PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066775

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066775

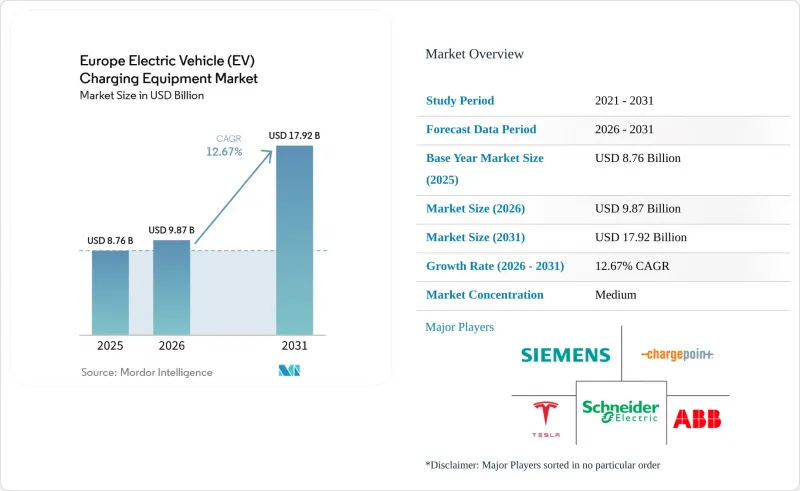

Europe Electric Vehicle (EV) Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe electric vehicle charging equipment market size in 2026 is estimated at USD 9.87 billion, growing from 2025 value of USD 8.76 billion with 2031 projections showing USD 17.92 billion, growing at 12.67% CAGR over 2026-2031.

This report is Segmented by Charging Level (Level 1, Level 2, DC Fast, Ultra-Fast, and Megawatt Class), Installation Site (Residential, Commercial and Retail, Public Municipal, and Transportation Hubs), Application (Home, Workplace, Public Urban, Highway Corridor/En-Route, and Fleet and Depot), and Geography (Germany, United Kingdom, France, Spain, Netherlands, Norway, and More).

Europe Electric Vehicle (EV) Charging Equipment Market Trends and Insights

Growing Adoption of EVs and Related Investments

Battery-electric vehicle registrations reached 3.2 million units in 2024, and the European Automobile Manufacturers' Association projects a fleet of more than 50 million EVs on the road by 2030. Automakers now embed high-power charging investments into product strategies; the IONITY consortium alone secured EUR 700 million in 2024 to grow its network to 7,000 chargers rated at 350 kW. Higher vehicle volumes raise charger utilization, which improves revenue certainty for equipment suppliers. Fleet buyers base procurement on corridor coverage rather than consumer subsidies, stabilizing long-term hardware demand.

Government-Backed Expansion of Public-Charging Networks

Member states have allocated more than EUR 10 billion for public-charging deployments between 2024 and 2030, led by Germany's EUR 5.5 billion Deutschlandnetz program and France's EUR 1.9 billion reinvestment in highway corridors. Tender frameworks specify minimum power outputs and interoperability features, so hardware vendors emphasize certified metering and remote-update capability. Competitive bidding squeezes margins, but multi-year contracts offset price pressure through volume scale.

High Installation and Grid-Connection Costs

Deploying a 150 kW fast charger can cost up to EUR 300,000, with grid fees comprising as much as half of the total. Rural sites often need kilometer-scale cabling and new transformers, which escalates break-even utilization levels. To ease barriers, suppliers promote modular cabinets that feed several 50 kW dispensers, trading peak speed for lower connection charges.

Other drivers and restraints analyzed in the detailed report include:

- EU AFIR Fast-Charger Mandate

- Grid-Balancing Revenue Streams Unlocking Charger ROI

- Distribution-Grid Congestion and Transformer Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Megawatt units above 350 kW are poised for a 23.88% CAGR, buoyed by truck electrification mandates that call for sub-30-minute refueling parity with diesel. Milence installed the first commercial 1 MW system at Antwerp-Bruges in 2024, demonstrating technical feasibility. Level 2 equipment retained a 46.85% share in 2025, thanks to the vast residential and workplace base across the European electric vehicle charging equipment market. Vendors that specialize in mid-range DC hardware feel pressure as fleet operators and highway concessionaires leapfrog directly to ultra-fast technology. The European electric vehicle charging equipment market size for Level 2 remains significant, yet growth rates favor higher power segments.

Domestic AC specialists shift their strategy accordingly. Alfen exited mid-range DC manufacturing in early 2025 to focus on high-volume AC lines, while Siemens broadened its 300-kW platform through a partnership with E.ON. Operators prefer suppliers able to bundle hardware, software, and maintenance, which favors companies with vertically integrated offerings. The expected acceleration in megawatt deployments should raise the European electric vehicle charging equipment market share of high-power systems from today's single-digit baseline toward the low-twenties by decade-end.

List of Companies Covered in this Report:

- ABB Ltd

- Schneider Electric SE

- Siemens AG

- Tesla Inc.

- ChargePoint Holdings Inc.

- Delta Electronics Inc.

- Robert Bosch GmbH

- EVBox Group

- Alfen N.V.

- Power Electronics S.L.

- Wallbox N.V.

- Kempower Oyj

- IONITY GmbH

- Fastned B.V.

- Enel X Way S.p.A.

- BP Pulse (BP p.l.c.)

- Shell Recharge (Shell p.l.c.)

- E.ON Drive GmbH

- Allego N.V.

- Eaton Corporation plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption of EVs & related investments

- 4.2.2 Government-backed expansion of public-charging networks

- 4.2.3 EU AFIR mandate for ?60 km fast-charger spacing on TEN-T corridors (2025)

- 4.2.4 Grid-balancing revenue streams (V2G & dynamic tariffs) unlocking charger ROI

- 4.2.5 Retail-energy players bundling home-solar + EV chargers

- 4.3 Market Restraints

- 4.3.1 High installation & grid-connection costs

- 4.3.2 Distribution-grid congestion & transformer upgrade delays

- 4.3.3 Fragmented payments/roaming standards outside AFIR scope

- 4.3.4 Rising electricity prices squeezing charger-operator margins

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Charging Level

- 5.1.1 Level 1 (Up to 3 kW)

- 5.1.2 Level 2 (3 to 50 kW)

- 5.1.3 DC Fast (50 to 150 kW)

- 5.1.4 Ultra-Fast (150 to 350 kW)

- 5.1.5 Megawatt Class (Above 350 kW)

- 5.2 By Installation Site

- 5.2.1 Residential

- 5.2.2 Commercial and Retail

- 5.2.3 Public Municipal

- 5.2.4 Transportation Hubs (Airports, Ports)

- 5.3 By Application

- 5.3.1 Home Charging

- 5.3.2 Workplace Charging

- 5.3.3 Public Urban Charging

- 5.3.4 Highway Corridor/En-Route Fast Charging

- 5.3.5 Fleet and Depot Charging

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Netherlands

- 5.4.7 Norway

- 5.4.8 Russia

- 5.4.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Schneider Electric SE

- 6.4.3 Siemens AG

- 6.4.4 Tesla Inc.

- 6.4.5 ChargePoint Holdings Inc.

- 6.4.6 Delta Electronics Inc.

- 6.4.7 Robert Bosch GmbH

- 6.4.8 EVBox Group

- 6.4.9 Alfen N.V.

- 6.4.10 Power Electronics S.L.

- 6.4.11 Wallbox N.V.

- 6.4.12 Kempower Oyj

- 6.4.13 IONITY GmbH

- 6.4.14 Fastned B.V.

- 6.4.15 Enel X Way S.p.A.

- 6.4.16 BP Pulse (BP p.l.c.)

- 6.4.17 Shell Recharge (Shell p.l.c.)

- 6.4.18 E.ON Drive GmbH

- 6.4.19 Allego N.V.

- 6.4.20 Eaton Corporation plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment