PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065517

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065517

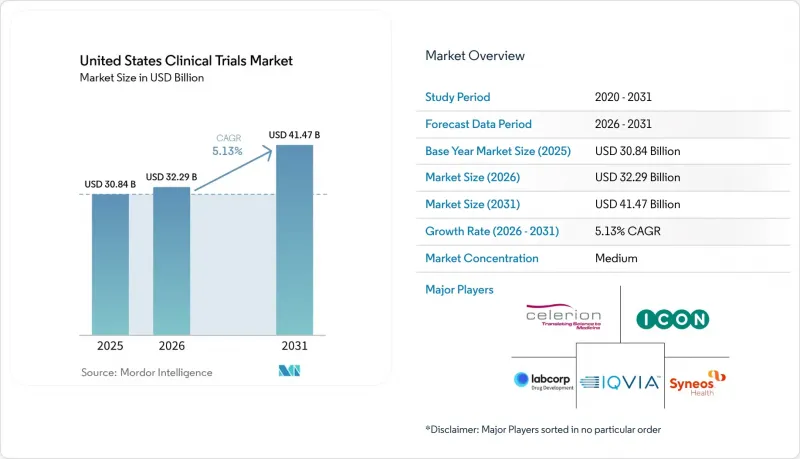

United States Clinical Trials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states clinical trials market size is projected to expand from USD 30.84 billion in 2025 and USD 32.29 billion in 2026 to USD 41.47 billion by 2031, registering a CAGR of 5.13% between 2026 to 2031.

This report is Segmented by Phase (I-IV), Study Design (Interventional, Observational, Expanded Access), Indication (Oncology, CNS, Autoimmune, Cardiovascular, Diabetes, Obesity, Pain, Infectious, Rare Diseases), Sponsor (Pharma, Biotech, Device, Academic, Government), and Service Type (Protocol Design, Site Management, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Clinical Trials Market Trends and Insights

Outsourcing Of Complex R&D Programs

The move toward outsourcing remains one of the clearest drivers of the United States clinical trials market. Sponsors are no longer sending only routine activities to outside partners, because they are also shifting regulatory work, safety support, site management, and post-approval obligations into broader service contracts. ACRO reported in March 2026 that member CROs conducted or participated in 7,634 studies involving 1.4 million patients in 2025 and supported 592 sponsor companies, which shows how much program volume is already flowing through external delivery networks. This matters because a broader outsourcing scope tends to lengthen relationships and raises switching costs once a provider is embedded across several programs. It also favors companies that can combine operational scale with therapeutic depth, which is why the United States clinical trials market increasingly rewards providers that can offer integrated clinical trial services instead of isolated tasks. Smaller generalist firms still compete, but growth is becoming harder where sponsors want fewer vendors and deeper accountability across full development programs.

Oncology And Rare-Disease Pipeline Expansion

Oncology remains the largest engine of study demand in the United States clinical trials market. IQVIA reported that oncology accounted for 38% of all Phase I to III industry-sponsored trial starts in 2025, and one-third of those starts involved novel modalities such as antibody-drug conjugates, radiopharmaceutical therapeutics, chimeric antigen receptor gene therapies, and multi-specific antibodies. These programs place heavier demands on site qualification, biomarker screening, cold chain handling, and long follow-up periods, which raises the need for specialized delivery teams. Rare-disease development adds another layer because patient pools are small and widely dispersed, making national outreach and flexible site coverage more important than traditional site-centric recruitment. AACR reported in 2026 that Phase I non-small cell lung cancer activity had consolidated at 223 US sites by 2024, which signals tighter access to high-performing oncology centers and reinforces the value of providers with established site relationships. As a result, the United States clinical trials market continues to favor CRO services that combine oncology scale with strong rare-disease recruitment models.

Recruitment And Retention Shortfalls

Recruitment still acts as one of the main brakes on the United States clinical trials market. Frontiers in Medicine reported in 2025 that more than 80% of studies missed planned recruitment timelines, and the Association of Clinical Research Professionals reported in 2025 that 28% of sites still identified recruitment and retention as a top operating challenge. IQVIA also reported that median enrollment duration in 2025 exceeded 16 months, which shows how strongly this issue affects study delivery even in a large and mature research system. Retention is part of the same problem because losses after enrollment force sites and sponsors to over-recruit, reopen outreach, and add costs that were not planned at study start. The burden becomes even heavier when site teams are already stretched by multiple systems, staff turnover, and principal investigator shortages. For that reason, providers in the United States clinical trials market are putting more value on retention design, not just patient identification, and that is helping patient support services move closer to the core of clinical trial services.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Trial Design And Recruitment

- Hybrid And Decentralized Trial Adoption

- Protocol Complexity And Cost Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Phase III held 48.87% of phase revenue in 2025, which kept it as the largest phase segment in the United States clinical trials market. Large oncology, cardiovascular, and neurology programs supported that position because they required broad site networks, central lab coordination, and long monitoring cycles. The segment also benefited from resumed late-stage activity that had been deferred earlier, which raised contract value as more studies moved back into active enrollment windows. In practical terms, Phase III remains the part of the United States clinical trials market where sponsor budgets, monitoring effort, and operational complexity come together most clearly. That is why providers with strong site oversight and national delivery footprints still capture much of the largest contract pool.

Phase I is projected to expand at 7.36% CAGR through 2031, making it the fastest-growing phase in the United States clinical trials market. IQVIA reported that emerging biopharma companies generated 68% of all global Phase I starts in 2025, which supports the view that first-in-human activity is rising among sponsors that rely heavily on external partners. This pattern supports demand for CRO services because many of these sponsors do not maintain in-house units for healthy-volunteer work, dose escalation, or intensive safety management. It also supports clinical trial services that combine early-phase unit capacity with flexible outpatient access and tighter data turnaround. ICON reflected this direction in May 2026 by opening a new Clinical Research Unit in San Antonio and adding satellite outpatient clinics in Houston and Lawrence, which expanded early-phase capacity in the United States.

Interventional studies accounted for 69.83% of study design revenue in 2025 and therefore represented the largest share of the United States clinical trials market size within this segment. Their lead reflects the volume of randomized controlled work across oncology, immunology, and cardiovascular disease, where direct sponsor oversight and service intensity remain high. These studies generate heavier operational needs because they require active treatment assignment, site monitoring, endpoint collection, and protocol compliance across many settings. That structure keeps interventional work central to the United States clinical trials market even as more complementary evidence models develop. Observational programs remain important, but they usually create a different revenue profile because they are more closely linked to post-approval evidence, payer support, and real-world study design.

Expanded access is forecast to grow at 7.87% CAGR through 2031, which makes it the fastest-rising study design category in the United States clinical trials market. FDA guidance published in November 2025 continued to support public access pathways for investigational drugs used outside formal trial enrollment, which helps explain why this category is gaining more attention from sponsors. The segment also creates a more specialized operating need because adverse event reporting and oversight must run alongside the main development program without blurring responsibilities. That requirement opens room for providers that can coordinate safety, medical writing, and regulatory support within the same workflow. As a result, the United States clinical trials market is seeing more value placed on service providers that can handle expanded access execution with the same discipline applied to formal registration programs.

List of Companies Covered in this Report:

- Advanced Clinical

- Allucent

- Caidya

- Celerion

- CenExel

- Clario

- ICON

- IQVIA

- LabCorp

- Medidata

- MedPace

- Parexel International

- Rho

- Suvoda

- Syneos Health

- Thermo Fisher Scientific (PPD)

- Veristat

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outsourcing of Complex R&D Programs

- 4.2.2 Oncology and Rare-Disease Pipeline Expansion

- 4.2.3 AI-Enabled Trial Design and Recruitment

- 4.2.4 Hybrid And Decentralized Trial Adoption

- 4.2.5 FDA Guidance Clarity for Decentralized Elements

- 4.2.6 Diversity Action Plan Operationalization

- 4.3 Market Restraints

- 4.3.1 Recruitment and Retention Shortfalls

- 4.3.2 Protocol Complexity and Cost Inflation

- 4.3.3 Site Technology Overload and PI Attrition

- 4.3.4 Diversity-Planning Policy Uncertainty

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Phase

- 5.1.1 Phase I

- 5.1.2 Phase II

- 5.1.3 Phase III

- 5.1.4 Phase IV

- 5.2 By Study Design

- 5.2.1 Interventional

- 5.2.2 Observational

- 5.2.3 Expanded Access

- 5.3 By Indication / Therapeutic Area

- 5.3.1 Oncology

- 5.3.1.1 Blood Cancers

- 5.3.1.2 Solid Tumors

- 5.3.2 CNS Conditions

- 5.3.2.1 Epilepsy

- 5.3.2.2 Parkinson's Disease

- 5.3.2.3 Stroke

- 5.3.2.4 Traumatic Brain Injury

- 5.3.2.5 Amyotrophic Lateral Sclerosis

- 5.3.3 Autoimmune / Inflammation

- 5.3.3.1 Rheumatoid Arthritis

- 5.3.3.2 Multiple Sclerosis

- 5.3.3.3 Osteoarthritis

- 5.3.3.4 Irritable Bowel Syndrome

- 5.3.4 Cardiovascular Diseases

- 5.3.5 Diabetes

- 5.3.6 Obesity

- 5.3.7 Pain Management

- 5.3.8 Infectious Diseases

- 5.3.9 Rare Diseases and Orphan Conditions

- 5.3.1 Oncology

- 5.4 By Sponsor

- 5.4.1 Pharmaceutical Companies

- 5.4.2 Biotechnology Companies

- 5.4.3 Medical Device Companies

- 5.4.4 Academic Medical Centers

- 5.4.5 Government and Nonprofit Research Organizations

- 5.5 By Service Type

- 5.5.1 Protocol Design and Feasibility

- 5.5.2 Site Identification and Activation

- 5.5.3 Site Management and Monitoring

- 5.5.4 Patient Recruitment and Retention

- 5.5.5 Central Laboratory and Bioanalytical Testing

- 5.5.6 Clinical Data Management and Biostatistics

- 5.5.7 Medical Writing and Regulatory Affairs

- 5.5.8 Pharmacovigilance and Safety

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Advanced Clinical

- 6.3.2 Allucent

- 6.3.3 Caidya

- 6.3.4 Celerion

- 6.3.5 CenExel

- 6.3.6 Clario

- 6.3.7 ICON plc

- 6.3.8 IQVIA

- 6.3.9 Labcorp Drug Development

- 6.3.10 Medidata

- 6.3.11 Medpace

- 6.3.12 Parexel International

- 6.3.13 Rho

- 6.3.14 Suvoda

- 6.3.15 Syneos Health

- 6.3.16 Thermo Fisher Scientific (PPD)

- 6.3.17 Veristat

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment