PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064541

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064541

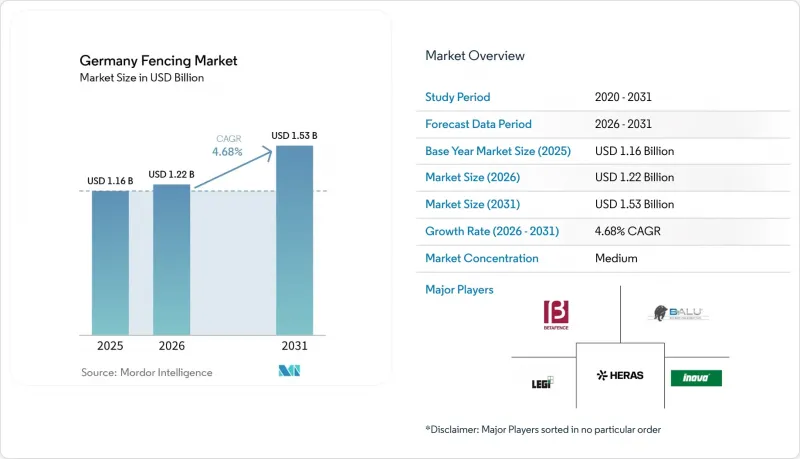

Germany Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany fencing market size is projected to be USD 1.16 billion in 2025, USD 1.22 billion in 2026, and reach USD 1.53 billion by 2031, growing at a CAGR of 4.68% from 2026 to 2031.

This report is Segmented by Material (Metal, Wood, Plastic & Composite, and More), End-User (Residential, Agricultural, Military & Defense, and More), Installation Type (Fixed / Permanent Fencing and Temporary / Mobile Fencing), Installation Channel (Professional Contractor and Others), and Geography (Berlin, Frankfurt, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Fencing Market Trends and Insights

Growth in Construction and Infrastructure Development

The Germany fencing market is closely tied to the construction cycle because every active project creates a need for temporary barriers during execution and permanent boundary systems at handover. German construction order intake grew 6.8% in real terms in 2025, which marked the first increase since 2021, and nominal orders reached EUR 113 billion (USD 129 billion), creating a broader base of live projects that require compliant fencing solutions. The German Institute for Economic Research (DIW Berlin) also expects overall construction volume to expand in 2026, with civil engineering showing the strongest momentum as infrastructure investment shifts to rail, road, and bridge work. Agricultural building permits also increased in the January to November 2025 period, which extends fencing demand into farm structures and rural perimeter projects alongside urban and commercial activity. The Germany fencing market benefits most where civil engineering and commercial work are improving faster than residential completions, because those project types carry larger and more specification-heavy perimeter needs.

Rising Demand for Security and Perimeter Protection

The Germany fencing market is seeing stronger demand from buyers that now treat perimeter protection as part of operational continuity rather than a simple boundary requirement. Germany's security posture remained elevated after federal authorities extended border controls across all German land borders from September 2024, and the Bundespolizei recorded 83,572 unauthorized entries in 2024, which kept physical security a visible priority in public procurement and facility planning. This effect now extends beyond public facilities, as commercial users such as data centers and logistics operators are buying fencing systems with forced-entry resistance and vehicle-mitigation features rather than standard perimeter products. That shift improves pricing resilience in technical categories and supports vendors with certification depth, while basic mesh and low-spec products remain exposed to price competition. In the Germany fencing market, security demand is therefore widening the gap between performance-led suppliers and volume-led suppliers.

Volatility in Raw Material Prices

The Germany fencing market remains exposed to input cost instability because steel wire products still sit at the center of many permanent security and industrial fencing systems. European Union (EU) steel supply conditions remained tight, with more than half of Europe's primary steel production capacity idled since 2021, which kept upward pressure on prices and reduced manufacturers' flexibility in responding to cost-sensitive tenders. When input costs move higher, suppliers in mid-range categories are often unable to pass through the full increase without losing orders to smaller local competitors. That creates a difficult trade-off between margin protection and product quality, especially where buyers compare offers on upfront price rather than lifecycle performance. In the German fencing market, this restraint is most visible in welded mesh, basic agricultural systems, and standard metal products, where input inflation can quickly narrow already modest margins.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Safety and Regulatory Standards

- Increasing Adoption of Smart and Low-Maintenance Fencing Solutions

- Competition from Unorganized Local Manufacturers is Affecting Pricing and Product Quality

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wood accounted for 40% of the Germany fencing market size in 2025, which kept it as the leading material category in the country. Its position rests on strong consumer acceptance in residential and agricultural settings, where buyers value familiar appearance, broad design choice, and ease of handling during installation. Germany also benefits from a large domestic timber base, which supports supply visibility and keeps wood relevant across garden fencing, paddock solutions, and farm boundaries.

In the Germany fencing market, that local supply advantage supports a wide mix of standard and premium products rather than a narrow low-cost niche. It also helps explain why wood remains established even as other materials gain share in higher-security or lower-maintenance uses. Species choice adds another layer to wood's staying power, allowing buyers to choose between treated softwood and naturally durable hardwood options, depending on budget and service-life needs. Suppliers such as ROBINIO position Robinia-based products as offering long-term in-ground durability without chemical treatment, which aligns with a segment of German buyers who prefer a more natural specification. FSC-linked sourcing and sustainability messaging have also become more visible in garden and paddock procurement, which helps wood retain appeal where aesthetics and environmental criteria both matter. In the Germany fencing industry, wood therefore continues to serve as a practical and culturally familiar material rather than a declining legacy choice. The segment's growth is slower than metal, but its installed base and broad use cases continue to anchor demand across the Germany fencing market.

Metal is the fastest-growing material segment, with the Germany fencing market size for metal projected to expand at a 5.6% CAGR between 2026 and 2031. Demand is strongest where sites require anti-climb performance, longer service life, or compatibility with access control and detection systems, making metal central to energy sites, transport facilities, critical infrastructure, and data center projects. Praesidiad and Betafence have expanded their portfolios to include certified high-security perimeter systems, reflecting this move toward performance-led procurement. Within the Germany fencing market, steel remains the main metal type because welded mesh, palisade formats, and rolled wire systems cover a wide range of industrial and public applications. Aluminum is also gaining ground in residential and light commercial applications, where lower weight and corrosion resistance support lifecycle value, even if the upfront cost is higher. Plastic and composite materials remain smaller than wood and metal, but they are building a firmer base in privacy fencing and modular residential systems. Composite infills and related systems appeal to buyers who want lower upkeep and a more uniform appearance across garden and boundary applications. Concrete remains a niche option for noise barriers and in selected infrastructure locations, while decorative materials play a limited but stable role in certain garden projects. The Germany fencing industry is therefore not shifting toward one replacement material, but toward a clearer material hierarchy shaped by aesthetics, upkeep, and security needs. That hierarchy keeps wood in the lead, but it gives metal the clearest path to outperformance through the forecast period in the Germany fencing market.

Residential held a 38% share of the Germany fencing market share in 2025, making it the largest end-user category. Germany's large housing stock, strong preference for privacy in gardens and outdoor living areas, and broad retail access to fencing products all support this position. Housing-related activity also improved in parts of the pipeline in 2025, helping maintain demand for new boundary fencing, replacement panels, and modular privacy systems. In the Germany fencing market, residential demand is especially important because it spreads orders across material types, price points, and installation channels rather than concentrating demand in a few contract buyers. That makes the segment less dependent on a single project cycle and more tied to a broad base of household spending and small-contractor activity.

The segment also benefits from strong distribution coverage across home improvement and building supply channels, making product comparison and project planning easier for households. Hornbach and other retailers continue to expand natural wood and modular fencing options, which support replacement demand and the gradual move toward planned outdoor upgrades rather than purely functional boundary work. Residential buyers span both contractor-led and self-managed projects, which keeps volume flowing through multiple sales routes in the Germany fencing market. Even with uneven residential completions at the national level, the installed housing base keeps replacement and modernization demand active. This is why residential remains the structural anchor for the Germany fencing market even while faster growth is coming from other end-users.

Agricultural users form the next important demand layer because fencing is tied to livestock management, farm security, and land separation rather than purely visual boundaries. Veterinary and farm protection requirements continue to support multi-line installations and more complex layouts than earlier single-fence farm formats. That raises per-project meterage and makes fencing an operating need rather than a discretionary one. The Germany fencing market gains from this because farm orders often combine posts, mesh, gates, and electrified elements in a single purchase set. It also supports contractor demand in larger rural jobs where mechanized installation improves speed and consistency. The energy & power is the fastest-growing end-user segment at a 6.3% CAGR through 2031, which reflects the rising perimeter needs of renewable energy and utility sites in the Germany fencing market. These sites need protection for equipment, cable routes, transformer areas, and controlled access points, which increases the value of metal and high-security perimeter systems. Public-sector, military, and government facilities also provide a steady stream of specification-led projects as critical infrastructure resilience moves further into implementation. Mining, petroleum and chemicals, and other industrial buyers add baseline replacement demand, but the strongest acceleration is clearly within energy-linked projects. This mix means the Germany fencing market is no longer driven only by household and farm demand, because strategic infrastructure buyers are taking a larger role in the growth profile.

List of Companies Covered in this Report:

- Betafence

- Heras

- LEGI Group

- Berlemann Torbau

- BALU Tore GmbH

- WISNIOWSKI

- Zaun Ltd

- Blaser Zaunsysteme GmbH

- A1 ZAUNDISCOUNT

- Heras Mobilzaun

- MY-Zaunsysteme

- GAVER Sichtschutz

- Praesidiad Group

- SchweiBgitter GmbH

- Bekaert

- DIRICKX Group

- CLD Physical Security Systems

- Jacksons Fencing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Construction and Infrastructure Development

- 4.2.2 Rising Demand for Security and Perimeter Protection

- 4.2.3 Stringent Safety and Regulatory Standards

- 4.2.4 Increasing Adoption of Smart and Low-Maintenance Fencing Solutions

- 4.2.5 Increasing Agricultural Protection Needs Drive Demand for Farm and Livestock Fencing

- 4.2.6 Growing Preference for Sustainable and Recycled-Material Fencing

- 4.3 Market Restraints

- 4.3.1 Volatility in Raw Material Prices

- 4.3.2 Competition from Unorganized Local Manufacturers Affecting Pricing and Product Quality

- 4.3.3 Price Sensitivity among Rural and Small-Scale Buyers Limiting Premium Fencing Adoption

- 4.3.4 Shortage of Skilled Fencing Installation Labor

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology & Innovation Trends

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Sustainability & Eco-Friendly Material Trends

- 4.10 Border Security Framework & Deployment Trends

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Fixed / Permanent Fencing

- 5.3.2 Temporary / Mobile Fencing

- 5.4 By Installation Channel

- 5.4.1 Professional Contractor

- 5.4.2 Others (Fabricators, DIY / Modular Kits)

- 5.5 By Geography

- 5.5.1 Berlin

- 5.5.2 Frankfurt

- 5.5.3 Hamburg

- 5.5.4 Munich

- 5.5.5 Rest of Germany

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Betafence

- 6.4.2 Heras

- 6.4.3 LEGI Group

- 6.4.4 Berlemann Torbau

- 6.4.5 BALU Tore GmbH

- 6.4.6 WISNIOWSKI

- 6.4.7 Zaun Ltd

- 6.4.8 Blaser Zaunsysteme GmbH

- 6.4.9 A1 ZAUNDISCOUNT

- 6.4.10 Heras Mobilzaun

- 6.4.11 MY-Zaunsysteme

- 6.4.12 GAVER Sichtschutz

- 6.4.13 Praesidiad Group

- 6.4.14 SchweiBgitter GmbH

- 6.4.15 Bekaert

- 6.4.16 DIRICKX Group

- 6.4.17 CLD Physical Security Systems

- 6.4.18 Jacksons Fencing

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment