PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064405

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064405

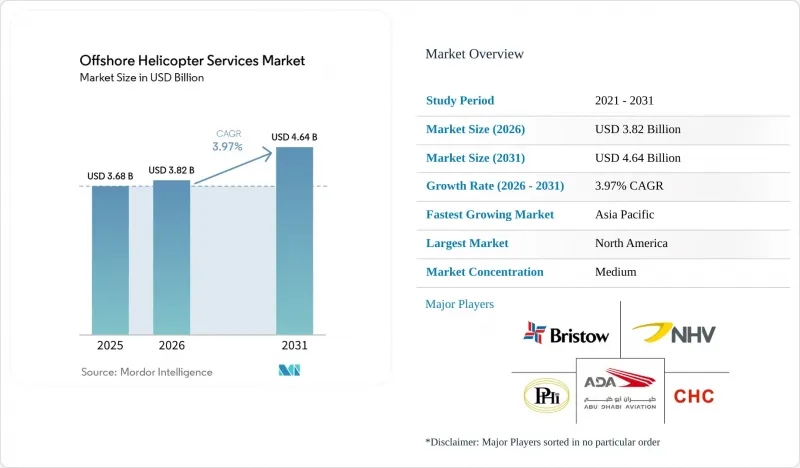

Offshore Helicopter Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the offshore helicopter services market size is expected to increase from USD 3.68 billion in 2025 to USD 3.82 billion in 2026 and reach USD 4.64 billion by 2031, growing at a CAGR of 3.97% over 2026-2031.

This report is Segmented by Type (Light Helicopters, Medium Helicopters, Heavy Helicopters), Application (Crew Transport, Cargo Transport, Inspection, Others), End-User Industry (Oil and Gas, Offshore Wind, Marine and Shipping, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Offshore Helicopter Services Market Trends and Insights

Rising Deep- and Ultra-Deep-Water E&P Spending

Investment momentum continues as operators chase high-margin barrels in ultra-deep basins where helicopters remain the only viable crew-change option. Chevron allocated USD 7 billion to offshore CAPEX in 2026, prioritizing Gulf of Mexico tie-backs that demand super-medium range. Guyana's output reached 918,000 barrels per day in 2026 and will climb when ExxonMobil's Uaru FPSO adds 250,000 barrels per day more than 190 kilometers offshore. Petrobras committed over USD 12 billion to SEAP I/II pre-salt projects in waters deeper than 2,000 meters, locking in helicopter utilization for decades. Subsea7's USD 1.25 billion Buzios 9 contract underlines the subsea infrastructure that will require aerial inspection and emergency cover. Combined, these programs are expected to keep offshore helicopter fleet utilization above 70% through 2031.

Accelerating Build-Out of Offshore Wind Farms

Global installed offshore wind capacity hit 89.2 GW in 2025 and continues to rise on projections of 9.0% CAGR to 2031. China alone added 6 GW in 2025, while Europe advanced megaprojects such as Hornsea 3 at 2.9 GW. Vietnam cleared targets that could reach 17 GW by 2035, creating new hoist-mission demand beyond 80 nautical miles. NHV logs up to 100 flight-hours per month on H175s for Vestas at Baltic Power, showing how super-medium platforms can complement crew-transfer vessels on distant wind zones. Although drones cut routine inspection sorties, emergency blade repair and medical evacuation keep helicopters integral to wind-farm O&M cycles.

Competition from Crew-Transfer Vessels

Crew-transfer vessels move crews at under half the cost of helicopters on routes below 50 nautical miles and emit 60% less carbon per passenger-kilometer. Wind-farm operators accept higher injury risk to meet ESG budgets, so helicopters now focus on long-range, hoist, and medevac sorties. NHV's H175s at Baltic Power demonstrate the unique capability to move multiple teams and conduct stretcher hoists in one flight, which CTVs cannot match. The most acute substitution threat lies in shallow European and Chinese wind zones where CTVs could absorb up to 70% of short-haul volume by 2028.

Other drivers and restraints analyzed in the detailed report include:

- Fleet Modernization Toward Medium-Heavy Twins

- Growth of Hybrid-/E-Fuel Retrofit Programs

- Oil-Price Volatility Curbing Drilling Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium helicopters dominated with 53.7% offshore helicopter services market share in 2025 thanks to AW189 and H175 fleets that deliver 14-to-16-seat capacity at 20% lower fuel burn than heavy twins. The offshore helicopter services market size tied to light types will accelerate at 6.3% CAGR through 2031 as marginal-field crew changes and wind inspection reward agility.

Operators increasingly tailor fleet mix to route length instead of defaulting to heavy platforms. Light AW139s cover sub-100-nautical-mile hops, super-mediums handle 150-plus-nautical-mile missions with hoist, and heavies stay on ultra-long routes above 300 nautical miles or Arctic duty. Abu Dhabi Aviation's fresh order for six AW139s shows Middle East carriers modernizing regional fleets under new IOGP rules. By 2031, super-mediums are forecast to exceed 60% of total fleet, while heavies drop below 15% as S-92s retire.

Geography Analysis

North America accounted for 31.9% of offshore helicopter services market share in 2025, anchored by Gulf of Mexico deep-water fields and Arctic Barents contracts. Bristow's NOK 1.9 billion Barents agreement deploys two S-92 transports and one SAR variant, servicing up to 3,400 passengers per month. CHC and Lufttransport together landed a NOK 4.3 billion Bergen contract to fly three S-92s and two AW189s to Troll, Gullfaks, and Oseberg starting May 2026. Although shallow-water Gulf routes see CTV encroachment, ultra-deep-water hubs and harsh-weather Arctic missions keep helicopter demand robust.

Europe remains the historical nucleus of the offshore helicopter services market. NHV introduced Airbus H160s financed by GD Helicopter Finance for North Sea and Baltic wind work beginning May 2026. Avincis entered offshore wind through the KN Helicopters buyout, adding H135s and H145s in Denmark. Mandatory helideck monitoring and HUMS upgrades under UK CAA and EASA rules raise compliance costs but also solidify barriers to entry.

Asia-Pacific is the fastest-growing region at 6.8% CAGR to 2031. Jadestone's Nam Du and U Minh gas project approval and ONGC's extended Vietnam Block 06.1 license will add long-range crew changes above 100 nautical miles. China added 6 GW of offshore wind capacity in 2025 yet remains CTV-centric, providing a white-space for super-medium helicopter entrants. Global Vectra supports ONGC and Reliance from Mumbai bases with over 25 helicopters, illustrating domestic fleet capability growth. South America accelerates on Guyana's march toward 1 million bpd and Brazil's pre-salt programs, while Middle East-Africa posts steady demand from Mozambique LNG and Angola's USD 7.8 billion Agogo development.

- Service Providers

- Helicopter Manufacturers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising deep- & ultra-deep-water E&P spending

- 4.2.2 Accelerating build-out of offshore wind farms

- 4.2.3 Fleet modernisation toward medium-heavy twins

- 4.2.4 Digitalised safety mandates (e.g., helideck monitoring systems)

- 4.2.5 Growth of hybrid-/e-fuel retrofit programmes

- 4.3 Market Restraints

- 4.3.1 Competition from crew-transfer vessels (CTVs)

- 4.3.2 Oil-price volatility curbing drilling budgets

- 4.3.3 Global shortage of certified offshore-rated pilots

- 4.3.4 Prolonged S-92 gearbox supply bottlenecks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Light Helicopters

- 5.1.2 Medium Helicopters

- 5.1.3 Heavy Helicopters

- 5.2 By Application

- 5.2.1 Crew Transport

- 5.2.2 Cargo Transport

- 5.2.3 Inspection, Monitoring, and Surveying

- 5.2.4 Relocation and Decommissioning Support

- 5.2.5 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Offshore Wind

- 5.3.3 Marine and Shipping

- 5.3.4 Government and Defence

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Service Providers

- 6.4.1.1 Bristow Group Inc.

- 6.4.1.2 CHC Group Ltd.

- 6.4.1.3 PHI Inc.

- 6.4.1.4 Abu Dhabi Aviation PJSC

- 6.4.1.5 CITIC Offshore Helicopter Co.

- 6.4.1.6 Cougar Helicopters Inc.

- 6.4.1.7 HeliService International GmbH

- 6.4.1.8 Era Group Inc.

- 6.4.1.9 Global Vectra Helicorp Ltd.

- 6.4.1.10 Babcock MCS Offshore

- 6.4.1.11 Lufttransport RW AS

- 6.4.1.12 NHV Group

- 6.4.1.13 Omni Taxi Aereo S.A.

- 6.4.2 Helicopter Manufacturers

- 6.4.2.1 Airbus SE

- 6.4.2.2 Leonardo SpA

- 6.4.2.3 Textron Inc. (Bell)

- 6.4.2.4 Lockheed Martin Corp. (Sikorsky)

- 6.4.2.5 Russian Helicopters

- 6.4.2.6 MD Helicopters LLC

- 6.4.1 Service Providers

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment