PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065546

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065546

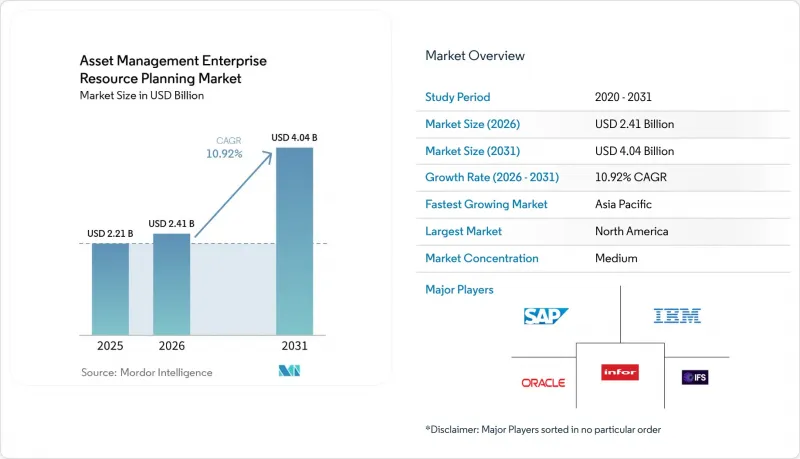

Asset Management Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asset management enterprise resource planning (ERP) market size is expected to grow from USD 2.21 billion in 2025 to USD 2.41 billion in 2026 and is forecast to reach USD 4.04 billion by 2031 at 10.92% CAGR over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises, and SMEs), Application Vertical (Manufacturing, Energy and Utilities, Healthcare, and More), Module and Functionality (Asset Lifecycle Management, Work Order Management, Inventory and Spare Parts Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Asset Management Enterprise Resource Planning Market Trends and Insights

Rapid Migration to Cloud-Based Deployment Models

Cloud-native suites let enterprises offload infrastructure, accelerate feature delivery, and align expenses with consumption. Cloud ERP spending will shift toward AI-enabled solutions by 2027, highlighting a pivot toward platforms that embed machine learning into valuation and depreciation workflows. According to NetSuite, Hybrid architectures remain prevalent, with 88% of organizations retaining sensitive ledgers on private clouds while scaling analytics in the public cloud. Containerization has been adopted in significant production environments, making asset modules portable across clouds and simplifying disaster recovery. However, several percent of enterprises have repatriated workloads amid unforeseen costs, underscoring the need for FinOps governance and automated cost controls. Overall, cloud acceleration is unlocking rapid IoT integration and predictive analytics, making it the largest single growth lever for the Asset Management Enterprise Resource Planning (ERP) market.

Growing Adoption of IoT Sensors Enabling Predictive Maintenance

IEEE case studies confirm that sensor-to-ERP integration automates maintenance request processing and failure threshold alerts, reducing manual entry and enabling predictive workflows. Utilities are early adopters: DNV's Cascade links SCADA historians to asset scores, while SAS analytics detect turbine anomalies to enable proactive scheduling. Security remains a hurdle because most IoT devices lack agents and ship with default credentials, forcing enterprises to rely on micro-segmentation and network detection to safeguard ERP interfaces. As coverage gaps close, predictive maintenance will continue to outpace other modules within the Asset Management Enterprise Resource Planning (ERP) market.

High Upfront Integration Cost with Legacy ERP Systems

Decades of custom code and undocumented interfaces make modernization expensive. Process-mining tools reveal hidden inefficiencies: production often lags records by two days, and BOMs misstate changeover rules, underscoring the need for master-data remediation before go-live. Organizations that neglect this step risk automating poor workflows and eroding the ROI of the Asset Management Enterprise Resource Planning (ERP) market rollout.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand to Reduce Unplanned Downtime in Asset-Intensive Industries

- Convergence of EAM and Sustainability Reporting for Scope 3 Compliance

- Cybersecurity and Data-Privacy Concerns in Connected Asset Ecosystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 48.50% of the Asset Management Enterprise Resource Planning (ERP) market share in 2025, and the segment is forecast to grow at a 12.30% CAGR through 2031. Organizations prefer vendor-managed infrastructure and rapid feature releases, while containerized microservices improve portability for hybrid strategies. The Asset Management Enterprise Resource Planning (ERP) market size attached to cloud deployments will expand as AI-enabled services move maintenance analytics and carbon accounting closer to compute power.

On-premise solutions persist where latency and data-sovereignty mandates prevail, especially in defense and heavily regulated utilities. Hybrid models, now embraced by 88% of enterprises, balance these constraints by keeping sensitive ledgers on private clouds and using public regions for scaling analytics. FinOps guardrails are becoming standard because 54% of enterprises cannot accurately track cloud spend, threatening to offset savings from hardware avoidance. Overall, the deployment choice now hinges more on regulatory and latency considerations than on technical capability differentials.

Large enterprises accounted for 60.30% of 2025 revenue, but small and medium enterprises are expanding at a 11.60% CAGR as vendors roll out consumption-based pricing, low-code templates, and managed services. The Asset Management Enterprise Resource Planning (ERP) market size accruing to SMEs will benefit from easier onboarding and reduced capital expenditure.

Resource constraints still challenge SMEs, yet SaaS suites that bundle finance, supply chain, and asset modules with automated master-data cleansing narrow the capability gap. In APAC and South America, cloud-first government incentives and currency-hedged subscription offers further lower adoption barriers. As usage-based pricing matures, SMEs are expected to drive a larger share of incremental demand over the forecast period.

Geography Analysis

North America accounted for 33.40% of 2025 revenue, supported by mature cloud infrastructure and early adoption of AI-driven analytics. Migration from SAP ECC to S/4HANA before the 2027 deadline is accelerating deals, though data-cleansing complexity is stretching timelines. The extraterritorial reach of the EU Cyber Resilience Act is prompting U.S. vendors to harden their products preemptively, embedding vulnerability-reporting and SBOM features to maintain European market access.

Asia-Pacific, the fastest-growing region at 11.40% CAGR, benefits from large-scale infrastructure investment in China and India and semiconductor capacity expansion backed by private commitments exceeding USD 500 billion. SMEs across Southeast Asia are leveraging subscription licensing to access enterprise-grade functionality without capital strain, further lifting regional demand.

Europe faces stringent cybersecurity and sustainability requirements, making integrated compliance features a must-have. The Middle East and Africa and South America remain nascent but promising. UAE conglomerates rolling out Infor M3 and Brazilian mid-market manufacturers adopting NetSuite SaaS platforms reflect rising interest where cloud regions and foreign-exchange-hedged pricing mitigate macro risks. Government cloud-first mandates, such as Kenya's trusted data zone projects, illustrate how sovereign-cloud provisions unlock adoption among state-owned utilities and transportation agencies. Absent major economic shocks, regional uptake is expected to broaden steadily through 2031.

- IBM Corporation

- SAP SE

- Oracle Corporation

- Infor, Inc.

- IFS AB

- Hexagon AB

- ABB Ltd.

- Aptean, Inc.

- CGI Inc.

- CMMS Data Group, Inc.

- Ramco Systems Limited

- IPS Intelligent Process Solutions GmbH

- AVEVA Group plc

- Bentley Systems, Incorporated

- ServiceNow, Inc.

- UpKeep Technologies, Inc.

- Asset Panda, Inc.

- AssetWorks LLC

- Fluke Corporation

- Trimble Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Migration to Cloud-Based Deployment Models

- 4.2.2 Growing Adoption of IoT Sensors Enabling Predictive Maintenance

- 4.2.3 Rising Demand to Reduce Unplanned Downtime in Asset-Intensive Industries

- 4.2.4 Convergence of EAM and Sustainability Reporting Modules for Scope 3 Emissions Compliance

- 4.2.5 Uptake of AI-Driven Master-Data Cleansing Tools Improving ROI Acceleration

- 4.2.6 Availability of Usage-Based Subscription Pricing for Mid-Tier Manufacturers

- 4.3 Market Restraints

- 4.3.1 High Upfront Integration Cost with Legacy ERP Systems

- 4.3.2 Cybersecurity and Data-Privacy Concerns in Connected Asset Ecosystems

- 4.3.3 Shortage of Certified Asset Management ERP Implementation Specialists

- 4.3.4 Vendor Lock-In Risk Due to Proprietary Data Models and Limited Interoperability Standards

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises

- 5.3 By Application Vertical

- 5.3.1 Manufacturing

- 5.3.2 Energy and Utilities

- 5.3.3 Transportation and Logistics

- 5.3.4 Government and Public Sector

- 5.3.5 Healthcare

- 5.3.6 Other Application Verticals

- 5.4 By Module

- 5.4.1 Asset Lifecycle Management

- 5.4.2 Work Order Management

- 5.4.3 Inventory and Spare Parts Management

- 5.4.4 Predictive Maintenance

- 5.4.5 Financial Asset Accounting

- 5.4.6 Other Modules

- 5.5 BY GEOGRAPHY

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 Infor, Inc.

- 6.4.5 IFS AB

- 6.4.6 Hexagon AB

- 6.4.7 ABB Ltd.

- 6.4.8 Aptean, Inc.

- 6.4.9 CGI Inc.

- 6.4.10 CMMS Data Group, Inc.

- 6.4.11 Ramco Systems Limited

- 6.4.12 IPS Intelligent Process Solutions GmbH

- 6.4.13 AVEVA Group plc

- 6.4.14 Bentley Systems, Incorporated

- 6.4.15 ServiceNow, Inc.

- 6.4.16 UpKeep Technologies, Inc.

- 6.4.17 Asset Panda, Inc.

- 6.4.18 AssetWorks LLC

- 6.4.19 Fluke Corporation

- 6.4.20 Trimble Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment