PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063941

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063941

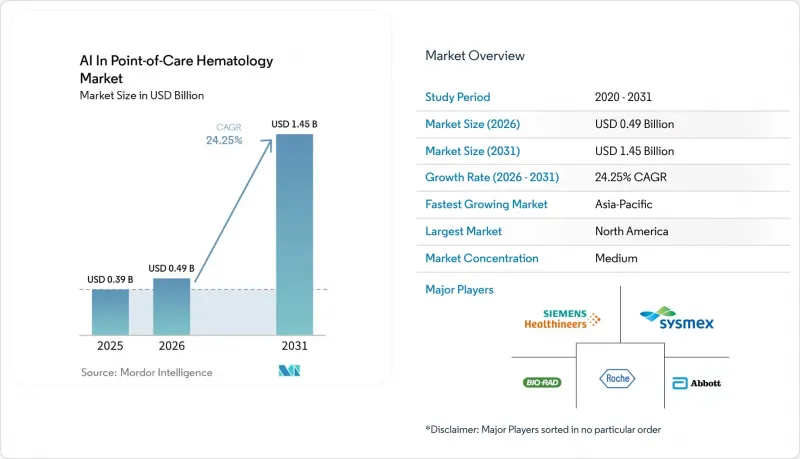

AI In Point-of-Care Hematology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in point-of-Care hematology market size is projected to expand from USD 0.39 billion in 2025 and USD 0.49 billion in 2026 to USD 1.45 billion by 2031, registering a CAGR of 24.25% between 2026 to 2031.

This report is Segmented by Product (Systems, Consumables and Reagents), Test Type (CBC, Hemoglobin/Hematocrit, and More), Technology (Impedance-Based, Optical/Imaging-based, and More), End User (Hospitals, Emergency Departments, Diagnostic Laboratories, Blood Banks, Ambulatory Centers), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Point-of-Care Hematology Market Trends and Insights

Rapid Bedside CBC Demand in Acute and Ambulatory Care

Rapid bedside hematology is becoming critical as emergency and ambulatory teams require immediate blood count results to make treatment decisions. The AI in point-of-care hematology market is benefiting from this demand, with advanced analyzers delivering multi-parameter blood counts from fingerstick or low-volume samples in minutes. This capability is particularly impactful in oncology follow-ups, monitoring immunosuppressed patients, and urgent triage, where delays can disrupt patient flow and increase repeat visits. The introduction of AI-supported testing devices for near-patient use highlights the shift toward decentralized diagnostics, enabling faster and more efficient decision-making. Providers are also leveraging this technology to transition routine blood monitoring to care sites previously reliant on central laboratories.

Rising Burden of Anemia, Infection, and Hematologic Disease

The growing prevalence of anemia, infections, oncology cases, and hematologic diseases is driving demand for AI in point-of-care hematology. Clinical validation of AI-supported analyzers in pediatric oncology demonstrated over 98.9% classification accuracy and Cohen's kappa values above 0.95, proving their reliability in high-frequency testing. These systems also offer cost advantages, making them suitable for clinics and resource-limited settings. Additionally, AI devices for sepsis triage have shown superior performance compared to traditional markers, achieving a bacterial infection AUROC of 0.83 and enhanced sensitivity for ICU-level care. These advancements are building trust in AI tools for both routine and critical care applications.

Accuracy Validation Gap Versus Central Laboratory Workflows

A critical challenge in the AI-driven point-of-care hematology market is ensuring that capillary or point-of-care test results meet the reliability standards of high-throughput central laboratory systems. Despite strong concordance results, accredited reporting environments demand method comparisons, precision assessments, and consistent evidence across sites. Commercial adoption depends on validation against established laboratory quality benchmarks, and compliance with ISO 15189 adds complexity. Smaller companies face hurdles as they often lack the resources or infrastructure to support extensive validation programs, slowing their market entry.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturized Cartridge and Capillary Sampling Adoption

- Expansion of Decentralized Diagnostics in APAC and Emerging Markets

- LIS Interoperability and Cybersecurity Compliance at Decentralized Sites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, systems dominated the product structure with 38.2% of revenue, reflecting capital spending trends and the demand for validated analyzer platforms in hospitals. The systems category benefits from hospital procurement cycles and service contracts, with instrument placement often determining consumables in workflows. Consumables and reagents are projected to grow at a robust 25.05% CAGR through 2031, driven by cartridge-based and closed-test designs that shift recurring spending to individual test events.

Complete blood count (CBC) testing contributed 39.78% of test-type revenue in 2025, maintaining its position as the volume anchor in the AI-driven point-of-care hematology market. CBC's broad clinical applications, including infection assessment, anemia workup, oncology monitoring, and pre-surgical screening, sustain its market dominance. Hemoglobin and hematocrit testing, supported by demand from anemia screening and sickle-cell monitoring, is the fastest-growing test type, with a 25.76% CAGR forecast through 2031.

Geography Analysis

In 2025, North America commanded a dominant 44.32% share of the revenue in the AI-driven point-of-care hematology market. This leadership is supported by a strong regulatory framework, enhanced reimbursement for near-patient testing, and significant investments in hospital and outpatient care. The February 2026 clearance of Athelas Home under a CLIA-waived pathway further strengthened the region's position by enabling AI-powered testing in decentralized care settings. North America's focus on faster patient routing and quicker monitoring continues to make it a key launch market for innovations in this sector.

While Europe plays a crucial role in adoption, the pace varies across nations and healthcare settings. Western European markets are advancing in AI-supported digital morphology and workflow modernization, while other regions remain in early stages of integration. The February 2026 certification of Scopio Labs' AI-powered platforms under EU IVDR regulations expanded access across the EU. Europe's growth in this market depends on how quickly hospitals and laboratories transition from pilot programs to routine workflows.

Asia-Pacific is on track to witness a robust 27.25% CAGR growth rate through 2031, making it the fastest-growing region in the AI-driven point-of-care hematology market. Growth is driven by healthcare decentralization, rising demand for community diagnostics, and local manufacturers catering to regional needs. Operational changes in Japan highlight this trend, with significant efficiency gains reported after deploying AI solutions in laboratory operations. Simpler point-of-care platforms also address service gaps in areas with limited laboratory access, while community clinics and primary care networks serve as key entry points for adoption in emerging regions.

- Abbott Laboratories

- Beckton Dickinson

- Bio-Rad Laboratories

- Boule Diagnostics

- CellaVision AB

- Diatron

- EKF Diagnostics Holdings plc

- Roche

- HemoCue AB

- HORIBA Ltd.

- Nihon Kohden

- Nova Biomedical

- PixCell Medical Technologies

- Scopio Labs

- Mindray

- Siemens Healthineers

- Sight Diagnostics

- Sysmex

- Transasia Bio-Medicals Ltd.

- Trivitron Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Bedside CBC Demand in Acute Care

- 4.2.2 Rising Burden of Anemia, Infection, and Hematologic Disorders

- 4.2.3 Miniaturized Cartridge and Capillary Sampling Adoption

- 4.2.4 Expansion of Decentralized Diagnostics in APAC and Emerging Markets

- 4.2.5 Morphology Workforce Shortages Favor AI-Assisted Review

- 4.2.6 Remote Telehematology and Digital Collaboration Unlock Small-Site Adoption

- 4.3 Market Restraints

- 4.3.1 Accuracy Validation Gap Versus Central Lab Workflows

- 4.3.2 High Instrument and Per-Test Consumable Costs

- 4.3.3 AI Bias Risk in Rare-Cell and Low-Prevalence Scenarios

- 4.3.4 LIS Interoperability and Cybersecurity Burdens at Decentralized Sites

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Systems

- 5.1.2 Consumables & Reagents

- 5.2 By Test Type

- 5.2.1 Complete Blood Count (CBC)

- 5.2.2 White Blood Cell Count / Differential

- 5.2.3 Hemoglobin / Hematocrit Testing

- 5.2.4 Anemia Screening & Triage

- 5.2.5 ESR / CRP-enabled Hematology

- 5.2.6 Digital Morphology / Peripheral Smear Review

- 5.3 By Technology & AI Capability

- 5.3.1 Impedance-based Analysis

- 5.3.2 Optical / Imaging-based Analysis

- 5.3.3 Flow cytometry-based Analysis

- 5.3.4 Microfluidic / Lab-on-Cartridge Analysis

- 5.3.5 AI-assisted Cell Classification

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Emergency Departments

- 5.4.3 Diagnostic Laboratories

- 5.4.4 Blood Banks & Transfusion Centers

- 5.4.5 Ambulatory / Urgent Care Centers

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Beckman Coulter

- 6.3.3 Bio-Rad Laboratories, Inc.

- 6.3.4 Boule Diagnostics AB

- 6.3.5 CellaVision AB

- 6.3.6 Diatron

- 6.3.7 EKF Diagnostics Holdings plc

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 HemoCue AB

- 6.3.10 HORIBA Ltd.

- 6.3.11 Nihon Kohden Corporation

- 6.3.12 Nova Biomedical

- 6.3.13 PixCell Medical Technologies

- 6.3.14 Scopio Labs

- 6.3.15 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.16 Siemens Healthineers

- 6.3.17 Sight Diagnostics

- 6.3.18 Sysmex Corporation

- 6.3.19 Transasia Bio-Medicals Ltd.

- 6.3.20 Trivitron Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment