duty depots and motorway hubs, enabling 500 kWh trucks to recharge in under 30 minutes. Level 2 hardware accounted for 51.30% of 2025 deployments, driven by 1.2 million home units utilizing 7 pence night rates under Intelligent Octopus Go. DC fast units between 50 kW and 150 kW dominate motorway services, balancing throughput with connection costs and hitting 20-plus daily sessions at prime sites. Ultra-fast chargers cluster along the M25 and M6 where Tesla and Ionity anchor long-distance corridors. Level 1 sockets now account for under 2% of new installs because 12-hour charge times cannot match modern 60 kWh packs.

Battery chemistries accepting 3C charge rates promote higher-power adoption, and IEC 61851 compliance became mandatory in public tenders during 2024, driving refresh cycles among incumbents. Level 2's future growth depends on LEVI-funded lamppost conversions delivering 5.5 kW to apartment streets where 40% of households lack driveways. Modular power-stack designs let operators upgrade 75 kW cabinets to 150 kW as utilization rises without full replacement, protecting ROI. Ultra-fast hubs add retail partners that monetize 20-minute dwell times, earning GBP 4-6 ancillary spend per session. Together, these dynamics sustain a layered power portfolio within the United Kingdom electric vehicle charging equipment market.

List of Companies Covered in this Report:

- BP Pulse (BP plc)

- Pod Point Group Holdings plc

- InstaVolt Ltd

- Shell Recharge Solutions (Shell plc)

- Osprey Charging Network Ltd

- Gridserve Sustainable Energy Ltd

- Tesla Inc.

- ABB Ltd

- Siemens AG

- ChargePoint Holdings Inc.

- Schneider Electric SE

- Eaton Corporation plc

- Delta Electronics Inc.

- EO Charging

- Rolec Services Ltd

- Wallbox NV

- Robert Bosch GmbH

- Alfen NV

- Fastned BV

- Zaptec ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV adoption & ZEV mandate timelines

- 4.2.2 OZEV grants & tax incentives

- 4.2.3 Public-sector funding (LEVI & Rapid Charging Fund)

- 4.2.4 Corporate fleet electrification targets

- 4.2.5 Dynamic tariffs enabling profitable smart charging

- 4.2.6 Second-life batteries integrated with chargers

- 4.3 Market Restraints

- 4.3.1 High installation & grid-connection CAPEX

- 4.3.2 Power-electronics supply-chain constraints

- 4.3.3 DNO queue delays at urban substations

- 4.3.4 Payment-system interoperability gaps

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

- 4.9 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Charging Level

- 5.1.1 Level 1 (Up to 3 kW)

- 5.1.2 Level 2 (3 to 50 kW)

- 5.1.3 DC Fast (50 to 150 kW)

- 5.1.4 Ultra-Fast (150 to 350 kW)

- 5.1.5 Megawatt Class (Above 350 kW)

- 5.2 By Installation Site

- 5.2.1 Residential

- 5.2.2 Commercial and Retail

- 5.2.3 Public Municipal

- 5.2.4 Transportation Hubs (Airports, Ports)

- 5.3 By Application

- 5.3.1 Home Charging

- 5.3.2 Workplace Charging

- 5.3.3 Public Urban Charging

- 5.3.4 Highway Corridor/En-Route Fast Charging

- 5.3.5 Fleet and Depot Charging

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 BP Pulse (BP plc)

- 6.4.2 Pod Point Group Holdings plc

- 6.4.3 InstaVolt Ltd

- 6.4.4 Shell Recharge Solutions (Shell plc)

- 6.4.5 Osprey Charging Network Ltd

- 6.4.6 Gridserve Sustainable Energy Ltd

- 6.4.7 Tesla Inc.

- 6.4.8 ABB Ltd

- 6.4.9 Siemens AG

- 6.4.10 ChargePoint Holdings Inc.

- 6.4.11 Schneider Electric SE

- 6.4.12 Eaton Corporation plc

- 6.4.13 Delta Electronics Inc.

- 6.4.14 EO Charging

- 6.4.15 Rolec Services Ltd

- 6.4.16 Wallbox NV

- 6.4.17 Robert Bosch GmbH

- 6.4.18 Alfen NV

- 6.4.19 Fastned BV

- 6.4.20 Zaptec ASA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment