PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066369

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066369

Residential Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

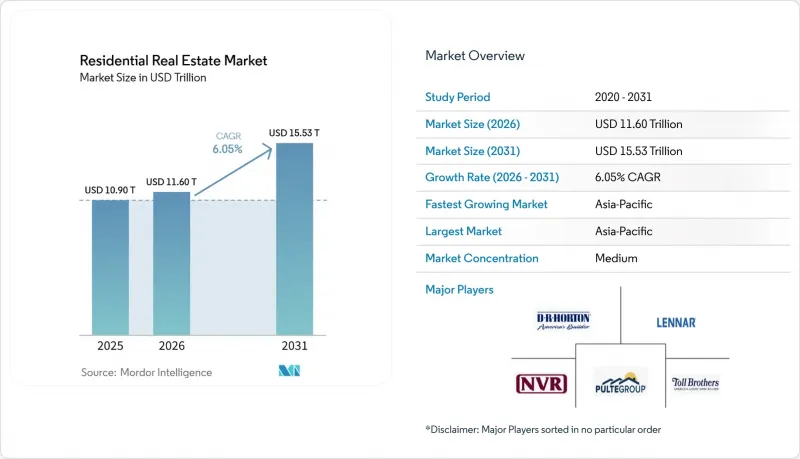

According to Mordor Intelligence, the residential real estate market size is expected to grow from USD 10.90 trillion in 2025 to USD 11.60 trillion in 2026 and is forecast to reach USD 15.53 trillion by 2031 at 6.05% CAGR over 2026-2031.

This report is Segmented by Property Type (Apartments & Condominiums, and Landed Houses & Villas), by Price Band (Affordable, Mid-Market, and Luxury/Super-prime), by Business Model (Sales and Rental), by Mode of Sale (Primary and Secondary), and by Region (North America, South America, Europe, Asia-Pacific, and Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Residential Real Estate Market Trends and Insights

Rapid Urbanisation & Middle-Class Expansion

The UN projects 68% of the global population will reside in urban areas by 2050, adding approximately 2.5 billion urban dwellers by that date, with 90% of this growth concentrated in Asia and Africa. In India alone, household formation is outpacing supply additions by an estimated 1.2 to 1.4 million units annually, compressing the country's housing deficit to critical levels despite government interventions such as the Pradhan Mantri Awas Yojana. Middle-class income thresholds are expanding fastest in Southeast Asian economies-Indonesia recorded a 23% rise in households earning above USD 5,000 annually between 2022 and 2025, directly fueling condominium absorption in Jakarta, Surabaya, and Bandung. This driver disproportionately benefits the mid-market price band, which commands 47% of the 2025 transaction share, yet it simultaneously tightens affordability ratios when wage growth lags property-price appreciation. Urbanisation's compound effect on land scarcity and infrastructure capex is pushing developers toward vertical-housing formats and transit-oriented developments, reshaping density norms in tier-2 and tier-3 cities. Policy frameworks such as India's Real Estate (Regulation and Development) Act, 2016 (RERA) and Indonesia's land-banking mandates are critical enablers that reduce project-delivery risk and attract institutional capital into previously informal markets.

Institutional BTR & SFR Capital Inflows

Institutional allocations to build-to-rent (BTR) and single-family rental (SFR) portfolios exceeded USD 85 billion globally in 2025, a 31% year-on-year increase, with North American platforms capturing 52% of that capital. Sovereign wealth funds and pension plans are treating rental housing as core infrastructure, drawn by inflation-linked cash yields averaging 4.5% to 5.8% net, regulatory stability, and demographic tailwinds such as delayed homeownership among millennials and Gen Z. In the EU, BTR supply now represents 18% of new multifamily completions in the UK and 11% in Germany, addressing a structural shortage of professionally managed rental stock that has depressed homeownership rates to multi-decade lows. Asia-Pacific is emerging as the next frontier: Japan's Ministry of Land, Infrastructure, Transport and Tourism approved BTR zoning incentives in 12 metropolitan zones in 2025, while South Korea's National Pension Service committed KRW 2.1 trillion (USD 1.6 billion) to domestic rental-housing funds. This capital is professionalizing asset management, embedding ESG standards, and pushing rental yields toward convergence with bond proxies, though it also intensifies competition with individual investors in secondary markets. Regulatory influence from bodies such as the Financial Conduct Authority (UK) and the Securities and Exchange Commission (US) ensures disclosure and tenant-protection compliance, further legitimizing the asset class for conservative allocators.

Global Housing-Affordability Crisis

Housing affordability across OECD markets reached historic stress levels in 2025, with the median house-price-to-income ratio rising to 8.7X, led by Sydney (13.2X), Toronto (11.8X), and Auckland (10.9X). In the UK, first-time buyers now require 5.8 years of gross income to fund a 15% deposit, up from 3.2 years in 2010, pushing younger households into the private-rental sector. Hong Kong's ratio eased marginally to 18.8X but remains prohibitive, with subsidised homeownership waitlists exceeding 280,000 applications. Governments are responding with affordability controls-foreign-buyer restrictions, vacant-home taxes, tighter loan-to-value limits, and the removal of interest-only mortgages-dampening transaction volumes and speculative demand. Intergenerational transfers now fund roughly 38% of UK first-time purchases, reinforcing inequality and constraining market mobility. These pressures weigh most heavily on entry- and mid-market segments, which represent over 60% of unit volumes, and are likely to persist absent sustained wage growth or meaningful supply-side reform.

Other drivers and restraints analyzed in the detailed report include:

- Net-Zero Mandates Driving Green-Retrofit Premium

- Climate-Risk Migration Reshaping Housing Pipelines

- Rising Policy Rates & Tighter Credit Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Apartments and condominiums accounted for 59.0% of the 2025 global total, the largest slice of residential real estate market share by product type, supported by higher land-use efficiency in dense urban centers and continued demand in gateway cities. This concentration reflects the economics of height in core districts, with master developers using larger towers to spread land costs and maintain acceptable project margins even as input inflation persists. Villas and landed houses remain the fastest-growing category, with a 6.23% CAGR expected during 2026-2031 as affluent buyers seek more space, privacy, and the lifestyle benefits of low-density neighborhoods. Select Gulf markets continue to prioritize horizontal communities that blend private plots with club amenities, which has reinforced premium absorption at the upper end of the residential real estate market. Developers in India have scaled villa formats in high-demand leisure and suburban submarkets, aiming to capture non-resident and upgrade demand as mortgage availability remains supportive for higher-income households.

The growth of townhouses and duplexes in North America and Europe illustrates the rise of "missing middle" formats, which add units within established neighborhoods without high-rise typologies. Modular and manufactured solutions have improved build speed and cost predictability for select programs, supporting affordability targets where standardization and procurement scale lower unit economics. Quality standards and energy codes have also converged, with developers investing in envelope performance, HVAC efficiency, and air-tightness metrics that reduce operating costs for residents. With supply concentrated in vertical formats and demand diversifying, the residential real estate market offers distinct value propositions across built forms that will continue to shape pricing and absorption patterns by location and income band.

The mid-market represented 47.0% of 2025 unit volumes, giving it the largest contribution to the residential real estate market size by price band as builders prioritize functional layouts and dependable commute access for dual-income households. Branded strategies that package popular finishes and smart home features at accessible price points continue to capture elastic demand when combined with targeted financing incentives. Price-sensitive absorption improves when monthly payments drop through rate buydowns or smaller price adjustments, and that responsiveness has made the mid-market a primary focus for inventory turns in several large metros. Developers are aligning product mix with local income distributions, which has produced more stable pre-sales profiles in markets with strong employment nodes and established school districts.

Luxury and super-prime segments in the residential real estate market are forecast to grow at a 6.30% CAGR during 2026-2031, supported by cash-rich buyers, branded residences, and international capital that seeks trophy assets, residency pathways, and inflation hedges. Sales campaigns for premium launches in India and the UAE demonstrate the speed of uptake when branding, location, and amenity programming align with high-net-worth preferences. In the same period, subsidized affordable housing pipelines remain central in emerging markets, where programmatic support reduces funding costs and ensures demand for targeted brackets. Builders in those programs have emphasized industrialized construction to maintain unit margins while meeting delivery timelines, proving that cost control is compatible with quality standards at scale.

Geography Analysis

Asia-Pacific held 34.50% of global activity in 2025 and is set to grow at a 6.96% CAGR during 2026-2031, making it both the largest and the fastest-growing region in the residential real estate market. Policy-backed delivery in India remains a core pillar, with PMAY-Urban 2.0 underpinning demand through interest subsidies, approval reforms, and transparent tracking of project milestones. In China, state-owned developers have gained share as they absorb pipeline and support stability in premium urban districts, while nationwide volumes continue to rationalize. Japan's urban markets maintain steady rent growth and long-duration mortgage products at low rates, supporting transactional resilience. Australia's tight rental markets reflect sustained migration and supply frictions, reinforcing development interest where feasibility holds. Across Southeast Asia, integrated townships are scaling to capture employment-led urbanization and household formation, bolstering mid-market and starter-home demand in key corridors.

North America is navigating a sizable supply gap and persistent affordability challenges, but rate stabilization and incentives on new-builds are helping to unlock transactions in the residential real estate market. Builders continue to price to market with financing support, seeking inventory turns that offset margin pressure and shifting focus toward community segmentation by buyer profile. In the U.S., regulatory constraints and long approval cycles are still binding in many jurisdictions, which limits supply elasticity and slows rebalancing in constrained metros. Canada's major cities remain undersupplied as population growth and immigration sustain household formation, while policy and stress-test rules influence buyer capacity. Mexico's regional growth benefits from nearshoring-driven jobs in manufacturing hubs, channeling demand into the workforce and mid-market housing in several industrial corridors.

Europe faces a twin imperative to retrofit aging stock and tighten standards for new-builds under the EPBD, creating both cost pressure and a large, investable upgrade pipeline within the residential real estate market. Landlords investing in energy efficiency report better net operating income through lower tenant utility costs and small rent premiums, strengthening the long-run case for modernization. Living-sector investment remains a favored allocation for institutions seeking defensive, inflation-linked cash flows across residential, student housing, and senior living. In the Middle East and parts of Africa, Saudi Arabia's Vision 2030 and active housing programs have advanced ownership goals while continuing to expand delivery capacity and eligibility for support. The United Arab Emirates continues to attract international buyers to master planned communities and branded residences, supported by long-term residency options and investment-friendly rules. Brazil anchors South America's activity through Minha Casa Minha Vida, where expanded eligibility and revised caps sustained launches and sales in 2025, supporting a diverse range of price points.

- D.R. Horton, Inc.

- Lennar Corporation

- PulteGroup, Inc.

- NVR, Inc.

- Toll Brothers, Inc.

- Meritage Homes Corporation

- KB Home

- Taylor Morrison Home Corporation

- China Vanke Co., Ltd.

- Poly Developments and Holdings Group Co., Ltd.

- China Overseas Land & Investment Limited

- China Resources Land Limited

- Vonovia SE

- Emaar Properties PJSC

- Aldar Properties PJSC

- DLF Limited

- Godrej Properties Limited

- Mahindra Lifespace Developers Ltd.

- MRV Engenharia e Participacoes S.A.

- Cyrela Brazil Realty S.A.

- Direcional Engenharia S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Residential Real Estate Buying Trends - Socio-economic and Demographic Insights

- 4.3 Government Initiatives and Regulatory Aspects for the Residential Real Estate Sector

- 4.4 Focus on Technology Innovation, Start-ups, and PropTech in Real Estate

- 4.5 Insights into Rental Yields in the Residential Segment

- 4.6 Real Estate Lending Dynamics

- 4.7 Insights into Affordable-Housing Support Provided by Government & Public-private Partnerships

- 4.8 Market Drivers

- 4.8.1 Rapid urbanisation & middle-class expansion

- 4.8.2 Institutional BTR & SFR capital inflows

- 4.8.3 Wealth migration & second-home demand in tax-advantaged hubs

- 4.8.4 Net-zero mandates driving green-retrofit premium

- 4.8.5 Climate-risk migration reshaping housing pipelines

- 4.8.6 Blockchain-enabled fractional ownership

- 4.9 Market Restraints

- 4.9.1 Global housing-affordability crisis

- 4.9.2 Rising policy rates & tighter credit standards

- 4.9.3 Construction-labour shortages & material-cost volatility

- 4.9.4 Hybrid-work vacancy drag in urban cores

- 4.10 Value / Supply-Chain Analysis

- 4.10.1 Overview

- 4.10.2 Real-estate Developers & Contractors - Key Quantitative and Qualitative Insights

- 4.10.3 Real-estate Brokers and Agents - Key Quantitative and Qualitative Insights

- 4.10.4 Property-management Companies - Key Quantitative and Qualitative Insights

- 4.10.5 Insights on Valuation Advisory and Other Real-estate Services

- 4.10.6 State of the Building-materials Industry & Partnerships with Key Developers

- 4.10.7 Insights on Key Strategic Real-estate Investors/Buyers in the Market

- 4.11 Porter's Five Forces

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Suppliers

- 4.11.3 Bargaining Power of Buyers

- 4.11.4 Threat of Substitutes

- 4.11.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 Sales

- 5.2 Rental

6 Sales Model Size & Growth Forecasts (Value, USD)

- 6.1 By Property Type

- 6.1.1 Apartments & Condominiums

- 6.1.2 Landed Houses & Villas

- 6.2 By Price Band

- 6.2.1 Affordable

- 6.2.2 Mid-Market

- 6.2.3 Luxury / Super-prime

- 6.3 By Mode of Sale

- 6.3.1 Primary (New-Build)

- 6.3.2 Secondary (Existing-home Resale)

- 6.4 By Region

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.1.3 Mexico

- 6.4.2 South America

- 6.4.2.1 Brazil

- 6.4.2.2 Argentina

- 6.4.2.3 Chile

- 6.4.2.4 Rest of South America

- 6.4.3 Europe

- 6.4.3.1 Germany

- 6.4.3.2 United Kingdom

- 6.4.3.3 France

- 6.4.3.4 Italy

- 6.4.3.5 Spain

- 6.4.3.6 Rest of Europe

- 6.4.4 Asia-Pacific

- 6.4.4.1 China

- 6.4.4.2 India

- 6.4.4.3 Japan

- 6.4.4.4 South Korea

- 6.4.4.5 Australia

- 6.4.4.6 Rest of Asia-Pacific

- 6.4.5 Middle East & Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Nigeria

- 6.4.5.5 Rest of Middle East & Africa

- 6.4.1 North America

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 7.4.1 D.R. Horton, Inc.

- 7.4.2 Lennar Corporation

- 7.4.3 PulteGroup, Inc.

- 7.4.4 NVR, Inc.

- 7.4.5 Toll Brothers, Inc.

- 7.4.6 Meritage Homes Corporation

- 7.4.7 KB Home

- 7.4.8 Taylor Morrison Home Corporation

- 7.4.9 China Vanke Co., Ltd.

- 7.4.10 Poly Developments and Holdings Group Co., Ltd.

- 7.4.11 China Overseas Land & Investment Limited

- 7.4.12 China Resources Land Limited

- 7.4.13 Vonovia SE

- 7.4.14 Emaar Properties PJSC

- 7.4.15 Aldar Properties PJSC

- 7.4.16 DLF Limited

- 7.4.17 Godrej Properties Limited

- 7.4.18 Mahindra Lifespace Developers Ltd.

- 7.4.19 MRV Engenharia e Participacoes S.A.

- 7.4.20 Cyrela Brazil Realty S.A.

- 7.4.21 Direcional Engenharia S.A.

8 Market Opportunities & Future Outlook

- 8.1 White-space & unmet-need assessment