PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064015

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064015

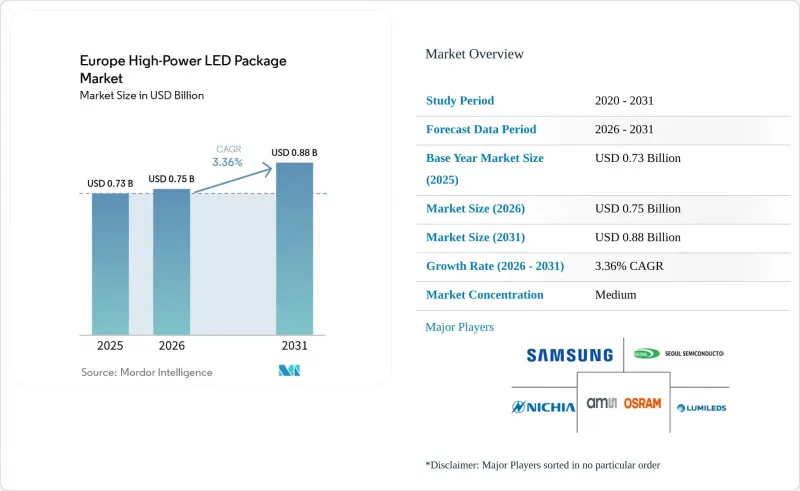

Europe High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe high-Power lED package market size was valued at USD 0.73 billion in 2025 and is estimated to grow from USD 0.75 billion in 2026 to reach USD 0.88 billion by 2031, at a CAGR of 3.36% during the forecast period (2026-2031).

This report is Segmented by Power Range (1 W To 3 W, 3 W To 10 W, and Above 10 W), Architecture (Single-Die Packages, Multi-Die Packages, and More), Application (General Lighting, Automotive Lighting, Display and Backlighting, and More), and Country (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe High-Power LED Package Market Trends and Insights

Rapid Decline in $/lm for High-Power Packages

High-power LED package prices are falling roughly 15% a year as oversupply in China's gallium-nitride wafer capacity converges with efficiency gains in phosphor conversion. European luminaire makers are redesigning fixtures around fewer, brighter emitters, cutting bill-of-materials costs but shrinking supplier margins. Vertically integrated vendors that own phosphor IP can absorb wafer volatility, whereas merchant assemblers face immediate commoditization. Lumileds' LUXEON HL2X-V, launched February 2025, underscores this shift by delivering 200 lm W-1 at 85 °C junction temperature and lowering system cost for industrial high-bay retrofits. Procurement teams increasingly emphasize dollar-per-lumen benchmarks over headline efficacy, tightening contract cycles and accelerating design revisions.

Soaring Automotive LED Penetration in China and Japan

LED penetration in Chinese passenger cars topped 70% in 2025, and Japan cleared micro-LED arrays for ultrathin headlamps in March 2025. European automakers are now importing these architectures to meet EU safety rules and differentiate premium trims, bringing chip-on-board modules into regional supply chains. Hella, part of Forvia, cited lighting revenue of EUR 3 billion (USD 3.39 billion) for 2023 and a 25% share of Europe's premium headlamp segment, on the back of gallium-nitride-on-silicon-carbide packages that cut EV energy draw by 40%. Asian cost baselines, however, frame European negotiations, forcing suppliers to match APAC unit economics while meeting stricter binning and reliability metrics.

Margin Erosion from Intense Price Competition

Chinese foundries running at 85%+ utilization undercut European pricing by up to 30%, compressing gross margins below sustainable thresholds. Lumileds' August 2025 sale to San'an Optoelectronics for USD 239 million illustrated the survival advantage of upstream wafer integration. European vendors, therefore, retreat to niches such as AEC-Q102-qualified automotive packages, horticulture spectra, and ultra-high-CRI museum modules. Yet lower volume limits fixed-cost absorption, creating a feedback loop of continuing margin pressure and defensive consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Mandates Across ASEAN

- Industrial Retrofits to High-Bay LED Fixtures

- Volatile Sapphire Substrate Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Above-10-W packages are advancing at a 3.98% CAGR to 2031, outpacing lower-power classes that currently dominate the Europe high-power LED package market. The 1 W-3 W bracket, which held a 47.13% share in 2025, remains popular for general lighting retrofits, where cost and form-factor familiarity drive purchasing. Growth, however, is flattening as most large warehouses and offices have completed LED conversions by 2025 and now enter replacement cycles. Packages in the 3 W-10 W tier support automotive daytime running lamps and streetlights, balancing lumen output against manageable heat loads.

Technology breakthroughs in GaN-on-SiC substrates and two-phase vapor chambers now keep junction temperatures below 125 °C at 200 W cm-2 flux, enabling above-10-W modules to invade stadium floodlighting and port-crane luminaires. Lumileds' LUXEON HL2X-V exemplifies this shift, pairing 12% higher efficacy with reduced thermal resistance. IEC 62471 rules that cap drive currents for blue-rich spectra impose limits on absolute efficacy, prompting suppliers to tweak phosphor blends to meet Risk Group 1 while preserving target brightness.

List of Companies Covered in this Report:

- Nichia Corporation

- ams-OSRAM AG

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Samsung Electronics Co., Ltd.

- Cree LED, Inc.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Lextar Electronics Corporation

- Broadcom Inc.

- Brightek Optoelectronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Stanley Electric Co., Ltd.

- Lite-On Technology Corporation

- Refond Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- TDK Electronics AG

- Wurth Elektronik GmbH & Co. KG

- Vishay Intertechnology, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Decline in $/lm for High-Power Packages

- 4.2.2 Soaring Automotive LED Penetration in China and Japan

- 4.2.3 Energy-Efficiency Mandates Across ASEAN

- 4.2.4 Industrial Retrofits to High-Bay LED Fixtures

- 4.2.5 Thermal-Management Breakthroughs Enabling 10 W+ Packages*

- 4.2.6 India's PLI Incentives for GaN-on-SiC LED Foundries*

- 4.3 Market Restraints

- 4.3.1 Margin Erosion from Intense Price Competition

- 4.3.2 Volatile Sapphire Substrate Supply

- 4.3.3 Photobiological Safety Norms Limiting Drive Current

- 4.3.4 Inadequate End-of-Life Recycling Streams*

- 4.4 Regulatory Landscape

- 4.5 Impact of Macroeconomic Factors

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Others (CSP, Flip-chip, Hybrid Modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Europe

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 ams-OSRAM AG

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Cree LED, Inc.

- 6.4.7 Everlight Electronics Co., Ltd.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Lextar Electronics Corporation

- 6.4.10 Broadcom Inc.

- 6.4.11 Brightek Optoelectronic Co., Ltd.

- 6.4.12 Dominant Opto Technologies Sdn. Bhd.

- 6.4.13 Stanley Electric Co., Ltd.

- 6.4.14 Lite-On Technology Corporation

- 6.4.15 Refond Optoelectronics Co., Ltd.

- 6.4.16 Hongli Zhihui Group Co., Ltd.

- 6.4.17 NationStar Optoelectronics Co., Ltd.

- 6.4.18 TDK Electronics AG

- 6.4.19 Wurth Elektronik GmbH & Co. KG

- 6.4.20 Vishay Intertechnology, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment