PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065491

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065491

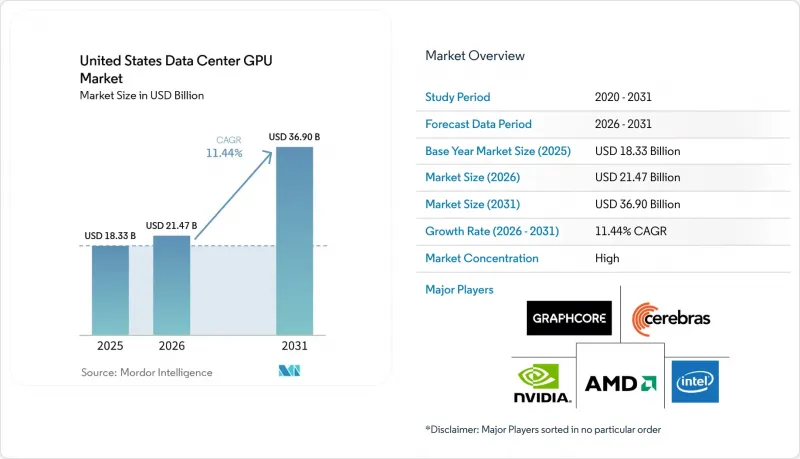

United States Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states data center GPU market size was valued at USD 18.33 billion in 2025 and estimated to grow from USD 21.47 billion in 2026 to reach USD 36.90 billion by 2031, at a CAGR of 11.44% during the forecast period (2026-2031).

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise / Private Data Centers, and More), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and More), and End-User (Hyperscalers/CSPs, Enterprises, and More). The Market Forecasts are Provided in Value (USD).

United States Data Center GPU Market Trends and Insights

Growing AI Model Complexity Driving GPU Refresh Cycles

Trillion-parameter transformers now demand rack-scale clusters with aggregate memory exceeding 10 TB, pushing hyperscalers to retire Hopper systems after roughly 18 months and to accelerate Blackwell and Rubin procurement cycles. NVIDIA's Vera Rubin NVL72 couples 72 Rubin GPUs with 36 Vera CPUs, delivering a 3.6 TB/s interconnect that cuts GPU counts by one-quarter per petaflop. Continuous agentic workloads have shifted spending from one-time training bursts to always-on inference fleets, favoring reserved-instance contracts over spot pricing. OpenAI's multi-year wafer-scale deal demonstrates how model providers can lock in capacity years in advance. The result is a shortened refresh cadence that strengthens secondary markets for lightly used GPUs.

Escalating Energy Efficiency Mandates Favoring Advanced GPUs

The Environmental Protection Agency's ENERGY STAR v4.0 caps idle power and targets PUE below 1.3, disadvantaging legacy Pascal and Volta cards. Department of Energy guidelines now require quarterly reporting of GPU utilization, nudging agencies toward Blackwell and Rubin devices that quadruple FP8 performance per watt. California Title 24, effective January 2026, mandates GPU fleet averages of 50 TFLOPS per kilowatt, a level only liquid-cooled Blackwell and AMD MI400 systems meet. Colocation providers are retrofitting with direct-to-chip liquid cooling, raising rent premiums in Northern Virginia and Phoenix. Together, federal and state rules are splitting the market into legacy air-cooled sites and next-generation liquid-cooled campuses.

Supply Chain Constraints for Advanced Packaging Substrates

TSMC's CoWoS capacity remains capped at around 30,000 wafers per month until at least 2027, slowing Blackwell and Rubin's output. SK hynix experienced HBM3e yield issues in 2025, delaying shipments by up to 12 weeks. ASML delivery backlogs limit advanced-node expansion despite multibillion-dollar fab projects. Micron entered HBM production in late 2025, yet early volumes are targeted at mobile rather than data center demand. Vendors therefore prioritize the highest-margin rack-scale systems, leaving mid-market enterprises with prolonged lead times.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Edge Inference Accelerating Low-Latency GPU Demand

- Adoption of Cloud-Native HPC Workflows in Enterprise Research and Development

- Rising Total Cost of Ownership Versus ASIC Alternatives for Inference

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud data centers accounted for 64.76% of United States data center GPU revenue in 2025, yet edge data centers are forecast to grow at 12.89% annually through 2031, reflecting the migration of latency-sensitive inference workloads from centralized hyperscaler facilities to distributed edge sites. Hyperscalers such as AWS, Microsoft Azure, and Google Cloud continue to dominate capital expenditure.

NVIDIA's Omniverse on DGX Cloud, launched in February 2026 with optimized L40 GPUs for RTX rendering and low-latency streaming, targets industrial digitalization and digital twin workflows that require scalable GPU resources without customer infrastructure management, positioning cloud-managed GPU services as an on-ramp for enterprises hesitant to commit capital to on-premise clusters. Edge data centers, particularly those supporting autonomous vehicle fleets and smart manufacturing, are deploying ruggedized GPU servers with 50-150 watt thermal envelopes and passive cooling to operate in non-climate-controlled environments, a segment where NVIDIA Jetson and AMD Radeon PRO platforms compete on software ecosystem maturity and long-term supply commitments.

Training GPUs commanded 59.88% of market share in 2025, yet inference GPUs are forecast to grow at 12.77% annually through 2031 as model providers shift capital from one-time pretraining toward multi-year inference fleets that serve continuous agentic workloads. The economic logic is straightforward: a trillion-parameter model requires USD 50-100 million and 10,000-20,000 GPUs for initial training, but serving that model at scale demands 5-10x more inference capacity over its operational lifetime, fundamentally altering the capital allocation calculus for hyperscalers and model builders. NVIDIA's Groq 3 LPX inference rack, integrating 256 language processing units with 128 gigabytes of on-chip SRAM and 40 petabytes per second of aggregate bandwidth, targets low-latency token generation for agentic reasoning workloads where sub-millisecond response times unlock premium pricing tiers.

Training GPUs remain essential for foundation model development and post-training fine-tuning, yet the cadence of new model releases is slowing GPT-5 and Llama 4 training runs are stretching to 12-18 months versus 6-9 months for prior generations, reducing the urgency of continuous training cluster expansion and allowing hyperscalers to amortize training infrastructure over longer periods. The emergence of test-time compute scaling, where models iteratively refine outputs during inference rather than relying solely on pretraining scale, is blurring the boundary between training and inference workloads and driving demand for hybrid GPU architectures that support both high-throughput batch training and low-latency interactive inference.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Alphabet Inc. (Google Cloud TPU ecosystem)

- Amazon Web Services, Inc.

- Microsoft Corporation

- Meta Platforms, Inc.

- IBM Corporation

- Graphcore Ltd.

- Cerebras Systems Inc.

- Marvell Technology, Inc.

- Samsung Electronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing AI Model Complexity Driving GPU Refresh Cycles

- 4.2.2 Escalating Energy Efficiency Mandates Favoring Advanced GPUs

- 4.2.3 Proliferation of Edge Inference Accelerating Low-latency GPU Demand

- 4.2.4 Adoption of Cloud-native HPC Workflows in Enterprise R&D

- 4.2.5 Emergence of Multi-tenant GPU Virtualization Platforms

- 4.2.6 U.S. Government Incentives For Domestic Semiconductor Capacity

- 4.3 Market Restraints

- 4.3.1 Supply Chain Constraints For Advanced Packaging Substrates

- 4.3.2 Rising Total Cost of Ownership Versus ASIC Alternatives For Inference

- 4.3.3 Data Center Power and Cooling Bottlenecks in Legacy Facilities

- 4.3.4 Geopolitical Export Controls Limiting GPU Availability To Certain Users

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Alphabet Inc. (Google Cloud TPU ecosystem)

- 6.4.6 Amazon Web Services, Inc.

- 6.4.7 Microsoft Corporation

- 6.4.8 Meta Platforms, Inc.

- 6.4.9 IBM Corporation

- 6.4.10 Graphcore Ltd.

- 6.4.11 Cerebras Systems Inc.

- 6.4.12 Marvell Technology, Inc.

- 6.4.13 Samsung Electronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment