PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063896

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063896

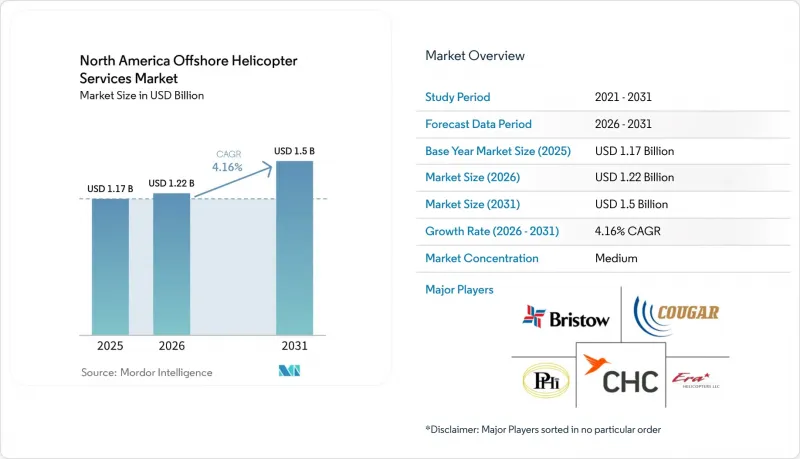

North America Offshore Helicopter Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america offshore helicopter services market size is expected to grow from USD 1.17 billion in 2025 to USD 1.22 billion in 2026 and is forecast to reach USD 1.5 billion by 2031 at 4.16% CAGR over 2026-2031.

This report is Segmented by Type (Light, Medium, Heavy Helicopters), Application (Crew Transport, Cargo Transport, Inspection/Monitoring/Surveying, Relocation/Decommissioning Support, and Others), End-User Industry (Oil and Gas, Offshore Wind, Marine and Shipping, and More), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Offshore Helicopter Services Market Trends and Insights

Rising Deep-Water Offshore Development Activity

Gulf of Mexico Lease Sale 261 in March 2024 awarded 73 tracts covering 395,000 acres and produced USD 382 million in high bids, demonstrating strong operator appetite for acreage in water depths that necessitate 90-minute helicopter transits from Houma and Lafayette shore bases. Shell followed by approving up to four exploration wells for 2025-2026 targeting prospects below 1,500 meters, sustaining call-outs for medium and heavy helicopters certified to Sea State 6 survival requirements. Mexico's Trion field, 180 kilometers offshore at 2,500 meters, began drilling in 2024 and plans 24 subsea wells that will rely on Tampico-based super-medium aircraft for crew rotations as soon as 2028. Nova Scotia's 2026 licensing round covering the Sable Island area re-energizes Canada's Atlantic offshore sector even if near-term well counts stay low . Deep-water campaigns inherently require larger cabins, auxiliary fuel, and emergency-flotation kits, creating a structural demand floor for the North America offshore helicopter services market.

Improved Viability of Offshore Oil & Gas Projects

Regional breakeven prices for deep-water Gulf of Mexico wells now sit at USD 35-45 per barrel Brent thanks to standardized subsea trees and faster drill-times, encouraging operators to commit to multi-year helicopter capacity blocks despite commodity swings. Gulf production climbed to 1.96 million barrels per day in 2026, above the pre-pandemic level and supporting predictable flight-hour purchasing. Equinor's Bay du Nord development offshore Newfoundland, expected to sanction in 2027 with first oil in 2031, will need long-range flights of 270 nautical miles from St. John's, justifying heavy twin-engine capacity retention. West White Rose's 2026 startup and tie-back projects at Hebron and Hibernia safeguard baseline demand even as Canada targets net-zero by 2050. Stronger project economics therefore decrease the revenue volatility that once typified the North America offshore helicopter services market.

Competition from Crew-Transfer Vessels

Jones Act-compliant CTVs operated by WINDEA and Atlantic Wind Transfers price a round trip at USD 150-250 versus USD 800-1,200 for comparable helicopter seats, absorbing roughly 85% of personnel transfers at U.S. wind farms . Motion-compensated gangways now allow safe transfers in 1.5-meter wave heights, conditions that represent most operational days along the New York Bight. Helicopters retain indispensable roles for emergency medical evacuation, senior-executive visits, and winter contingency transport, but those missions account for only 10-15% of offshore-wind labor hours. As wind capacity expands, CTV competition will cap the upside for rotary-wing revenues in that segment of the North America offshore helicopter services market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of U.S. Offshore-Wind Construction Zone

- Fleet-Modernization Cycle

- High Operating & Maintenance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium helicopters retained 51.7% of 2025 revenue, yet the North America offshore helicopter services market size for light twins is projected to grow at 6.6% CAGR through 2031 as AW169 and H135 aircraft migrate from offshore-wind crew transfer to high-frequency inspection flights. Heavy-lift capacity, still 28% of market revenue, is slowly shrinking as operators retire high-maintenance S-92 and H225 airframes. Super-medium newcomers such as the AW189 and soon-to-be-certified Bell 525 deliver a 20-30% fuel-burn advantage per passenger-mile, explaining why PHI, CHC, and Bristow are placing sizeable orders despite 18-month lead times .

Super-medium fleet uptake promotes mission optimization. Operators no longer treat helicopters as one-size-fits-all assets; instead, they tailor capacity to workload, deploying heavy twins for deep-water crew rotations while assigning light twins to turbine-blade inspections and harbor-pilot shuttles. This nuanced fleet mix keeps utilization high and helps the North America offshore helicopter services market defend profitability even under flat topline growth scenarios.

List of Companies Covered in this Report:

- Bristow Group Inc.

- PHI Inc.

- CHC Helicopter

- Era Helicopters LLC

- Cougar Helicopters Inc.

- Babcock International Group PLC

- Air Center Helicopters Inc.

- HNZ Group Ltd.

- Omni Helicopters International

- Gulf Helicopters Co.

- NHV Group

- Abu Dhabi Aviation Co.

- Leonardo SpA

- Airbus SE

- Lockheed Martin/Sikorsky

- Textron (Bell)

- Russian Helicopters JSC

- Kaman Corp.

- Heli-One (CHC MRO)

- Petroleum Helicopters International (PHI)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising deep-water offshore development activity

- 4.2.2 Improved viability of offshore oil & gas projects

- 4.2.3 Expansion of U.S. offshore-wind construction zone

- 4.2.4 Fleet-modernization cycle (AW139/S-92 replacements)

- 4.2.5 U.S. SAF tax-credit incentives lowering fuel costs

- 4.2.6 AI-driven predictive-maintenance savings

- 4.3 Market Restraints

- 4.3.1 Competition from crew-transfer vessels (CTV)

- 4.3.2 High operating & maintenance costs

- 4.3.3 Oil-price volatility reducing drilling programs

- 4.3.4 FAA Part-135 retrofit mandates (avionics/safety)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Light Helicopters

- 5.1.2 Medium Helicopters

- 5.1.3 Heavy Helicopters

- 5.2 By Application

- 5.2.1 Crew Transport

- 5.2.2 Cargo Transport

- 5.2.3 Inspection, Monitoring, and Surveying

- 5.2.4 Relocation and Decommissioning Support

- 5.2.5 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Offshore Wind

- 5.3.3 Marine and Shipping

- 5.3.4 Government and Defence

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Bristow Group Inc.

- 6.4.2 PHI Inc.

- 6.4.3 CHC Helicopter

- 6.4.4 Era Helicopters LLC

- 6.4.5 Cougar Helicopters Inc.

- 6.4.6 Babcock International Group PLC

- 6.4.7 Air Center Helicopters Inc.

- 6.4.8 HNZ Group Ltd.

- 6.4.9 Omni Helicopters International

- 6.4.10 Gulf Helicopters Co.

- 6.4.11 NHV Group

- 6.4.12 Abu Dhabi Aviation Co.

- 6.4.13 Leonardo SpA

- 6.4.14 Airbus SE

- 6.4.15 Lockheed Martin/Sikorsky

- 6.4.16 Textron (Bell)

- 6.4.17 Russian Helicopters JSC

- 6.4.18 Kaman Corp.

- 6.4.19 Heli-One (CHC MRO)

- 6.4.20 Petroleum Helicopters International (PHI)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment