PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065548

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065548

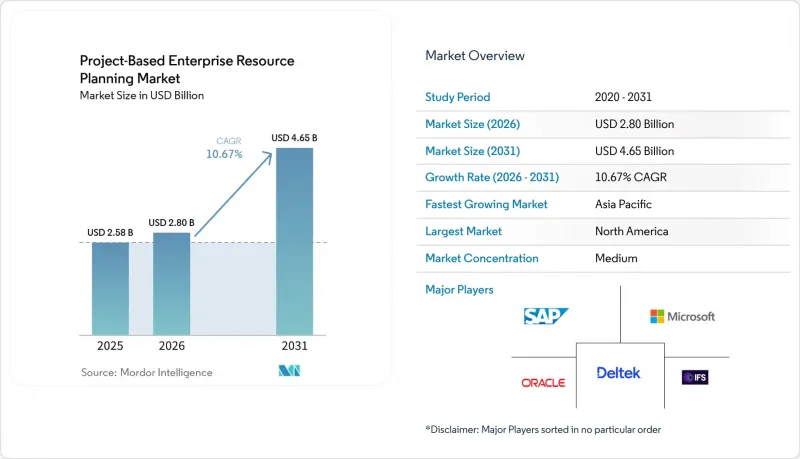

Project-Based Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the project-Based enterprise resource planning (ERP) market size is projected to expand from USD 2.58 billion in 2025 and USD 2.80 billion in 2026 to USD 4.65 billion by 2031, registering a CAGR of 10.67% during 2026-2031.

This report is Segmented by Deployment Mode (On-Premise, Cloud/SaaS, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Component (Software, and Services), End-User Industry (Construction and Engineering, Professional Services, Aerospace and Defense, Government and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Project-Based Enterprise Resource Planning Market Trends and Insights

Adoption Of Remote Work And Distributed Project Teams

Remote and hybrid work models became permanent in 2025, forcing companies to retire on-premises systems that rely on VPN access and desktop clients. Cloud-native Project-Based ERP market platforms now ship with mobile interfaces that let field engineers submit timecards and approve change orders from any device, cutting approval cycles by 40% in aerospace and professional-services pilots. Billable utilization climbs when time entries are captured within hours, protecting margins that would otherwise be eroded by manual delays. Buyers increasingly prefer vendors that embed chat, document management, and workflow approvals directly inside the ERP rather than through third-party tools. This consolidation simplifies user training and reduces integration overhead, making remote collaboration a key purchase criterion. As a result, solution providers that optimize experiences for distributed teams are winning competitive bids.

Transition To SaaS And Subscription-Based Pricing Models

The Project-Based ERP market is shifting decisively toward subscription contracts as vendors announce sunset dates for on-premises releases. Epicor's January 2026 roadmap gives customers four years to migrate, a deadline that compresses decision cycles and accelerates cloud adoption. SaaS eliminates server hardware costs, yet it converts capital expenditure into recurring operating expense that can exceed perpetual-license amortization over long horizons. Firms that value continuous feature updates and elastic user scaling find the trade-off attractive, whereas organizations with stable headcounts must carefully evaluate lifetime subscription totals. Migration windows are pushing even risk-averse industries to accelerate data-conversion projects, reinforcing double-digit growth in cloud revenue across the Project-Based ERP market.

High Switching Costs From Legacy ERP Platforms

Migrating historical data, rebuilding custom integrations, and training users can consume 18-24 months and overrun budgets by 30% in complex carve-outs. A mid-sized engineering firm replacing a 15-year-old Deltek instance must map legacy cost codes and maintain audit trails for active contracts during cutover. NetSuite's SuiteSuccess and Unit4's low-code configuration help compress timelines, yet the investment hurdle deters risk-averse CFOs. Until accelerated implementation frameworks prove reliable at scale, high switching costs will temper adoption velocity in parts of the Project-Based ERP market.

Other drivers and restraints analyzed in the detailed report include:

- Integration Of AI-Driven Project Analytics

- Growing Complexity Of Compliance In Project Accounting

- Shortage Of Skilled Project-ERP Implementation Specialists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid configurations are expanding at 17.80% CAGR through 2031 as enterprises pair private-cloud databases with public-cloud collaboration modules. Cloud installations captured 52.12% of the Project-Based ERP market share in 2025, confirming buyer confidence in vendor-managed security and automatic upgrades. A construction conglomerate might hold sensitive financials on private infrastructure but place mobile field-service and analytics workloads in public SaaS to support site engineers. The Project-Based ERP market size for on-premises deployments is shrinking as vendors limit innovation to cloud editions, yet it persists in defense and critical infrastructure accounts that require air-gapped networks.

Organizations choosing deployment models assess total cost across subscription, data egress, and integration charges versus the flexibility to scale. Microsoft's tiered Dynamics 365 options and SAP's RISE program encourage phased migrations that reduce operational risk. Hybrid offerings that allow incremental module shifts appeal to firms burdened by heavily customized legacy stacks. Consequently, hybrid remains the fastest-growing slice of the Project-Based ERP market as businesses seek both compliance and rapid innovation.

Large enterprises held a 60.29% share of the Project-Based ERP market in 2025, yet small and medium enterprises are growing at a 15.60% CAGR through 2031. Subscription pricing removes capital barriers: a 200-person architectural firm can deploy core modules for USD 50,000-100,000 in year one, a fifth of historical on-premises costs. Net at Work's January 2026 purchase of BHE Consulting underscores integrator interest in mid-market growth. Modular licensing lets SMEs add procurement or analytics when revenue allows, aligning software expense with contract inflows.

Professional services, construction, and IT consultancies lead adoption because margins depend on real-time capture and prompt billing. Currency fluctuations and macroeconomic volatility still curb adoption in South America and Africa, but vendors that offer flexible payment terms and regionally hosted data centers are reducing barriers. As capabilities once reserved for global enterprises become accessible, SMEs will exert growing influence on functional roadmaps within the Project-Based ERP market.

Geography Analysis

North America accounted for 34.26% of the Project-Based ERP market revenue in 2025, owing to mature ecosystems, high IT budgets, and a concentration of defense and professional services. U.S. federal agencies adopted enterprise project management software to track capital programs, while Canadian and Mexican manufacturers integrated ERP systems to coordinate nearshore supply chains. A deep bench of certified consultants and early AI experimentation helps the region maintain leadership.

Asia-Pacific is growing fastest, with a 13.70% CAGR through 2031. China's Belt and Road projects, India's electronic invoicing mandates, and ASEAN manufacturing expansion are fueling robust demand. Australia and New Zealand have high deployment rates in mining, and Japan is upgrading its ERP systems to support smart-factory initiatives. Talent shortages and diverse data-residency laws are driving regional cloud zones and accelerating hybrid models.

Europe balances opportunity with regulatory headwinds. GDPR, sustainability reporting, and the Medical Device Regulation elevate compliance requirements, steering buyers toward platforms with built-in audit capabilities. Germany, the United Kingdom, France, and Italy dominate spend across automotive, aerospace, and engineering. The Middle East invests in megaprojects tied to diversification agendas, seeking ERP that supports joint ventures and Islamic finance. South American growth is localized to Brazil and Argentina due to currency volatility, and Africa's uptake is led by South Africa and Nigeria in mining and telecom despite infrastructure gaps.

- Deltek, Inc.

- IFS AB

- Unit4 N.V.

- Oracle Corporation

- SAP SE

- Microsoft Corporation

- Infor, Inc.

- Epicor Software Corporation

- Workday, Inc.

- Acumatica, Inc.

- Ramco Systems Limited

- SYSPRO (Proprietary) Limited

- Priority Software Ltd.

- QAD Inc.

- Sage Group plc

- Totvs S.A.

- NetSuite Inc.

- FinancialForce.com, Inc.

- Aptean, Inc.

- Plex Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of Remote Work and Distributed Project Teams

- 4.2.2 Transition to SaaS and Subscription-Based Pricing Models

- 4.2.3 Integration of AI-Driven Project Analytics

- 4.2.4 Growing Complexity of Compliance in Project Accounting

- 4.2.5 Demand for Unified Bid-to-Cash Visibility Across Projects

- 4.2.6 Rising Investment in Public Infrastructure Megaprojects

- 4.3 Market Restraints

- 4.3.1 High Switching Costs from Legacy ERP Platforms

- 4.3.2 Shortage of Skilled Project-ERP Implementation Specialists

- 4.3.3 Data Security Concerns in Multi-Tenant Cloud Environments

- 4.3.4 Budget Constraints in SMEs Amid Macroeconomic Uncertainty

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud/SaaS

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Component

- 5.3.1 Software

- 5.3.2 Services

- 5.4 By End-User Industry

- 5.4.1 Construction and Engineering

- 5.4.2 Professional Services

- 5.4.3 Aerospace and Defense

- 5.4.4 Government and Utilities

- 5.4.5 Healthcare

- 5.4.6 IT and Telecom

- 5.4.7 Manufacturing

- 5.4.8 Oil and Gas

- 5.4.9 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Deltek, Inc.

- 6.4.2 IFS AB

- 6.4.3 Unit4 N.V.

- 6.4.4 Oracle Corporation

- 6.4.5 SAP SE

- 6.4.6 Microsoft Corporation

- 6.4.7 Infor, Inc.

- 6.4.8 Epicor Software Corporation

- 6.4.9 Workday, Inc.

- 6.4.10 Acumatica, Inc.

- 6.4.11 Ramco Systems Limited

- 6.4.12 SYSPRO (Proprietary) Limited

- 6.4.13 Priority Software Ltd.

- 6.4.14 QAD Inc.

- 6.4.15 Sage Group plc

- 6.4.16 Totvs S.A.

- 6.4.17 NetSuite Inc.

- 6.4.18 FinancialForce.com, Inc.

- 6.4.19 Aptean, Inc.

- 6.4.20 Plex Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment