PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065554

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065554

Blockchain-Integrated ERP - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

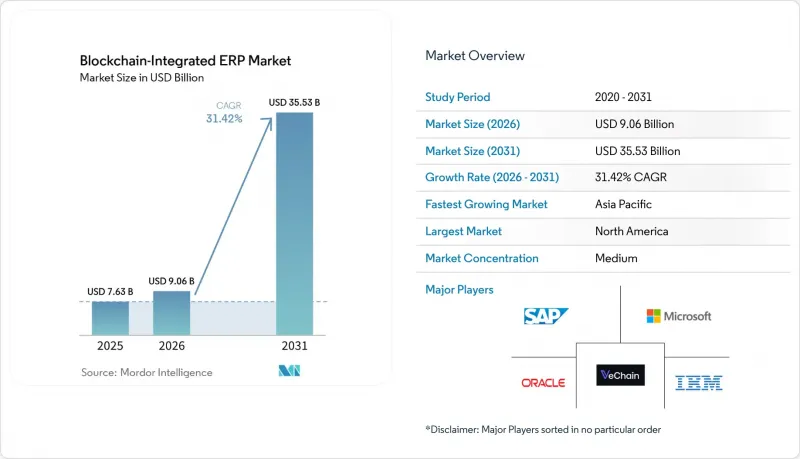

According to Mordor Intelligence, the blockchain-integrated ERP market size is expected to grow from USD 7.63 billion in 2025 to USD 9.06 billion in 2026 and is forecast to reach USD 35.53 billion by 2031 at 31.42% CAGR over 2026-2031.

This report is Segmented by Component (Platform and Services), Deployment Mode (Public, Private, and Hybrid Cloud), Enterprise Size (Large Enterprisesand SMEs), Application (Supply Chain, Financial, and Other Applications), Industry Vertical (Manufacturing, Retail and E-Commerce, BFSI, Healthcare, Transportation and Logistics Government, and More), and Geography. Market Forecasts are in Value (USD).

Global Blockchain-Integrated ERP Market Trends and Insights

Rapid Expansion of Blockchain-Enabled Supply Chain Finance Modules

Supply-chain finance modules that release working capital upon cryptographic proof of delivery are displacing traditional factoring. IBM field trials showed dispute-resolution times falling 68% and supplier cash-flow predictability improving 52%. Microsoft partnerships unlocked USD 1.2 billion of invoices for small businesses in 2025, proving blockchain credit rails can reach underserved suppliers. ConsenSys automated letter-of-credit issuance for German automotive suppliers, cutting bank fees 30%. ISO 22739 definitions will bring common semantics to trade-finance smart contracts. Because financing spreads are widest in Southeast Asia and Latin America, the impact is pronounced in regions with fragmented supply chains and scarce alternative credit.

Regulatory Mandates for Immutable Audit Trails in Highly Regulated Sectors

Markets in Crypto-Assets Regulation requires digital-asset firms to maintain tamper-proof logs, which now extend to ERP systems processing tokenized securities. The U.S. SEC's Project Crypto grants examiners read-only access to settlement ledgers. OECD's Crypto-Asset Reporting Framework compels 48 jurisdictions to submit standardized XML transaction files. FDA pilots require pharmaceutical batch events to be written on a chain. Vendors now combine off-chain data stores with on-chain hashes to square GDPR erasure rules with auditability. Penalties exceeding 4% of global revenue have made immutable ledgers a non-negotiable foundation in finance and life sciences.

Interoperability Issues Between Heterogeneous Blockchain Protocols and Legacy ERP Systems

Phoenix Strategy Group's 2025 guide found that 62% of projects slipped by more than 6 months due to middleware failures that map SAP tables to Hyperledger channels. Corda's UTXO model clashes with Ethereum's account-based state, forcing firms to run separate reconciliation layers. ISO's TC 307 aims to draft cross-chain APIs, but vendor rivalries postpone ratification. Companies with 20-year-old finance modules cannot justify rip-and-replace migrations, so brittle point-to-point integrations linger, inflating latency and support bills. North American and European manufacturers feel the pain first because they operate diversified legacy estates.

Other drivers and restraints analyzed in the detailed report include:

- Post-Quantum Cryptography Integration to Future-Proof ERP Platforms

- Growing Adoption of Smart-Contract-Driven Procurement Automation

- Uncertain Global Standards Governing Cross-Border On-Chain Data Residency

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform licenses accounted for 55.20% of 2025 revenue, but services are forecast to outgrow licenses at a 46.30% CAGR through 2031 as implementation complexity increases as new drivers intersect regulated workflows. Consulting now swallows 40-50% of total project budgets, covering architecture blueprints, governance policies, and zero-trust design. Managed-services subscriptions are popular among small enterprises that lack staff to monitor node performance and patch consensus clients. IBM, Infosys, and Accenture bundle monitoring, key-management, and smart contract auditing into annual retainers.

The blockchain-integrated ERP services market is projected to eclipse platform revenue by 2029. Vendors differentiate by vertical expertise, pharma serialisation, automotive quality audits, or banking collateral settlements, rather than by core ledger engine. SAP, Oracle, and Microsoft keep license churn low by embedding Hyperledger Fabric, Corda, or proprietary chains into Business Technology Platform, Fusion Cloud ERP, and Dynamics 365, respectively. Pure-play VeChain and ConsenSys win greenfield deals by promising governance flexibility and open-source tooling. Over the forecast horizon, automated code-generation and AI-assisted test harnesses will reduce development hours, yet specialized advisory work will remain essential in highly regulated verticals.

Hybrid cloud commanded 38.10% of 2025 revenue and is on track for a 42.10% CAGR. Enterprises partition workloads so personal data and financial ledgers reside on private nodes behind corporate firewalls, while non-sensitive events post to public or consortium chains for ecosystem visibility. Public cloud attracted roughly 35% of revenue, anchored by Amazon Managed Blockchain and Azure Confidential Ledger. Private cloud is dominant in defense, healthcare, and government because certification processes mandate single-tenant isolation.

Data-localization statutes such as China's Cybersecurity Law and the European Union's GDPR intensify hybrid adoption. SAP's February 2026 updates allow clients to replicate chain state across multiple regions, ensuring that European invoices never leave the bloc. Oracle's multi-cloud blueprint enables identical smart contracts to run across Oracle Cloud Infrastructure, Azure, and AWS regions, hedging against provider outages and vendor lock-in. Edge-native deployments are emerging as factories host lightweight Raft consensus on gateway appliances, synchronizing with cloud anchors hourly to cut latency on production lines.

Geography Analysis

North America led with 36.50% of 2025 spending, buoyed by early pilots in finance, tech, and healthcare. Wyoming, Delaware, and Texas enacted friendly legislation, while SEC guidance clarifies audit expectations. Canada funds mining supply chain pilots, tracking cobalt from pit to battery plant. Despite leadership, fragmented state laws introduce compliance complexity, slowing multi-state rollouts.

Asia-Pacific is the fastest-growing region at a projected 49.20% CAGR. China's Blockchain-based Service Network provides low-cost node hosting and cross-chain APIs. India's Ministry of Electronics and Information Technology mandates the use of distributed ledgers for government procurement, thereby seeding captive demand. Singapore's Infocomm Media Development Authority subsidizes trade digitization that cuts customs clearance times from days to minutes. South Korea's smart-port program attaches non-fungible tokens to containers, reducing demurrage fees.

Europe accounted for about 28% of 2025 revenue. The European Union's ViDA directive makes real-time e-invoicing compulsory, driving blockchain upgrades in automotive and luxury goods manufacturing hubs such as Germany and France. GDPR and data-sovereignty clauses spur adoption of hybrid cloud. The Middle East, spearheaded by the United Arab Emirates and Saudi Arabia's Vision 2030, is placing blockchain at the core of smart-city initiatives, from land registries to customs. Africa and South America each accounted for less than 5% of 2025 revenue, yet remittance corridors, agricultural provenance, and microfinance pilots demonstrate latent potential.

Overall, the blockchain-integrated ERP market faces a regulatory-innovation tension. Regions with the clearest rules attract platform spending first, but localization laws necessitate architectural gymnastics that lift professional-services revenue. Companies capable of navigating cross-border data frameworks will capture an outsized share as global supply networks rewire around shared ledgers.

- Oracle Corporation

- SAP SE

- International Business Machines Corporation

- Microsoft Corporation

- VeChain Technology Co., Ltd.

- ConsenSys Software Inc.

- Chainstack Pte. Ltd.

- Monax Industries Limited

- Accenture Plc

- Huawei Technologies Co., Ltd.

- Infosys Limited

- Inetum S.A.

- Synergix Technologies Pte. Ltd.

- Verizon Communications Inc.

- Wakuu Enterprises Inc.

- Oracle NetSuite LLC

- BlockApps Inc.

- Oracle Corporation (Hyperledger-based ERP)

- Infor, Inc.

- R3 HoldCo LLC

- SAP SE (SAP Business Network Blockchain)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Blockchain-Enabled Supply Chain Finance Modules

- 4.2.2 Post-Quantum Cryptography Integration to Future-Proof ERP Platforms

- 4.2.3 Regulatory Mandates for Immutable Audit Trails in Highly Regulated Sectors

- 4.2.4 Convergence of IoT and Tokenized Asset Tracking within ERP Workflows

- 4.2.5 Growing Adoption of Smart-Contract-Driven Procurement Automation

- 4.2.6 Rise of Decentralized Identity Frameworks for Vendor and Employee Access

- 4.3 Market Restraints

- 4.3.1 Interoperability Issues Between Heterogeneous Blockchain Protocols and Legacy ERP Systems

- 4.3.2 Scarcity of Blockchain-Savvy ERP Implementation Talent

- 4.3.3 Uncertain Global Standards Governing Cross-Border On-Chain Data Residency

- 4.3.4 High Energy Consumption Concerns for Permissionless Blockchain Architectures

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Supply Chain and Logistics Management

- 5.4.2 Financial Management and Auditing

- 5.4.3 Smart Contracts Automation

- 5.4.4 Identity and Access Management

- 5.4.5 Payment Systems

- 5.4.6 Other Applications

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and e-Commerce

- 5.5.3 Banking, Financial Services and Insurance

- 5.5.4 Healthcare

- 5.5.5 Transportation and Logistics

- 5.5.6 Government

- 5.5.7 Energy and Utilities

- 5.5.8 Others Industry Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Oracle Corporation

- 6.4.2 SAP SE

- 6.4.3 International Business Machines Corporation

- 6.4.4 Microsoft Corporation

- 6.4.5 VeChain Technology Co., Ltd.

- 6.4.6 ConsenSys Software Inc.

- 6.4.7 Chainstack Pte. Ltd.

- 6.4.8 Monax Industries Limited

- 6.4.9 Accenture Plc

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Infosys Limited

- 6.4.12 Inetum S.A.

- 6.4.13 Synergix Technologies Pte. Ltd.

- 6.4.14 Verizon Communications Inc.

- 6.4.15 Wakuu Enterprises Inc.

- 6.4.16 Oracle NetSuite LLC

- 6.4.17 BlockApps Inc.

- 6.4.18 Oracle Corporation (Hyperledger-based ERP)

- 6.4.19 Infor, Inc.

- 6.4.20 R3 HoldCo LLC

- 6.4.21 SAP SE (SAP Business Network Blockchain)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment