PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064410

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064410

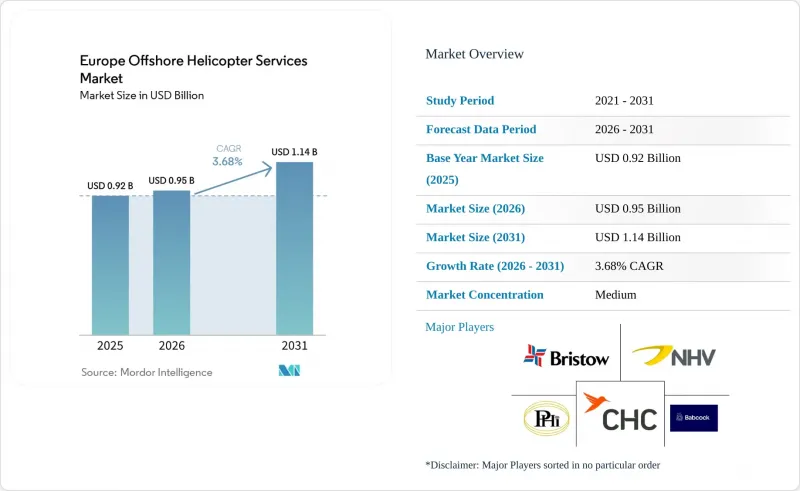

Europe Offshore Helicopter Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe offshore helicopter services market size is projected to expand from USD 0.92 billion in 2025 and USD 0.95 billion in 2026 to USD 1.14 billion by 2031, registering a CAGR of 3.68% between 2026 to 2031.

This report is Segmented by Type (Light Helicopters, Medium Helicopters, Heavy Helicopters), Application (Crew Transport, Cargo Transport, Other Applications), End-User Industry (Oil and Gas, Offshore Wind, Marine and Shipping, Others), and Geography (United Kingdom, Norway, Netherlands, Denmark, Germany, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Offshore Helicopter Services Market Trends and Insights

Offshore Wind Build-Out Beyond 50 km From Shore

Projects located farther offshore eliminate the economic viability of CTVs because sea-state limits prolong transits past two hours each way. Germany's Nordlicht field, positioned 85 kilometers offshore, and the UK's Outer Dowsing array at 54 kilometers both specify helicopter logistics for technician rotations and emergency response. Belgium's 5 GW Princess Elisabeth Island energy hub incorporates a helideck to coordinate wind-farm maintenance across multiple clusters. Such infrastructure hard-wires long-term helicopter demand because OEM maintenance contracts stipulate aerial access to hit turbine-uptime guarantees. Upcoming projects like East Anglia TWO, with first power due 2028, further widen the addressable route portfolio.

Reshoring of Deep-Water Rigs to the Northern North Sea

Equinor's Rosebank development and the redeployment of the Deepsea Bollsta to Norwegian waters in 2025 illustrate a reversal of the post-2014 rig exodus. Rig activity triggers regular crew-change flights out of Sumburgh and Bergen, highlighted by Equinor's NOK 4.3 billion Bergen contract split between CHC and Lufttransport in October 2025. Decommissioning campaigns Shell's Brent Delta and AF Gruppen's 39,500-ton platform lift also need heavy-lift sorties, ensuring a baseline of missions even as production wanes.

Two-Year Production Bottleneck for S-92 Gearboxes

Sikorsky's Phase IV gearbox has slashed groundings, yet machining complexity still leaves an 18-24-month lead time. Carriers dependent on the 19-seat S-92 must lease aircraft or defer discretionary flights, inflating residual values for serviceable airframes and prompting Bristow's pivot to AW189s.

Other drivers and restraints analyzed in the detailed report include:

- Heavy-IFR Super-Medium Fleet Renewal Cycle

- EU Sustainable-Aviation-Fuel Blending Mandates

- North Sea Crew-Transfer-Vessel Substitution on Short Hops

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium helicopters held 54.9% of Europe offshore helicopter services market share in 2025 thanks to entrenched AW139 and H175 fleets serving 150-kilometer oil-and-gas corridors. Light helicopters are set to post a 6.1% CAGR to 2031 as operators choose lower-cost H135 or AW109 platforms for turbine blade inspections and short-hop crew rotations. Heavy helicopters, chiefly the S-92, remain essential for decommissioning lifts and deep-water rigs but face slower growth because gearbox bottlenecks restrict capacity and high fuel burn magnifies ETS exposure. The Europe offshore helicopter services market size tied to heavy types therefore grows below the overall CAGR.

Momentum is shifting to 16- to 19-seat super-medium aircraft. NHV's H175 fleet began dedicated wind-farm service in April 2025, demonstrating the type's 15% fuel-efficiency edge over heavy rivals. Bristow's four AW189 deliveries between 2025 and 2026 widen mission flexibility, while Leonardo's digital-twin modules extend component lives and lift dispatch reliability. As a result, super-medium platforms are expected to erode medium-segment Europe offshore helicopter services market share beyond 2028.

List of Companies Covered in this Report:

- Bristow Group Inc.

- CHC Group Ltd.

- Babcock International Group plc

- NHV Group

- Lufttransport RW AS

- HeliService International GmbH

- Heli-Union

- PHI Group Inc.

- Omni Helicopters International

- Cougar Helicopters

- Abu Dhabi Aviation PJSC

- Era Helicopters LLC

- Bond Offshore Helicopters

- Noordzee Helikopters Vlaanderen

- Heli-One Canada / Stavanger

- Airbus SE

- Leonardo SpA

- Sikorsky (Lockheed Martin)

- Bell Textron Inc.

- MD Helicopters LLC

- Russian Helicopters JSC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Offshore wind build-out beyond 50 km from shore

- 4.2.2 Reshoring of deep-water rigs to Northern North Sea

- 4.2.3 Heavy-IFR super-medium fleet renewal cycle (AW189 / H175)

- 4.2.4 EU Sustainable-Aviation-Fuel (SAF) blending mandates

- 4.2.5 OEM digital twins enabling predictive maintenance

- 4.2.6 Green-corridor tax incentives for low-noise rotorcraft

- 4.3 Market Restraints

- 4.3.1 Two-year production bottleneck for S-92 gearboxes

- 4.3.2 North Sea crew-transfer-vessel substitution on short hops

- 4.3.3 Limited heli-deck capacity on next-gen floating turbines

- 4.3.4 EU ETS Phase IV cost pass-through on jet-A1

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Light Helicopters

- 5.1.2 Medium Helicopters

- 5.1.3 Heavy Helicopters

- 5.2 By Application

- 5.2.1 Crew Transport

- 5.2.2 Cargo Transport

- 5.2.3 Inspection, Monitoring, and Surveying

- 5.2.4 Relocation and Decommissioning Support

- 5.2.5 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Offshore Wind

- 5.3.3 Marine and Shipping

- 5.3.4 Government and Defence

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Norway

- 5.4.3 Netherlands

- 5.4.4 Denmark

- 5.4.5 Germany

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Bristow Group Inc.

- 6.4.2 CHC Group Ltd.

- 6.4.3 Babcock International Group plc

- 6.4.4 NHV Group

- 6.4.5 Lufttransport RW AS

- 6.4.6 HeliService International GmbH

- 6.4.7 Heli-Union

- 6.4.8 PHI Group Inc.

- 6.4.9 Omni Helicopters International

- 6.4.10 Cougar Helicopters

- 6.4.11 Abu Dhabi Aviation PJSC

- 6.4.12 Era Helicopters LLC

- 6.4.13 Bond Offshore Helicopters

- 6.4.14 Noordzee Helikopters Vlaanderen

- 6.4.15 Heli-One Canada / Stavanger

- 6.4.16 Airbus SE

- 6.4.17 Leonardo SpA

- 6.4.18 Sikorsky (Lockheed Martin)

- 6.4.19 Bell Textron Inc.

- 6.4.20 MD Helicopters LLC

- 6.4.21 Russian Helicopters JSC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment