PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065783

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065783

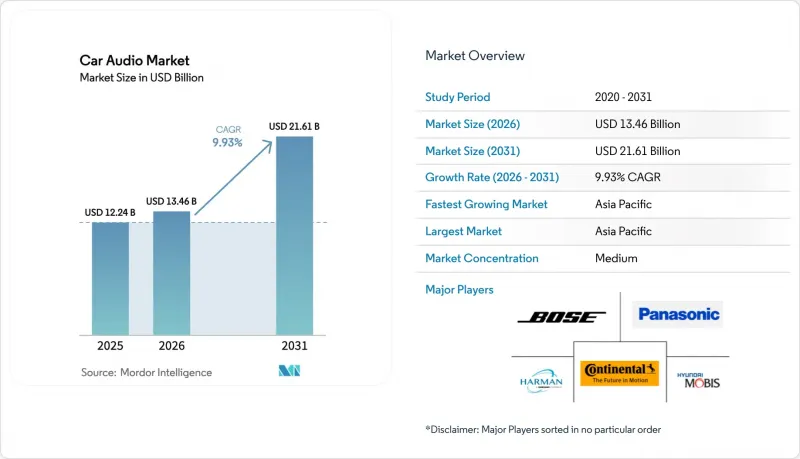

Car Audio - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the car audio market size was valued at USD 12.24 billion in 2025 and estimated to grow from USD 13.46 billion in 2026 to reach USD 21.61 billion by 2031, at a CAGR of 9.93% during the forecast period (2026-2031).

This report is Segmented by Component Type (Speakers [2-Way, 3-Way, and More], Amplifiers [Class-AB and Class-D], Head Units / DSP, and More), Vehicle Type (Hatchback, Sedan, and More), Sound Management Mode (Manual, Voice Recognition, and More), Sales Channel (OEM-Installed and Aftermarket), Connectivity Technology (Wired and Wireless), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Car Audio Market Trends and Insights

Voice-Controlled Audio Baseline in MY-27 Vehicles

Volkswagen already integrates a ChatGPT-powered assistant in its European portfolio that supports conversational commands. The shift removes physical buttons, frees dashboard space, and enables paid upgrades delivered by voice, influencing innovation across the car audio market.Suppliers must secure AI partnerships early because automakers lock preferred stacks into long development cycles that freeze specifications years ahead. The trend also raises privacy expectations, prompting on-device processing that avoids cloud latency and data exposure.

Class-D Amplifier Migration for EV Efficiency

Electric vehicle architectures cannot tolerate wasted watts. Class-D designs reach 90% efficiency, extending range and reducing thermal load. Asian factories specify Class-D across mid-segment models, pressuring North American badge engineers to follow suit. New silicon integrates one-inductor modulation that cuts part counts and board size, easing packaging in crowded instrument panels. OEM procurement teams prefer suppliers that offer retrofit-ready modules for legacy platforms, ensuring consistent sound reproduction while meeting tougher efficiency mandates. The incremental energy savings, though small per vehicle, scale across millions of units and thus carry strategic weight for fleet-level carbon compliance within the car audio market.

SDV Cyber-Security Certification Delays

Since July 2024, all new cars sold in the EU must comply with UN Regulation No. 155. Laboratories such as TUV SUD report queues for approval slots, postponing launch schedules and revenue recognition. Smaller audio suppliers lack dedicated cyber teams, stretching project budgets and sometimes leading OEMs to isolate audio domains from high-risk networks, limiting advanced feature integration. Every delay compresses the technology roadmap and reduces the window for monetizing audio upgrades, tempering near-term growth in the car audio market.

Other drivers and restraints analyzed in the detailed report include:

- Upselling Of 3-D / Immersive Sound Packages

- SDV Audio Feature Unlocks Via OTA

- Shortage of Automotive-Grade DSPs and MEMS Mics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Speakers contributed 46.81% of the car audio market share in 2025, underscoring their role as the primary perception driver of audio quality. Demand rises for slimline diaphragm designs that use lightweight composites, allowing automakers to embed drivers inside headliners and seats without adding mass. Class-D amplifiers follow as the high-growth component at 11.41% CAGR, pushed by electric-vehicle energy budgets that penalize inefficiency. Integration trends favor system-on-chip audio controllers that merge digital processing, amplification, and diagnostics into a single enclosure, reducing wiring weight and assembly time.

Software-defined architectures shift equalization and loudness management from discrete DSP boxes into central compute domains within the car audio market. This simplification frees dashboard real estate, yet places heightened accuracy requirements on speaker cones that must faithfully reproduce algorithmic outputs. Suppliers respond with low-profile woofers that extend frequency response below 30 Hz without the need for bulky enclosures. Piezo-based exciters capable of turning door panels into resonating surfaces enter pilot production, promising up to 90% packaging volume reduction.

SUVs accounted for 41.63% of car audio market size in 2025, and hold the highest 11.19% CAGR outlook to 2031. Their larger cabins support additional speaker placements, enabling immersive 19-channel sets that command a premium price. High rooflines ease antenna packaging for wireless subwoofers that maintain bass performance without structural vibration. Hatchbacks and sedans lose share to crossovers, yet they retain volume in cost-sensitive regions where compact body styles remain popular. Sports cars occupy niche positions but often specify flagship audio to justify brand pedigrees.

As electrification proliferates, SUVs transition into lifestyle hubs, hosting work calls, gaming sessions, and streaming content during charging stops. This usage profile increases dwell-time, driving consumer willingness to pay for upgraded sound. Manufacturers leverage modular audio platforms that scale from 8 speakers in entry trims to 24 speakers in luxury variants without rewiring the harness, optimizing margin capture across the car audio market.

Geography Analysis

Asia Pacific led with 43.23% share of the car audio market size in 2025, and is forecast to grow at 11.14% CAGR. Chinese automakers are projected to secure around one-fourth of the global vehicle share by 2030, underpinning volume demand for locally manufactured speakers and amplifiers. National industrial policy subsidizes domestic supply chains, allowing system integrators to cut lead times to 20 months, half the duration of traditional programs. South Korea and Japan augment regional momentum through advanced semiconductor ecosystems that feed Class-D amplifier modules, while India emerges as an assembly hub for entry-segment infotainment head units.

North America is the second-largest buyer, driven by consumer preference for large SUVs and pick-ups that provide abundant cabin space for multi-channel audio. Growth is slower because penetration exceeds 90%, yet upgrade rates remain healthy as OTA functions extend feature life cycles. Dealers bundle subscription trials with new models, converting about 25% of owners into recurring revenue plans.

Europe absorbs stringent cyber rules that lengthen validation cycles. Nevertheless, the bloc sets acoustic design trends that eventually globalize, such as mandated pedestrian warning sounds for electric cars, which require smart amplification and directional speakers. The Middle East and Latin America present smaller baselines but double-digit expansion owing to rising disposable income and grey-market imports of premium head units. Africa remains nascent, yet smartphone integration demand seeds future adoption of cost-optimized wireless audio within the car audio market.

- Harman International

- Panasonic Holdings

- Bose Corporation

- Sony Group (incl. Alpine)

- LG Electronics

- Hyundai Mobis

- Pioneer Corporation

- Denso

- Continental AG

- Faurecia-Forvia (Clarion)

- Alps Alpine

- Visteon

- Band W Group

- Meridian Audio

- Bang and Olufsen

- Dirac Research

- Cinemo

- Arkamys

- AAC Technologies / PSS

- Analog Devices

- NXP Semiconductors

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Voice-controlled audio baseline in MY-27 vehicles

- 4.2.2 Class-D amplifier migration for EV efficiency

- 4.2.3 Upselling of 3-D / immersive sound packages

- 4.2.4 SDV audio feature unlocks via OTA

- 4.2.5 E-commerce boom for plug-and-play upgrade kits

- 4.2.6 Acoustic glass enabling lighter speaker designs

- 4.3 Market Restraints

- 4.3.1 SDV cyber-security certification delays

- 4.3.2 Shortage of automotive-grade DSPs and MEMS mics

- 4.3.3 Right-to-Repair margin squeeze

- 4.3.4 Weight-saving mandates limiting speaker count

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Component Type

- 5.1.1 Speakers

- 5.1.1.1 2-Way

- 5.1.1.2 3-Way

- 5.1.1.3 4-Way and Coaxial

- 5.1.2 Amplifiers

- 5.1.2.1 Class-AB

- 5.1.2.2 Class-D

- 5.1.3 Head Units / DSP

- 5.1.4 Microphones and ANC Controllers

- 5.1.1 Speakers

- 5.2 By Vehicle Type

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUVs

- 5.2.4 MPVs

- 5.3 By Sound-Management Mode

- 5.3.1 Manual

- 5.3.2 Voice Recognition

- 5.3.3 AI-Driven Personalization

- 5.4 By Sales Channel

- 5.4.1 OEM-Installed

- 5.4.2 Aftermarket

- 5.5 By Connectivity Technology

- 5.5.1 Wired (MOST, A2B)

- 5.5.2 Wireless (Bluetooth, Wi-Fi, UWB)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Harman International

- 6.4.2 Panasonic Holdings

- 6.4.3 Bose Corporation

- 6.4.4 Sony Group (incl. Alpine)

- 6.4.5 LG Electronics

- 6.4.6 Hyundai Mobis

- 6.4.7 Pioneer Corporation

- 6.4.8 Denso

- 6.4.9 Continental AG

- 6.4.10 Faurecia-Forvia (Clarion)

- 6.4.11 Alps Alpine

- 6.4.12 Visteon

- 6.4.13 Band W Group

- 6.4.14 Meridian Audio

- 6.4.15 Bang and Olufsen

- 6.4.16 Dirac Research

- 6.4.17 Cinemo

- 6.4.18 Arkamys

- 6.4.19 AAC Technologies / PSS

- 6.4.20 Analog Devices

- 6.4.21 NXP Semiconductors

7 Market Opportunities and Future Outlook