PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063985

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063985

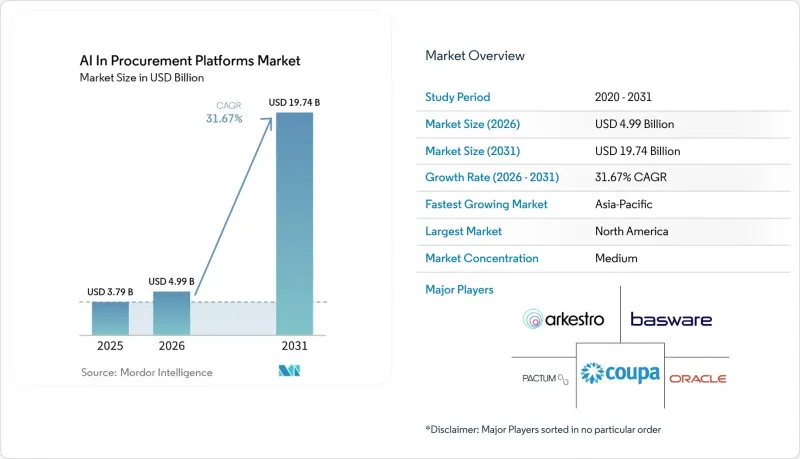

AI In Procurement Platforms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in procurement platforms market size is projected to expand from USD 3.79 billion in 2025 and USD 4.99 billion in 2026 to USD 19.74 billion by 2031, registering a CAGR of 31.67% between 2026 to 2031.

This report is Segmented by Component (Software, Services), Deployment (Cloud-Based, and More), Technology (Machine Learning, and More), Application (Supplier Management & Discovery, and More), Organization Size (Large Enterprises, Smes), End-Use Industry (Manufacturing, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Procurement Platforms Market Trends and Insights

Agentic AI for Tail-Spend Automation Redefines Savings Baselines

Agentic AI is transforming the procurement platforms market by automating tail-spend tasks that were previously manual and fragmented. This shift is driving the focus from basic workflow support to systems capable of executing approved sourcing and negotiation actions across diverse supplier bases. In 2025, Pactum reported significant growth in spend managed by its AI agents and annual recurring revenue, reflecting the increasing adoption of autonomous procurement workflows. Similarly, Coupa launched new solutions in 2026 to accelerate agentic AI value delivery, marking a shift from experimentation to scaled execution. Vendors enabling automated actions from approved policies are gaining traction, while suppliers lagging in digital readiness face mounting pressure.

Scope 3 and Supplier Compliance Data Burden Drives Platform Stickiness

Procurement platforms are becoming critical as they integrate supplier compliance data, audit records, and sustainability reporting workflows. Buyers now view these platforms as essential for managing compliance through continuous data capture, validation, and exception handling across supplier networks. Icertis expanded its partnership with SAP in 2026 to deliver AI-driven contract intelligence, highlighting the demand for embedded compliance logic in procurement. Consolidating emissions data, certifications, and contract obligations in one system increases switching costs for customers. Vendors building unified data pipelines early are gaining retention advantages as customers avoid recreating audit trails and reporting logic on new platforms.

Data Quality and Interoperability Challenges Constrain AI Agent Reliability

The AI in procurement platforms market faces challenges due to unclean and disconnected procurement data. Disparate systems housing supplier records, contracts, item masters, and spend categories reduce AI output reliability and delay deployments. A 2025 survey by MonotaRO of 407 procurement managers from Japanese firms with annual revenues above JPY 10 billion found that 70% had not implemented generative AI in procurement operations, citing data quality and availability as key barriers. The market's success depends on customers' ability to harmonize data across business units and regions, a task often underestimated, leading to extended payback periods.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Generative AI and Predictive Analytics Compresses Sourcing Cycles

- Cloud-Native Source-to-Pay Modernization Displaces On-Premise Legacy Systems

- Autonomous Buying Governance and Liability Limits Create Structural Adoption Ceilings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software accounted for 70.14% of revenue, reflecting the AI in procurement platforms market's reliance on platform licensing and suite adoption among large enterprises. Vendors like SAP, Oracle, Coupa, and JAGGAER have built a strong software base through extensive source-to-pay deployments, shaping buyer entry into the market. The software segment highlights the demand for integrated systems managing sourcing, supplier management, spend visibility, contracts, and policy enforcement.

Services are projected to grow at a 32.88% CAGR from 2026 to 2031, making it the fastest-growing component. This growth reflects the need for process design, data preparation, system integration, and change management alongside software activation. Coupa's launch of Catalyst in May 2026, an AI transformation service, underscores the shift toward a platform-plus-delivery model, where delivery support becomes a strategic revenue stream.

Cloud-based deployment held 72.3% of the market share in 2025, emphasizing the preference for scalable and connected operating models. Cloud solutions enable seamless data transfer across ERP systems, supplier portals, and finance tools without lengthy upgrade cycles. This architecture supports AI features reliant on real-time data and ensures faster access to new functionalities compared to on-premise systems.

On-premise deployment is forecast to grow at a 31.99% CAGR from 2026 to 2031, though its use cases remain limited. GEP highlights that its cloud infrastructure significantly reduces deployment time for source-to-pay connections, further solidifying the operational advantages of cloud solutions.

Geography Analysis

In 2025, North America accounted for 41.20% of the AI in procurement platforms market, making it the leading regional revenue contributor. The U.S. dominates due to significant enterprise IT budgets, a strong source-to-pay vendor base, and procurement organizations prioritizing digital transformation. Canada and Mexico benefit from supply chain proximity to the U.S. and nearshoring trends, driving demand for integrated supplier onboarding and risk management solutions.

Asia-Pacific is projected to grow at a 34.15% CAGR from 2026 to 2031, emerging as the fastest-growing region in the AI in procurement platforms market. High transaction volumes, varying procurement maturity, and digitalization pressures drive growth across public and private sectors. China leads with government-driven digitalization and enterprise procurement modernization, while Japan faces data quality challenges, indicating future adoption potential as readiness improves.

Europe remains a key market as procurement leaders focus on documenting, monitoring, and governing digital decision tools, increasing the demand for platforms offering auditability and contract-level control. In South America, Brazil and Argentina lead adoption, leveraging procurement platforms to address supplier fragmentation, cross-border trade complexities, and compliance variations. The market reflects diverse regional dynamics, with North America leading in scale, Asia-Pacific in growth, Europe in compliance, and South America in operational complexity, shaping varied vendor strategies.

- Arkestro, Inc.

- Basware Corporation

- Coupa Software Inc.

- EcoVadis SAS

- GEP Worldwide

- Globality, Inc.

- Icertis, Inc.

- Ivalua Inc.

- JAGGAER LLC

- Keelvar

- Oracle

- Pactum AI, Inc.

- Proactis Holdings PLC

- Procurify Technologies Inc.

- SAP

- Scoutbee GmbH

- Sievo Oy

- Synertrade

- TealBook Inc.

- Tradeshift Inc.

- Workday, Inc.

- Zycus Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-Takeout and Spend-Visibility Mandates

- 4.2.2 Supplier Risk and Resilience Management

- 4.2.3 Cloud-Native Source-to-Pay Modernization

- 4.2.4 Agentic AI for Tail-Spend Automation

- 4.2.5 Integration of Generative AI and Predictive Analytics

- 4.2.6 Scope 3 and Supplier Compliance Data Burden

- 4.3 Market Restraints

- 4.3.1 Data Quality and Interoperability Challenges

- 4.3.2 Concern Regarding Cybersecurity

- 4.3.3 High Implementation and Integration Cost

- 4.3.4 Autonomous Buying Governance and Liability Limits

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-based

- 5.2.2 On-premise

- 5.3 By Technology

- 5.3.1 Machine Learning

- 5.3.2 Natural Language Processing

- 5.3.3 Predictive Analytics

- 5.3.4 Generative AI / LLMs

- 5.3.5 Computer Vision / Intelligent Document Processing

- 5.4 By Application

- 5.4.1 Supplier Management & Discovery

- 5.4.2 Sourcing Event Management & RFx Automation

- 5.4.3 Spend Analytics

- 5.4.4 Contract Lifecycle Management

- 5.4.5 Procure-to-Pay / Guided Buying

- 5.4.6 Risk Management & Predictive Analytics

- 5.4.7 Invoice Automation & Accounts Payable

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 SMEs

- 5.6 By End-use Industry

- 5.6.1 Manufacturing

- 5.6.2 Retail & E-commerce

- 5.6.3 Healthcare & Life Sciences

- 5.6.4 BFSI

- 5.6.5 IT & Telecom

- 5.6.6 Government & Public Sector

- 5.6.7 Energy & Utilities

- 5.6.8 Transportation & Logistics

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Arkestro, Inc.

- 6.3.2 Basware Corporation

- 6.3.3 Coupa Software Inc.

- 6.3.4 EcoVadis SAS

- 6.3.5 GEP Worldwide

- 6.3.6 Globality, Inc.

- 6.3.7 Icertis, Inc.

- 6.3.8 Ivalua Inc.

- 6.3.9 JAGGAER LLC

- 6.3.10 Keelvar

- 6.3.11 Oracle Corporation

- 6.3.12 Pactum AI, Inc.

- 6.3.13 Proactis Holdings PLC

- 6.3.14 Procurify Technologies Inc.

- 6.3.15 SAP SE

- 6.3.16 Scoutbee GmbH

- 6.3.17 Sievo Oy

- 6.3.18 Synertrade

- 6.3.19 TealBook Inc.

- 6.3.20 Tradeshift Inc.

- 6.3.21 Workday, Inc.

- 6.3.22 Zycus Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment