PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064544

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064544

Contingent Workforce Management Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

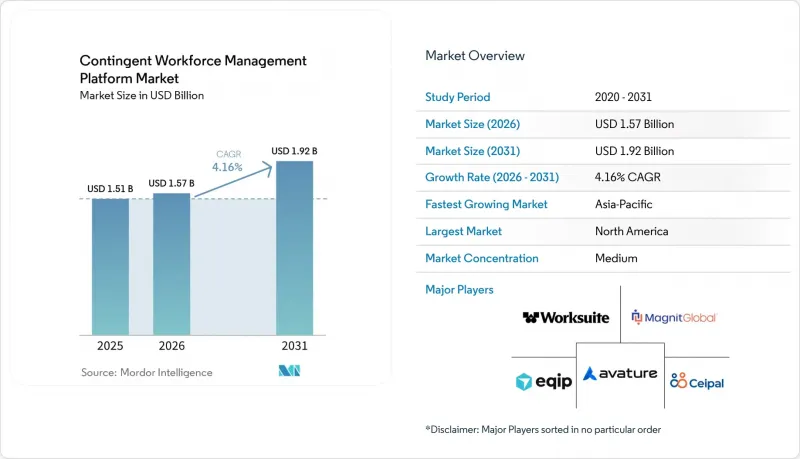

According to Mordor Intelligence, the contingent workforce management platform market size is projected to be USD 1.51 billion in 2025, USD 1.57 billion in 2026, and reach USD 1.92 billion by 2031, growing at a CAGR of 4.16% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Functionality (Vendor Management System [VMS], and More), Deployment Mode (Cloud-Based, and More), Organization Size (Large Enterprises, and More), End-User Industry (Information Technology and Telecommunications, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Contingent Workforce Management Platform Market Trends and Insights

Rising Enterprise Reliance on Flexible and Project-Based Labor

Flexible labor is now part of planned operating models, especially in sectors where delivery timelines, technology needs, and cost pressures change faster than permanent hiring cycles can adjust. That change raises the value of systems that can manage worker type, supplier use, approvals, onboarding, contract controls, and payment workflows with a common governance layer. The contingent workforce management (WFM) platform market benefits because enterprises want program-level visibility and consistent policy enforcement, rather than local contractor administration handled via email and spreadsheets. Higher-value external roles, including interim leaders and specialist consultants, also require stronger controls around tax treatment, intellectual property, contract value, and country-specific engagement rules. Buyers are therefore favoring platforms that can manage the full external worker journey and maintain auditable records across multiple talent channels. Beeline's June 2025 acquisition of MBO Partners reflected this need for broader external talent coverage, including independent contractors, consultants, gig workers, and payrolled professionals, within a single, compliant environment.

AI-Enabled Visibility, Matching, and Spend Optimization

AI has moved from optional product differentiation to a baseline expectation in the contingent workforce management platform market. Enterprises now want faster matching, cleaner spend visibility, rate benchmarking, workflow suggestions, and better forecasting built directly into everyday program management. Beeline introduced Beeline AI in April 2025 with skills-proximity scoring, agentic capabilities, and automated compliance policy management built on its contingent labor data foundation. SAP Fieldglass strengthened the same direction in its May 2026 release through AI-assisted resume assessment, AI-enhanced statement-of-work collaboration, and automated worker role suggestions from SOW details. These tools reduce sourcing and intake friction, but they also raise buyer expectations around explainability, oversight, and clear audit trails for decisions that affect external talent engagement. Vendors that combine automation with human review are gaining ground because procurement, HR, and legal teams want speed without giving up control.

Complex Integration with HRIS, ERP, Procurement, and Payroll Stacks

Integration remains the most persistent adoption barrier in the contingent workforce management platform market. Contingent labor programs usually cut across HR, procurement, finance, and payroll systems that were built separately and often use different definitions for worker type, cost center, supplier data, and invoicing rules. Beeline states that its platform supports 845 HCM and ERP integrations, including 500 Oracle, 440 SAP, and 405 Workday connections, which shows how broad the technical landscape has become. The same material notes that legacy batch-processing architectures can still create timing gaps and validation issues when buyers expect real-time API behavior. Integration cost and complexity can delay deployment decisions, especially when enterprises also need local tax, billing, supplier, and worker rules aligned across countries. Even so, organizations that postpone automation often continue to accumulate fragmented records and weaker auditability, which can make later transitions even harder.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Worker Classification and Labor Compliance Requirements

- Need for Faster Access to Specialized Digital and Professional Skills

- Data Privacy, Cybersecurity, and Cross-Border Data Transfer Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 67.22% of the contingent workforce management platform market share in 2025, while services are projected to expand at a 6.72% CAGR through 2031. Software remains the core revenue engine because buyers still want a system of record that centralizes requisitions, worker data, supplier lists, approval rules, timesheets, invoices, and reporting within a single operating layer. Configurable software also gives enterprises a practical way to enforce policies around tenure limits, onboarding steps, role approvals, and rate controls across business units that may otherwise manage external talent differently. The continued weight of software therefore reflects its role as the operational backbone of formal contingent labor programs, especially in global organizations with large spend under management. Yet the faster growth in services shows that many enterprises do not want to manage complex rollouts, integrations, and policy alignment on their own.

Implementation, integration, and managed support are becoming part of the standard buying package for buyers with global programs and cross-system complexity. The services mix is also moving beyond one-time setup work toward recurring support around compliance monitoring, supplier performance, analytics review, user administration, and program optimization. That change matters in the contingent workforce management platform industry because service teams often become part of day-to-day governance after the platform goes live and internal ownership matures. It creates a stickier revenue profile, with services reinforcing software retention and helping buyers handle multi-country operating models that are difficult to standardize quickly. The result is that end-to-end vendors and their partners are broadening their managed-service capabilities rather than relying solely on license growth, especially where buyers want measurable outcomes tied to compliance, fill rates, and spend visibility.

VMS retained a 35.66% share in 2025, while talent sourcing and direct sourcing integration are set to expand at a 5.99% CAGR through 2031. VMS remains the foundational layer because it connects requisitions, suppliers, approvals, timesheets, invoicing, and reporting into a single, governed workflow, rather than leaving them spread across several tools and email chains. Large enterprise programs still depend on this core capability to control spend and enforce policy across many geographies, cost centers, and staffing partners. Its leading share, therefore, reflects continued relevance rather than simple buyer inertia, since point solutions still struggle to replace the breadth of control that VMS platforms provide. At the same time, the faster growth of direct sourcing shows that buyers now want platforms to improve talent access and administration.

Enterprises are trying to reduce agency markup and improve reuse of pre-vetted talent pools before opening demand to the wider supplier network. SAP Fieldglass added AI-enhanced statement-of-work collaboration and automated worker role suggestions in May 2026, showing how sourcing features are moving closer to planning and intake workflows rather than staying separate from them. Compliance and risk management modules are also gaining weight as classification rules tighten and buyers want stronger evidence that engagement decisions were applied consistently. Spend management and rate benchmarking tools are attracting more finance attention as enterprises seek clearer visibility into contractor pricing, markups, and supplier performance across business lines. Contractor lifecycle management is expanding as external talent mixes now include independent professionals engaged through AOR and EOR models, while other modules, such as DEI tracking and mobile-first field labor support, show how the contingent workforce management platform industry is broadening beyond the historic VMS core.

Geography Analysis

North America held 37.65% of the contingent workforce management platform market share in 2025 and remained the largest regional revenue base. The United States anchors demand because many large enterprises in the region already run formal contingent programs that integrate procurement, HR, finance, legal, and supplier management into a single operating model. Buyers in this region also face complex classification and co-employment exposures, which keep governance features high on the purchase agenda and support continued investment in formal systems of record. California's AB5 guidance continued to reinforce the need for documented contractor tests and consistent classification workflows in 2026. Canada and Mexico are also becoming more relevant to program design as multinational employers extend common governance standards across North America instead of managing each country through local exceptions.

Europe is becoming a regulation-led growth area for the contingent workforce management platform market. The EU Platform Work Directive introduced a rebuttable presumption of employment where direction and control are found, and member states must transpose the rules by December 2, 2026. That legal pressure supports demand for platforms that can monitor classification, tenure, approvals, and worker status across different national rules and corporate entities. The United Kingdom remains important as vendors must support separate off-payroll compliance needs alongside the EU framework, while Germany stands out for its compliance-heavy temporary labor environment and strong demand for governed external workforce processes.

Asia-Pacific is forecast to grow at a 6.31% CAGR through 2031, the fastest regional rate in the contingent workforce management platform market. China, India, Japan, and Southeast Asia are expanding the pool of project-based and platform-mediated work, which is drawing more formal governance and technology investment from local firms and multinational employers. India stands out as a major growth point because global enterprises continue to manage large contractor populations in IT and digital services delivery, and need better visibility across suppliers and engagements. The Middle East is still early in adoption, but the UAE and Saudi Arabia are creating space for structured oversight of external workforces as non-national labor programs expand under diversification efforts. South America and Africa remain less mature, yet Brazil and South Africa serve as the main regional anchors for multinational buyers seeking more consistent contingent workforce control and clearer audit trails.

- Beeline

- Magnit, LLC

- Avature Limited

- CXC Global

- Worksuite Inc.

- VectorVMS1 LLC

- Pixid

- Eqip AG

- Netive VMS

- Prosperix

- Ceipal Corp.

- Flextrack Inc.

- Simplify Workforce

- StafferLink

- Trio Workforce Solutions

- Flentis Corporation

- DirectSkills

- Worksome ApS

- MBO Partners

- 3 Story Software LLC

- i-Resource Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Enterprise Reliance on Flexible and Project-Based Labor

- 4.2.2 Tightening Worker Classification and Labor Compliance Requirements

- 4.2.3 AI-Enabled Visibility, Matching, and Spend Optimization

- 4.2.4 Need for Faster Access to Specialized Digital and Professional Skills

- 4.2.5 Expansion of Direct Sourcing and Private Talent Pool Strategies

- 4.2.6 Convergence of Services Procurement and Contingent Labor Workflows

- 4.3 Market Restraints

- 4.3.1 Complex Integration With HRIS, ERP, Procurement, and Payroll Stacks

- 4.3.2 Data Privacy, Cybersecurity, and Cross-Border Data Transfer Risk

- 4.3.3 Rising Identity Fraud and Worker Verification Burden in Remote Hiring

- 4.3.4 Governance Friction Across HR, Procurement, Legal, and Finance Stakeholders

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration

- 5.1.2.2 Support and Maintenance

- 5.2 By Functionality

- 5.2.1 Vendor Management System (VMS)

- 5.2.2 Contractor Lifecycle Management

- 5.2.3 Talent Sourcing and Direct Sourcing Integration

- 5.2.4 Compliance and Risk Management

- 5.2.5 Spend Management and Rate Benchmarking

- 5.2.6 Other Functionalities

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises

- 5.5 By End-User Industry

- 5.5.1 Information Technology and Telecommunications

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Manufacturing

- 5.5.5 Retail and E-commerce

- 5.5.6 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Beeline

- 6.4.2 Magnit, LLC

- 6.4.3 Avature Limited

- 6.4.4 CXC Global

- 6.4.5 Worksuite Inc.

- 6.4.6 VectorVMS1 LLC

- 6.4.7 Pixid

- 6.4.8 Eqip AG

- 6.4.9 Netive VMS

- 6.4.10 Prosperix

- 6.4.11 Ceipal Corp.

- 6.4.12 Flextrack Inc.

- 6.4.13 Simplify Workforce

- 6.4.14 StafferLink

- 6.4.15 Trio Workforce Solutions

- 6.4.16 Flentis Corporation

- 6.4.17 DirectSkills

- 6.4.18 Worksome ApS

- 6.4.19 MBO Partners

- 6.4.20 3 Story Software LLC

- 6.4.21 i-Resource Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment