PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065451

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065451

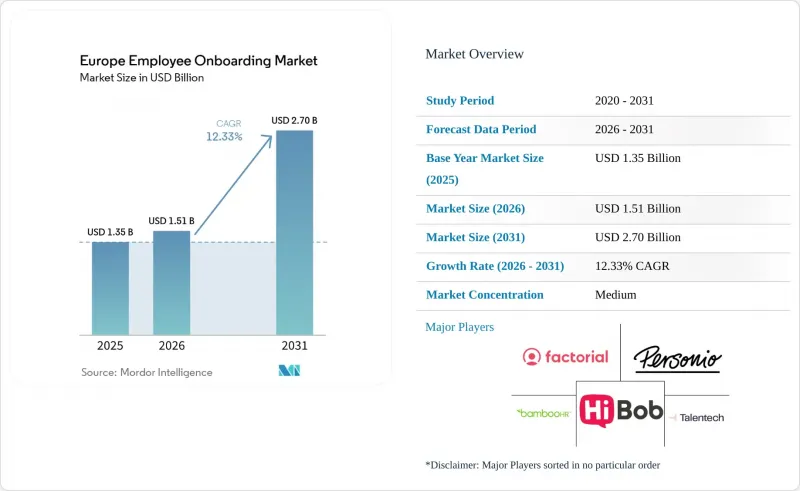

Europe Employee Onboarding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe employee onboarding market size is projected to be USD 1.35 billion in 2025, USD 1.51 billion in 2026, and reach USD 2.70 billion by 2031, growing at a CAGR of 12.33% from 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud-Based, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), Functionality (Workflow Automation and Task Orchestration, Document Management and E-Signature, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Employee Onboarding Market Trends and Insights

Rising Demand for GDPR-Compliant and Multilingual Onboarding

European employers increasingly want onboarding systems that create a defensible record of consent, data minimization, and deletion handling, rather than tools that only automate forms and reminders. That requirement matters more in the Europe employee onboarding market because a single hiring process may involve several labor regimes, languages, and internal reviewers before a new hire is active. Vendors that built field-level encryption, tenant separation, and records support into their core architecture are taking share from generic HR products that treated privacy compliance as an afterthought. The multilingual requirement adds another layer of buyer urgency because employers operating across Germany, France, Spain, and the Netherlands need contracts, policies, and training content in local languages without maintaining manual versions of these documents. Digital adoption is still uneven across Europe, leaving room for GDPR-native platforms to replace manual workflows over time. 52.7% of EU enterprises used paid cloud computing services in 2025, and adoption still varied widely by enterprise type and country, according to EUROSTAT. That combination of privacy depth and language localization is giving specialized vendors a durable edge in the Europe employee onboarding market when procurement teams evaluate long-term compliance risk.

Shift From Manual HR Administration to Automated Workflow Orchestration

Operational breakdowns in sequential task handling are driving the automation case in Europe, because new-hire readiness depends on HR, IT, payroll, legal, and line managers acting simultaneously rather than in sequence. In the Europe employee onboarding market, a contract signature is increasingly expected to trigger downstream actions such as laptop provisioning, payroll setup, compliance enrollment, and manager notifications without manual chasing. That model aligns with the wider enterprise technology base now in place across Europe, where 52.7% of EU enterprises used paid cloud services in 2025, and 85% of large enterprises had already adopted cloud services. The practical effect is that onboarding ROI is no longer judged solely within HR, because delays in IT provisioning and identity setup are counted as real business costs at the point of deployment. Vendors that can sit above the ATS, HRIS, payroll, and IT stack, rather than asking buyers to replace them, are gaining traction because this lowers implementation risk within existing enterprise architectures. The Europe employee onboarding market is therefore rewarding orchestration layers that simplify task routing across systems rather than platforms that depend on a full replacement strategy.

Integration Complexity Across ATS, HRIS, Payroll, and IT Systems

The biggest operational drag on adoption is not software selection, but the difficulty of connecting the onboarding layer to fragmented enterprise systems that were never designed to share data in a common format. In the Europe employee onboarding market, a multinational employer may use a single ATS, a single core HR system, different payroll providers by country, and a separate IT provisioning stack, which makes implementation a multi-stream integration project. When candidate data must be translated from the ATS into a new hire record, then again into payroll and IT systems, the cost and delay can become disproportionate to the platform license itself. Germany adds a specific friction point because DATEV remains deeply embedded in the Mittelstand payroll environment and often requires certified interface partners rather than generic API links. Data-model mismatches, such as different employee ID structures or classification rules, then force manual reconciliation, which puts administrative work back into a process the software was meant to simplify. The Europe employee onboarding market is favoring vendors that bring certified connectors to systems such as Workday, SAP SuccessFactors, DATEV, and AFAS because buyers want faster deployment and lower professional services exposure.

Other drivers and restraints analyzed in the detailed report include:

- Stronger Focus on Early Retention and Employee Experience

- Need To Coordinate HR, IT, and Compliance Tasks in One Workflow

- Budget and Change-Management Friction Among Small and Medium-Sized Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment held 68.41% of the Europe employee onboarding market size in 2025, while hybrid is projected to expand at a 13.82% CAGR through 2031. That lead reflected years of investment by European employers in SaaS platforms that package GDPR data residency, security certifications, and workflow tools as standard capabilities rather than optional add-ons. The Europe employee onboarding market still benefits from a favorable infrastructure base, as 52.7% of EU enterprises used paid cloud services in 2025, up 7.4 percentage points from 2023. The same dataset showed that cloud adoption among large enterprises had already reached 85%, which helps explain why higher-value buyers remain comfortable with hosted delivery models. Cloud, therefore, remained the default choice for organizations seeking faster deployment, lower internal maintenance costs, and easier multi-country rollouts within a single platform.

Hybrid, however, is growing faster because many employers are not abandoning cloud strategy; they are adapting it to regulated operating conditions and legacy system realities. In the Europe employee onboarding industry, hybrid design lets employers keep sensitive identity, document, or payroll steps in tightly controlled environments while still using SaaS workflows for collaboration and progress management. That approach fits sectors where sovereign hosting obligations, internal security policies, or critical infrastructure rules make a full cloud migration difficult to approve. It also suits enterprises that already invested heavily in on-premises HR or IT stacks and now want a layered transition rather than a disruptive replacement. The Europe employee onboarding market is therefore rewarding vendors that can support cloud, hybrid, and on-premises paths without forcing buyers into a single architecture that ignores procurement and compliance constraints.

Large enterprises accounted for 61.29% of the Europe employee onboarding market size in 2025, while SMEs are projected to grow at a 15.47% CAGR through 2031. Large organizations held the lead because they face the hardest coordination burden, including cross-border hiring, multi-language contract generation, works council obligations, and deep integration across HR, payroll, identity, and compliance systems. In practical terms, structured onboarding for these employers is less a discretionary software purchase and more a control layer that reduces errors across complex hiring operations. The Europe employee onboarding market also remains enterprise-led because large buyers have budget capacity to absorb implementation services, policy redesign, and manager training alongside the software license. That scale advantage keeps enterprise demand strong even as vendors simplify implementation and broaden self-service features.

The faster expansion in SMEs reflects a different set of conditions, centered on lower entry barriers and a clearer link between onboarding quality and avoidable turnover. A 2025 survey showed that 20.5% of HR leaders said up to 50% of new hires left within the first 90 days, which makes even a smaller software investment easier to justify when early exits are frequent. A 2026 publication also showed that SME cloud adoption still trailed that of large enterprises by a wide margin, indicating substantial room for first-time digitalization across the smaller employer base. As pricing falls and setup becomes easier through templates and guided configuration, the Europe employee onboarding industry is turning SMEs from a peripheral segment into a core expansion field. That shift matters because vendors that win early among smaller employers can create long customer lifecycles before those organizations move into more complex workforce and compliance needs.

List of Companies Covered in this Report:

- BambooHR LLC

- Hi Bob Limited

- Personio SE and Co. KG

- Deel, Inc.

- Enboarder Pty Ltd.

- Click Boarding, LLC

- Jobvite, Inc.

- Greenhouse Software, Inc.

- ClearCompany, LLC

- Leapsome GmbH

- Zavvy GmbH

- Appical B.V.

- Talentech Group AS

- HR-ON ApS

- Valamis Group Oy

- WorkMotion Software GmbH

- Employment Hero Pty Ltd.

- Factorial HR, S.L.

- Teamtailor AB

- Abacus Umantis AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand For GDPR-Compliant and Multilingual Onboarding

- 4.2.2 Shift From Manual HR Administration To Automated Workflow Orchestration

- 4.2.3 Stronger Focus On Early Retention and Employee Experience

- 4.2.4 Need To Coordinate HR, IT, and Compliance Tasks In One Workflow

- 4.2.5 EU Pay Transparency Directive Readiness Reshaping Hiring and Onboarding Data Flows

- 4.2.6 EUDI Wallet and Verified Digital Credential Adoption For Faster Identity Checks

- 4.3 Market Restraints

- 4.3.1 Integration Complexity Across HR/IT Systems

- 4.3.2 SME Budget and Change-Management Limits

- 4.3.3 Works Council and Labor Rule Delays

- 4.3.4 Data Sovereignty Narrowing Vendor Pools

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-based

- 5.1.2 On-premises

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-sized Enterprises

- 5.3 By End User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Information Technology and Telecom

- 5.3.4 Retail and E-commerce

- 5.3.5 Industrial Manufacturing

- 5.3.6 Government and Public Sector

- 5.3.7 Other End-user Industries

- 5.4 By Functionality

- 5.4.1 Workflow Automation and Task Orchestration

- 5.4.2 Document Management and E-signature

- 5.4.3 Learning and Training Management

- 5.4.4 Compliance and Policy Acknowledgment

- 5.4.5 Analytics and Progress Tracking

- 5.4.6 Employee Self-service and Communication

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Russia

- 5.5.7 Netherlands

- 5.5.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 BambooHR LLC

- 6.4.2 Hi Bob Limited

- 6.4.3 Personio SE and Co. KG

- 6.4.4 Deel, Inc.

- 6.4.5 Enboarder Pty Ltd.

- 6.4.6 Click Boarding, LLC

- 6.4.7 Jobvite, Inc.

- 6.4.8 Greenhouse Software, Inc.

- 6.4.9 ClearCompany, LLC

- 6.4.10 Leapsome GmbH

- 6.4.11 Zavvy GmbH

- 6.4.12 Appical B.V.

- 6.4.13 Talentech Group AS

- 6.4.14 HR-ON ApS

- 6.4.15 Valamis Group Oy

- 6.4.16 WorkMotion Software GmbH

- 6.4.17 Employment Hero Pty Ltd.

- 6.4.18 Factorial HR, S.L.

- 6.4.19 Teamtailor AB

- 6.4.20 Abacus Umantis AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment