PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065724

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065724

Safari Tourism - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

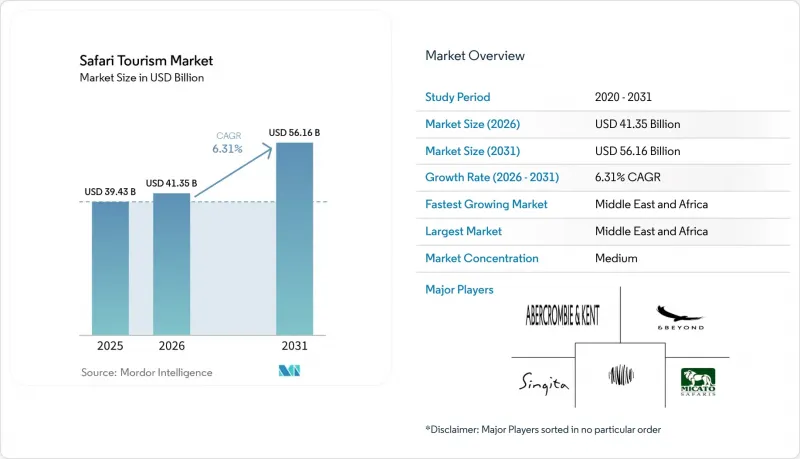

According to Mordor Intelligence, the safari tourism market size is expected to increase from USD 39.43 billion in 2025 to USD 41.35 billion in 2026 and reach USD 56.16 billion by 2031, growing at a CAGR of 6.31% over 2026-2031.

This report is Segmented by Tourism Type (Adventure, Private, Luxury, and More), by Accommodation Type (Resorts and Lodges, Tented Camps, Eco-Lodges, and Others), by Traveler Group (Group and Individual), by Booking Mode (Direct, Online Platforms, and Others), and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Safari Tourism Market Trends and Insights

Experiential Wildlife Travel Demand Reshapes Itinerary Architecture

Travel demand in the safari tourism market is shifting away from passive game viewing toward more active wildlife experiences, such as walking safaris, night drives, ranger-led tracking, and conservation-linked visits. This change matters because higher-engagement formats tend to deliver stronger local economic returns than standard mass-tourism products. The World Bank reported that Bwindi Impenetrable National Park in Uganda generated economic benefits that vastly exceeded its operating budget, demonstrating how low-volume, high-value wildlife tourism can scale economic impact. Buyers are also deciding earlier in the purchase process, which means digital content now influences destination choice before many travelers contact an operator. Operators that combine wildlife viewing with cultural and conservation activities are therefore capturing a larger share of trip spending in the safari tourism market.

Premiumization of Private Safari Itineraries Drives Per-Capita Yield Outperformance

The safari tourism market continues to show a clear shift toward higher-value private itineraries even as overall inquiry growth has normalized. Average budgets rose significantly year-on-year, suggesting strong pricing acceptance at the upper end of the safari tourism market. Product formats such as private camp buyouts, private villas, and exclusive-use departures are gaining traction because they offer more control over pace, privacy, and guest experience. This trend is pushing revenue growth toward yield expansion rather than pure traveler volume. It also favors operators that control premium inventory in private concessions and can package it into longer, more personalized journeys.

Political, Health, and Safety Disruptions Introduce Systemic Demand Shocks

The safari tourism market remains exposed to political events, public health concerns, and travel advisories because many of its core destinations depend on long-haul demand. The World Tourism Cities Federation projected Africa's 2026 tourism growth with a very wide range of possible outcomes, highlighting how quickly travel outcomes can change when external risks rise. High-value safari circuits in East and Southern Africa are especially sensitive because routing, insurance, and traveler confidence all affect booking conversion. A destination does not always need to experience a direct shock for demand to weaken, since regional headlines can influence trip planning across neighboring countries. This makes geographic diversification and flexible itinerary design important operating safeguards in the safari tourism market.

Other drivers and restraints analyzed in the detailed report include:

- Conservation-Led Travel Preferences Become a Purchasing Criterion

- Digital Discovery and Direct Booking Adoption Restructure Distribution Economics

- Climate Variability Affects Wildlife-Viewing Predictability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Adventure Safari held 29.84% of the safari tourism market share in 2025, making it the largest tourism type by revenue. Its scale comes from broad accessibility across budget group departures, classic lodge circuits, and mid-market expedition formats. That breadth makes Adventure Safari the main volume engine of the safari tourism market. It also leaves the segment more exposed to pressure from overtourism in heavily trafficked parks, as many itineraries still rely on standard game-drive patterns. Luxury Safari is forecast to grow at a 6.72% CAGR through 2031, indicating that high-end demand is advancing faster than the broader safari tourism market.

Luxury growth is being supported by stronger demand for private camps, exclusive-use villas, and personalized guiding. These products command higher rates because they deliver privacy, longer stays, and greater control over guest experience. The safari tourism industry is therefore seeing revenue growth shift toward yield rather than only toward higher visitor counts. Photographic Safari, Walking Safari, and Gorilla and Primate Safari remain smaller but strategically important because they serve travelers seeking deeper engagement and are less comparable with standard game-drive products. Gorilla and primate trips in particular continue to trade on scarcity because permit availability is structurally limited and closely linked to conservation carrying capacity.

Resorts and Lodges accounted for 38.63% of the safari tourism market in 2025, making them the largest accommodation type by revenue. Their position reflects established lodge networks, long-term operating agreements in core wildlife corridors, and the ability to serve both premium and upper mid-market demand. Eco-lodges are projected to grow at a 7.57% CAGR through 2031, making them the fastest-growing accommodation format in the safari tourism market. This reflects a clear overlap between premium pricing and visible sustainability credentials. The segment is benefiting from traveler preference for low-impact stays that still offer strong comfort and wildlife access.

In 2024, Great Plains Conservation launched Mara Toto Tree Camp in Kenya's Mara North Conservancy, demonstrating continued investment in high-value, design-led wilderness accommodation. Tented camps and bush camps also remain important because they preserve the traditional safari format and offer stronger wildlife proximity than more built-up properties. At the top end, water-based safari stays, treehouses, and other niche formats are pushing accommodation differentiation further by selling absolute scarcity and a more distinct sense of place. The safari tourism market is therefore moving toward product-led accommodation choice, where format matters almost as much as destination. The safari tourism industry is also rewarding operators that can combine environmental performance, exclusivity, and high service standards within a single asset.

Geography Analysis

Middle East and Africa retained 49.85% of the safari tourism market share in 2025 and is projected to grow at a 7.02% CAGR through 2031. This dual lead reflects the region's position as the core supply base of the safari tourism market, supported by wildlife estates, bush aviation links, private conservancies, and lodge development pipelines. South Africa, Kenya, and Tanzania continue to anchor the regional structure because they combine established tourism ecosystems with broad product depth across price points. Botswana is also strengthening its position through ultra-premium and low-density wilderness products, with Singita's planned Elela opening reinforcing the long-term appeal of controlled concession access. Rwanda and Uganda remain distinct high-value, low-volume destinations within the safari tourism market because gorilla trekking operates on scarcity, permit controls, and premium pricing rather than on high visitor throughput.

North America and Europe remain the main source-market engine for global safari revenue. The United States continues to be the most important high-spend source market, while the United Kingdom remains a major contributor to European demand in the safari tourism market. These two regions matter because they support both luxury custom itineraries and organized group formats. Premium safari demand from these markets also shows lower resistance to higher nightly rates and more willingness to purchase itinerary extensions such as beach stays or primate trekking. That spending pattern reinforces the importance of direct relationships, trusted specialist brands, and high-service booking support across the safari tourism market.

Asia-Pacific is the fastest-developing source region in proportional terms within the safari tourism market. Growth from this region is being supported by rising outbound travel, stronger digital trip discovery, and a growing preference for experiential long-haul travel. The World Tourism Cities Federation expects Asia-Pacific tourism growth to remain positive across a broad range of 2026 scenarios, supporting the region's long-term conversion potential. For operators, this means source diversification is expanding beyond traditional Western markets, even though conversion to safari travel remains more mature in North America and Europe. The safari tourism market is therefore expanding geographically on the demand side while remaining structurally concentrated in Africa on the supply side.

- Abercrombie & Kent

- A&K Sanctuary

- &Beyond

- Wilderness

- Singita

- Micato Safaris

- African Travel, Inc.

- Asilia Africa

- African Bush Camps

- Great Plains Conservation

- Gamewatchers Safaris

- Natural Habitat Adventures

- Audley Travel

- Ker & Downey Africa

- Go2Africa

- Nomad Tanzania

- Elewana Collection

- Scott Dunn

- Intrepid Travel

- G Adventures

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Experiential wildlife travel demand

- 4.2.2 Premiumization of private safari itineraries

- 4.2.3 Conservation-led travel preferences

- 4.2.4 Digital discovery and direct booking adoption

- 4.2.5 Shoulder-season normalization expands sellable inventory

- 4.2.6 Private conservancy-only activities widen product differentiation

- 4.3 Market Restraints

- 4.3.1 Political, health, and safety disruptions

- 4.3.2 Climate variability affects wildlife-viewing predictability

- 4.3.3 Flagship sighting overcrowding erodes premium experience value

- 4.3.4 Permit and conservation fee inflation raises trip friction

- 4.4 Value Chain Analysis

- 4.5 Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of new entrants

- 4.8.2 Bargaining power of suppliers

- 4.8.3 Bargaining power of buyers

- 4.8.4 Threat of substitutes

- 4.8.5 Intensity of competitive rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Tourism Type

- 5.1.1 Adventure Safari

- 5.1.2 Private Safari

- 5.1.3 Luxury Safari

- 5.1.4 Photographic Safari

- 5.1.5 Walking Safari

- 5.1.6 Gorilla and Primate Safari

- 5.2 By Accommodation Type

- 5.2.1 Safari Resorts and Lodges

- 5.2.2 Tented Camps and Bush Camps

- 5.2.3 Eco-lodges

- 5.2.4 Others (Houseboats, Water-Based Safari Stays, Treehouses, etc.)

- 5.3 By Traveler Group

- 5.3.1 Group

- 5.3.2 Individual

- 5.4 By Booking Mode

- 5.4.1 Direct Booking

- 5.4.2 Online Travel Platforms

- 5.4.3 Others (Marketplace Booking and others)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 BENELUX

- 5.5.3.8 NORDICS

- 5.5.3.9 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Abercrombie & Kent

- 6.4.2 A&K Sanctuary

- 6.4.3 &Beyond

- 6.4.4 Wilderness

- 6.4.5 Singita

- 6.4.6 Micato Safaris

- 6.4.7 African Travel, Inc.

- 6.4.8 Asilia Africa

- 6.4.9 African Bush Camps

- 6.4.10 Great Plains Conservation

- 6.4.11 Gamewatchers Safaris

- 6.4.12 Natural Habitat Adventures

- 6.4.13 Audley Travel

- 6.4.14 Ker & Downey Africa

- 6.4.15 Go2Africa

- 6.4.16 Nomad Tanzania

- 6.4.17 Elewana Collection

- 6.4.18 Scott Dunn

- 6.4.19 Intrepid Travel

- 6.4.20 G Adventures

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment