PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063901

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063901

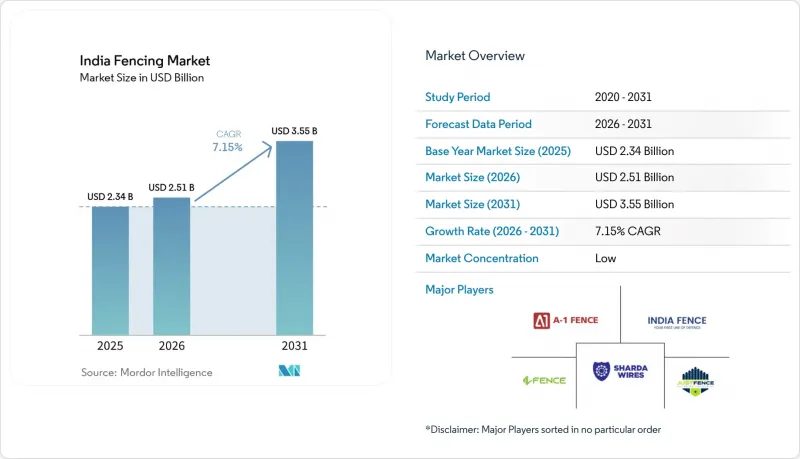

India Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india fencing market size is projected to be USD 2.34 billion in 2025, USD 2.51 billion in 2026, and reach USD 3.55 billion by 2031, growing at a CAGR of 7.15% from 2026 to 2031.

This report is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, Other), by End-User (Residential, Agricultural, Defense, Government, Mining, and More), by Installation Type (Fixed/Permanent, Temporary/Mobile), by Installation Channel (Professional Contractor, Fabricators/DIY), and by City (Mumbai, Delhi NCR, Pune, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Fencing Market Trends and Insights

Government Border Security: Sovereign Mandates Unlock Multi-Year Procurement

The India fencing market is seeing border work move from periodic buying to a long-cycle infrastructure program. India had already fenced 93.25% of its border with Pakistan and 79.08% of its border with Bangladesh. At the same time, the 1,643 km Myanmar frontier moved into a new execution phase after the USD 3.7 billion project was approved in 2024. In May 2025, the Ministry of Home Affairs also cleared USD 0.2 billion to replace more than 500 km of aging fencing on the Pakistan border with modular, multi-layered barriers. The Comprehensive Integrated Border Management System, a smart-fencing model, is expanding the product mix by linking barriers with sensors, thermal imaging, and surveillance tools. This keeps the India fencing market less exposed to normal construction cycles and gives organized suppliers a visible project pipeline.

Industrial Parks and Logistics Hubs: Plug-And-Play Infrastructure Creates Structured Fencing Demand

The India fencing market is also gaining from the spread of planned industrial parks and warehouse campuses that buy perimeter systems through formal specifications. India's warehousing sector drew USD 1.96 billion in institutional investment in 2024, while Grade A stock had expanded at a 21% CAGR over the prior five years. In March 2026, the Union Cabinet approved the BHAVYA scheme at USD 4.0 billion to develop 100 industrial parks with plug-and-play infrastructure, which makes perimeter fencing part of the base project scope rather than a later add-on. The Department for Promotion of Industry and Internal Trade stated that PM GatiShakti had mapped more than 600 projects, including industrial corridors and logistics parks, which support long-horizon site development. This gives the India fencing market a stronger mix of repeatable project demand from industrial and logistics users.

Input Cost Volatility: Steel Softness and Polymer Spikes Create Asymmetric Margin Pressure

The India fencing market faces a difficult cost mix because steel, aluminum, and PVC are not moving in the same direction. Wire rod prices dropped to USD 451-455 per tonne in October 2025, while PVC costs rose by up to 30% and aluminum prices increased by 8-10% over the same broad period. This helps basic steel-heavy products but puts pressure on composite and PVC-coated fencing, which are seeing improving demand. Producers with mixed portfolios, therefore, face uneven margin performance across product lines. The India fencing market can still grow under these conditions, but cost swings are likely to slow full adoption in newer material categories.

Other drivers and restraints analyzed in the detailed report include:

- Agricultural Fencing: Crop Losses and Wildlife Pressure Drive Rural Electrification Of Perimeters

- Rising Security Concerns: Industrial And Institutional Buyers Upgrade Perimeter Systems

- Unorganized Competition: Fragmented Supply Base Restrains Quality Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal fencing accounted for 65.1% of market revenues in 2025, maintaining its position as the largest material category in the India fencing market. Galvanized mild steel wire mesh, barbed wire, and chain-link panels still lead volume because government tenders and border projects favor certified and proven products. Aluminum fencing serves a smaller premium niche in coastal and chemical settings where corrosion resistance matters more than cost. Concrete fencing continues to hold a role in highway barriers and utility compounds, while wood remains limited to decorative residential use.

Plastic and composite fencing is the fastest-growing segment, with a 7.9% CAGR for 2026-2031, and this part of the India fencing market is expanding in gated housing and landscaped campuses. Wood-plastic composite and high-density polyethylene panels are gaining acceptance where appearance, low maintenance, and termite resistance offset the higher initial cost. Karnataka's Industrial Policy 2025-2030 supports investment in electronics, aerospace, and electric vehicle clusters, which aligns with demand for modular perimeter formats in cleaner industrial settings. Within the India fencing industry, this mix keeps metal dominant while giving composites a clearer growth lane.

Government end-users accounted for 30.5% of the India fencing market in 2025, making them the single largest demand group. Demand came from defense compounds, railway boundaries, national highways, border programs, and public utility sites. The BHAVYA scheme and the PM GatiShakti pipeline strengthen this position, as park, road, and logistics projects require perimeter systems early in the build cycle. Defense-linked orders also carry higher product specifications, which support better selling prices than basic enclosure work.

Agricultural fencing is the fastest-growing end-user segment, with a 8.1% CAGR for 2026-2031. Growth is strongest where crop losses, livestock movement, and wildlife conflict create a direct need for preventive fencing. Mining, petroleum and chemicals, and energy and power remain smaller in share, but they are important because they buy high-specification systems and are less tied to normal housing cycles. In the India fencing industry, residential demand is smaller today, but online sourcing and prefabricated kits are starting to expand access for urban homeowners.

List of Companies Covered in this Report:

- A-1 Fence Products

- India Fence

- Maa Vishla Industries (MV FENCE)

- JustFence

- Sharda Wires

- VBS Industries (VBS Group)

- Perfect Fencings

- Smart Fence Integrated Security Pvt. Ltd.

- Safe and Save Equipments (iFENCE)

- Fence Tech Innovations

- Godrej & Boyce Mfg. Co. Ltd.

- Static Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government initiatives for border security and infrastructure projects such as fencing along international borders

- 4.2.2 Government infrastructure development is driving fencing demand across roads, railways, and public facilities

- 4.2.3 Growth in industrial parks, warehouses, and logistics hubs supporting perimeter security fencing

- 4.2.4 Increasing agricultural protection needs driving demand for farm and livestock fencing

- 4.2.5 Rising security concerns boosting adoption of metal, wire mesh, and electric fencing systems

- 4.2.6 Growing need for wildlife protection and human-animal conflict mitigation driving adoption of wildlife fencing solutions

- 4.3 Market Restraints

- 4.3.1 Fluctuating steel, aluminum, and PVC prices increasing fencing product costs

- 4.3.2 Price sensitivity among rural and small-scale buyers limiting premium fencing adoption

- 4.3.3 Competition from unorganized local manufacturers affecting pricing and product quality

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology & Innovation Trends

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Sustainability & Eco-Friendly Material Trends

- 4.10 Border Security Framework & Deployment Trends

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Fixed / Permanent Fencing

- 5.3.2 Temporary / Mobile Fencing

- 5.4 By Installation Channel

- 5.4.1 Professional Contractor

- 5.4.2 Others - Fabricators, DIY / Modular Kits

- 5.5 By City

- 5.5.1 Mumbai Metropolitan Region

- 5.5.2 Delhi NCR

- 5.5.3 Pune

- 5.5.4 Bengaluru

- 5.5.5 Hyderabad

- 5.5.6 Chennai

- 5.5.7 Kolkata

- 5.5.8 Rest of India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 A-1 Fence Products

- 6.4.2 India Fence

- 6.4.3 Maa Vishla Industries (MV FENCE)

- 6.4.4 JustFence

- 6.4.5 Sharda Wires

- 6.4.6 VBS Industries (VBS Group)

- 6.4.7 Perfect Fencings

- 6.4.8 Smart Fence Integrated Security Pvt. Ltd.

- 6.4.9 Safe and Save Equipments (iFENCE)

- 6.4.10 Fence Tech Innovations

- 6.4.11 Godrej & Boyce Mfg. Co. Ltd.

- 6.4.12 Static Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment