PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065445

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065445

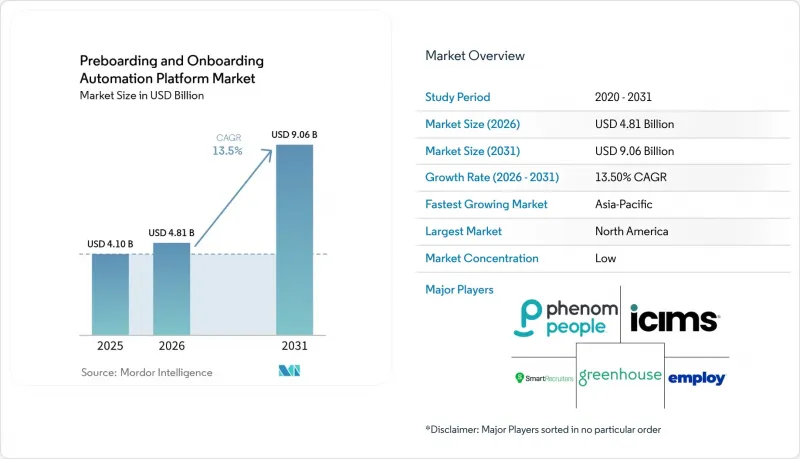

Preboarding And Onboarding Automation Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the preboarding and onboarding automation platform market size is projected to expand from USD 4.10 billion in 2025 and USD 4.81 billion in 2026 to USD 9.06 billion by 2031, registering a CAGR of 13.50% between 2026 and 2031.

This report is Segmented by Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and More), End-User Industry (BFSI, Healthcare and Life Sciences, and More), Functionality (Recruitment-To-Preboarding Automation, Documentation and Verification, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Preboarding And Onboarding Automation Platform Market Trends and Insights

Shift from Manual HR Workflows to Digital Employee Journeys

The move from manual coordination to structured digital workflows remains the clearest growth driver in the preboarding and onboarding automation platform market. Older onboarding routines relied on email follow-ups, disconnected checklists, and separate actions from HR, IT, legal, and facilities, which made delays hard to avoid as hiring volumes rose. Employers now want one workflow that starts as soon as the offer is accepted and continues through documentation, access setup, and first-day readiness. As these steps are brought together, buyers gain clearer visibility into completion gaps and early experience signals, making onboarding more useful for retention management, not just administration. Vendors that can tie workflow completion to faster readiness and measurable cost savings are gaining stronger buyer attention in the preboarding and onboarding automation platform market.

Hybrid and Distributed Hiring Expands Pre-Day-One Automation Needs

Hybrid and remote work changed what preboarding must complete before day one in the preboarding and onboarding automation platform market. New hires, managers, and verification contacts are often not in the same place, so document collection, equipment coordination, communication, and readiness tasks need to run asynchronously. That makes fixed office-based onboarding routines much less effective than they were in earlier hiring models. More than 70% of the workforce is expected to work remotely at least 5 days per month by the end of 2026, which keeps demand high for geography-aware onboarding flows. Vendors that let employers adapt tasks by country, legal entity, and manager without rebuilding the workflow each time are in a stronger position in the market for preboarding and onboarding automation platforms.

Fragmented Legacy HR Stacks Slow End-To-End Workflow Orchestration

Fragmented HR environments remain the most persistent operational restraint in the preboarding and onboarding automation platform market. Many employers still run recruiting, HR, payroll, benefits, learning, and identity tasks across systems acquired at different times and not built to work as a single architecture. In that setting, the main bottleneck is often the system connection point and not the workflow design itself. SAP's 2026 integration messaging highlighted the significant manual re-entry that existed before shared data flow was established across hiring and onboarding tasks, underscoring why disconnected stacks continue to delay value realization. The result is longer implementation cycles, heavier service requirements, and slower time-to-value for buyers in the preboarding and onboarding automation platform market.

Other drivers and restraints analyzed in the detailed report include:

- Compliance Automation Demand Across Labor, Privacy, and Hiring Rules

- Platform Consolidation Across ATS, HRIS, Payroll, and Experience Layers

- Budget Scrutiny And Longer HR Tech Payback Hurdles In SMBs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment accounted for 68.41% of revenue in 2025, making it the leading model in the preboarding and onboarding automation platform market. Buyers favored cloud platforms because they can connect more easily across ATS, HRIS, and payroll without requiring new on-premises infrastructure. On-premises deployment remained relevant in a narrower set of regulated environments where data control and internal hosting still carry more weight than flexibility. Hybrid deployment is projected to expand at a 16.47% CAGR through 2031, which makes it the fastest-growing model in this preboarding and onboarding automation platform market.

This pattern reflects the fact that many global employers want to modernize onboarding workflows without replacing the full HR backbone they already run. A hybrid setup lets them keep the core system of record in place while adding cloud-based experience and compliance layers on top. SAP's March 2026 integration work with SmartRecruiters and SuccessFactors demonstrated how a connected flow between recruiting and onboarding can reduce manual re-entry during this transition model. Within the preboarding and onboarding automation platform industry, vendors that support both stable system-of-record operations and flexible workflow orchestration are in the strongest position.

Large enterprises accounted for 62.37% of revenue in 2025, making them the largest buyer group in the preboarding and onboarding automation platform market. Their scale, multi-entity hiring needs, and greater compliance exposure make end-to-end workflow automation easier to justify. A Fortune 500 manufacturing case documented annual savings of more than USD 400,000 and more than 5x ROI after automation was applied across divisions. Small and medium-sized businesses are projected to grow at a 17.83% CAGR through 2031, which shows that adoption is broadening beyond the largest employers.

SMB growth is being helped by PEPM-priced offerings, no-code workflow builders, and bundled compliance libraries that reduce the entry barrier. At the same time, these buyers still expect faster activation and greater vendor support because they often lack dedicated HR technology teams. Intuit's move into connected HR automation through GoCo also supports the view that smaller employers want unified payroll, HR, and onboarding coverage rather than a collection of separate tools. The preboarding and onboarding automation platform industry is therefore seeing the gap narrow between what large enterprises and SMBs expect from day-zero readiness, even if the buying path remains easier for larger accounts.

Geography Analysis

North America accounted for 39.61% of global revenue in 2025, making it the largest regional market for preboarding and onboarding automation platforms. The region benefits from mature HR software adoption, a high level of remote and hybrid hiring, and a compliance environment that pushes employers toward audit-ready workflows. The United States is now being shaped by the March 2026 ICE revision to the substantive violation standards for Form I-9. Remote-verification errors, including failure to mark the alternative procedure checkbox and failure to meet E-Verify requirements while using remote document examination, can now trigger direct penalty exposure of up to USD 2,861 per form. That shift is increasing demand for remote I-9 and E-Verify-enabled workflows as standard product features in the preboarding and onboarding automation platform market.

Europe is shaped by GDPR handling requirements and the wider governance burden created by the EU AI Act. Germany remains the most regulation-heavy environment because employment data rules and works council consultation can affect how AI-enabled onboarding systems are deployed. Article 26(7) worker notification obligations remain relevant from August 2026, which adds disclosure steps that platforms must support in employee-facing flows. The UK follows its own right-to-work verification path, while South America remains earlier stage and is still led mainly by multinational rollouts rather than domestic-first deployments.

Asia-Pacific is projected to expand at a 14.71% CAGR through 2031, which makes it the fastest-growing region in the preboarding and onboarding automation platform market. Growth is being supported by HR digitization in India, Australia, South Korea, and Singapore. Singapore's Employment Pass process and the Philippines' multi-agency statutory enrollment needs create clear demand for localized workflow templates. Japan and China remain large untapped opportunities, but both require stronger localization around language, data control, and communication patterns. The Middle East and Africa add concentrated demand, driven by Saudi Arabia, the UAE, South Africa, and Nigeria, where multinational subsidiaries and regional technology employers are adopting cloud-first onboarding systems.

- Phenom People, Inc.

- iCIMS, Inc.

- Greenhouse Software, Inc.

- SmartRecruiters, Inc.

- Employ, Inc.

- Lever, Inc.

- ClearCompany, LLC

- Bamboo HR LLC

- GoCo.io, Inc.

- Namely, Inc.

- Talentech Group AS

- Tribepad Ltd

- EMP Trust Solutions, LLC

- Click Boarding, LLC

- Enboard.Me Pty Ltd.

- WorkBright

- NEO Global Pty Ltd.

- Affirm Software Group Pty Ltd.

- HROnboard Pty Ltd.

- Onboarded Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift From Manual HR Workflows to Digital Employee Journeys

- 4.2.2 Hybrid and Distributed Hiring Expands Pre-Day-One Automation Needs

- 4.2.3 Compliance Automation Demand Across Labor, Privacy, and Hiring Rules

- 4.2.4 Platform Consolidation Across ATS, HRIS, Payroll, and Experience Layers

- 4.2.5 HR-To-IT Identity Provisioning Becomes a Day-Zero Readiness Priority

- 4.2.6 Cross-Border Hiring Raises Need for Localized Preboarding and Right-To-Work Flows

- 4.3 Market Restraints

- 4.3.1 Fragmented Legacy HR Stacks Slow End-To-End Workflow Orchestration

- 4.3.2 Budget Scrutiny and Longer HR Tech Payback Hurdles in SMBs

- 4.3.3 EU AI Act and Worker-Notice Duties Raise Governance Burden for AI-Enabled Flows

- 4.3.4 Remote I-9 and Identity Verification Liability Keeps Regulated Employers Cautious

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-Sized Businesses

- 5.3 By End User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Information Technology and Telecom

- 5.3.4 Retail and E-commerce

- 5.3.5 Industrial Manufacturing

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-user Industries

- 5.4 By Functionality

- 5.4.1 Recruitment-to-Preboarding Automation

- 5.4.2 Documentation and Verification

- 5.4.3 Compliance and Identity Governance

- 5.4.4 IT Provisioning and Workspace Enablement

- 5.4.5 Learning and Productivity Enablement

- 5.4.6 Employee Experience and Journey Management

- 5.4.7 Workforce Analytics and Intelligence

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Netherlands

- 5.5.2.8 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Phenom People, Inc.

- 6.4.2 iCIMS, Inc.

- 6.4.3 Greenhouse Software, Inc.

- 6.4.4 SmartRecruiters, Inc.

- 6.4.5 Employ, Inc.

- 6.4.6 Lever, Inc.

- 6.4.7 ClearCompany, LLC

- 6.4.8 Bamboo HR LLC

- 6.4.9 GoCo.io, Inc.

- 6.4.10 Namely, Inc.

- 6.4.11 Talentech Group AS

- 6.4.12 Tribepad Ltd

- 6.4.13 EMP Trust Solutions, LLC

- 6.4.14 Click Boarding, LLC

- 6.4.15 Enboard.Me Pty Ltd.

- 6.4.16 WorkBright

- 6.4.17 NEO Global Pty Ltd.

- 6.4.18 Affirm Software Group Pty Ltd.

- 6.4.19 HROnboard Pty Ltd.

- 6.4.20 Onboarded Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment