PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066413

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066413

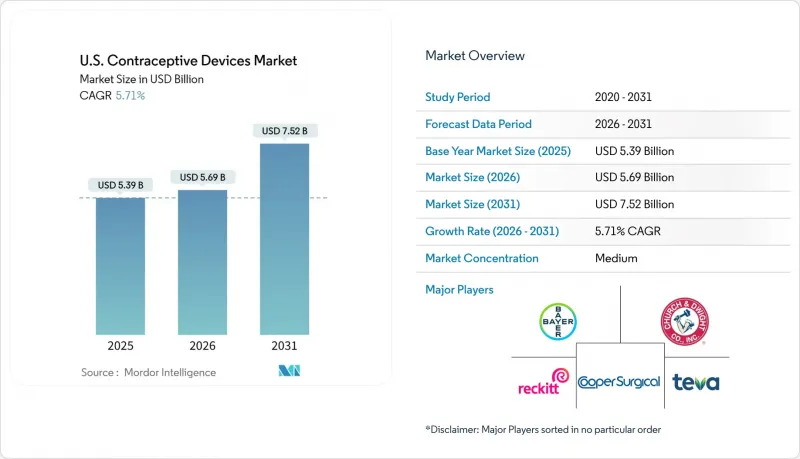

U.S. Contraceptive Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the u.S. contraceptive devices market size was valued at USD 5.39 billion in 2025 and is estimated to grow from USD 5.69 billion in 2026 to reach USD 7.52 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031).

This report is Segmented by Device Type (Condoms, Intra-Uterine Devices, Diaphragms, and More), Technology (Hormonal Devices and Non-Hormonal Devices), Gender (Male and Female), End-User (Home-care/Individual Users, and More), and Distribution Channel (Retail Pharmacies & Drug Stores, and More). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Contraceptive Devices Market Trends and Insights

Expansion of Medicaid Reimbursement and Employer-Sponsored Benefits

The August 2024 CMS bulletin obliges states to cover family-planning services without cost-sharing, smoothing the path to LARC uptake. A JAMA Health Forum study linked separate postpartum LARC reimbursement with a 1.58 percentage-point jump in overall LARC use within 60 days after delivery, underscoring how policy shifts remove long-standing cost barriers for underserved groups. Large employers have followed suit; mandates in California, Illinois, and New York now prohibit cost-sharing for all FDA-approved contraceptives, prompting self-funded plans to add high-priced options such as Annovera and Phexxi. Religious exemptions, however, still carve out gaps for employees at faith-based institutions, sustaining patchy coverage in parts of the Midwest and South.

Accelerating Adoption of LARCs

Post-Dobbs demand for longer-term protection pushes more consumers toward IUDs and implants. The Bixby Center reported higher LARC requests, while Tulsa County's Take Control Initiative distributed 2,855 IUDs and implants in 2024, reflecting heightened awareness of cost-effectiveness and reliability. The Dobbs decision intensified that pivot; a 2024 JAMA study found residents of abortion-ban states were 23% more likely to initiate an IUD or implant within six months of the ruling compared with counterparts in protected-access states.

Regulatory Uncertainty Post-Dobbs Decision

States with full abortion bans saw a 65% plunge in emergency contraceptive fills one year after Dobbs, along with a 25.6% fall in oral contraceptive prescriptions, stoking confusion among providers about legal parameters and hindering timely dispensing. Idaho and Missouri bills sought to block public funds for any method perceived as impairing implantation, prompting clinics to stockpile devices. The proposed Title X spending freeze for 2025 threatened 834,000 low-income patients and forced some centers to reduce hours. Medicaid cuts under discussion in Congress would undermine immediate postpartum LARC gains if implemented.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in IUD Insertion and Delivery

- Direct-to-Consumer and Telehealth Platforms

- Recalls and Litigation Linked to IUD Adverse Events

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Condoms accounted for 35.36% of contraceptive devices market share in 2025, yet IUDs are forecast to advance at an 8.43% CAGR through 2031, the swiftest clip across categories. LARC efficacy below 1% failure, combined with post-Dobbs risk calculus, is encouraging user migration away from coitally dependent barriers. The contraceptive devices market size tied to vaginal rings, implants, diaphragms, and caps remains modest but stable. Subdermal implants ride Nexplanon's three-year longevity and single-visit placement, whereas Miudella's slim inserter targets providers deterred by older copper models. Condom leaders continue to refresh latex alternatives and eco-friendly packaging, but their growth track is becoming defensive as long-term methods capture share.

Diaphragms, caps, and sponges collectively remain below a 2% sliver, constrained by fitting appointments and spermicide pairing requirements. Vaginal rings split into monthly NuvaRing and annual Annovera; the reusable Annovera commands a premium exceeding USD 2,000 annually when uninsured, narrowing its audience to high-income or fully covered groups. On-demand gel barriers such as Phexxi attract hormone-averse users yet face fluctuating reimbursement and 86% perfect-use efficacy that lags IUDs.

Non-hormonal products still lead with 56.56% share, but hormonal devices are on track for a 7.98% CAGR through 2031, outstripping their counterparts as extended-duration IUDs and implants lower lifetime cost per year protected. The contraceptive devices market size attributable to hormonal LARCs will expand as Mirena's eight-year label reduces swap-out visits and as Kyleena and Skyla cater to nulliparous users. Meanwhile, Miudella resets the copper category by shedding insertion complexity. Condoms, the largest non-hormonal bloc, remain vital for STI defense yet increasingly play a supplementary role to LARCs in steady partnerships.

List of Companies Covered in this Report:

- The Cooper Companies

- Abbvie

- Agile Therapeutics, Inc.

- Amneal Pharmaceuticals

- Bayer

- Church & Dwight Co., Inc. (Trojan)

- DKT International

- Evofem Biosciences, Inc.

- FemCap Inc.

- Futura Medical plc

- HLL Lifecare Ltd.

- Mayne Pharma Commercial LLC

- Okamoto Industries, Inc.

- Perrigo (HRA Pharma)

- Pfizer

- Pregna International Ltd.

- Reckitt Benckiser Group plc (Durex)

- Teva Pharmaceutical Industries

- TherapeuticsMD

- Veru

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Expansion of Medicaid Reimbursement and Employer-Sponsored Benefits

- 4.1.2 Accelerating Adoption of LARCs

- 4.1.3 Technological Advances in IUD Insertion and Delivery

- 4.1.4 Direct-to-Consumer and Telehealth Platforms

- 4.1.5 Teen-Pregnancy Prevention Campaigns

- 4.1.6 Surge in Male Contraceptive R&D Pipelines

- 4.2 Market Restraints

- 4.2.1 Regulatory Uncertainty Post-Dobbs Decision

- 4.2.2 Recalls and Litigation Linked to IUD Adverse Events

- 4.2.3 Cultural & Religious Opposition in Select Demographics

- 4.2.4 Limited Insurance Coverage for Premium Devices

- 4.3 Supply-Chain Analysis

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Condoms

- 5.1.2 Intra-Uterine Devices

- 5.1.3 Vaginal Rings

- 5.1.4 Subdermal Implants

- 5.1.5 Diaphragms

- 5.1.6 Cervical Caps

- 5.1.7 Sponges

- 5.1.8 Other Devices (Patches, Gel Barriers)

- 5.2 By Technology

- 5.2.1 Hormonal Devices

- 5.2.2 Non-Hormonal Devices

- 5.3 By Gender

- 5.3.1 Male

- 5.3.2 Female

- 5.4 By End-User

- 5.4.1 Home-care/Individual Users

- 5.4.2 Hospitals

- 5.4.3 Clinics & Community Health Centers

- 5.4.4 Specialty & Ambulatory Surgery Centers

- 5.5 By Distribution Channel

- 5.5.1 Retail Pharmacies & Drug Stores

- 5.5.2 Hospital Pharmacies

- 5.5.3 Online & Direct-to-Consumer Platforms

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 CooperSurgical Inc.

- 6.3.2 AbbVie Inc.

- 6.3.3 Agile Therapeutics, Inc.

- 6.3.4 Amneal Pharmaceuticals Inc.

- 6.3.5 Bayer AG

- 6.3.6 Church & Dwight Co., Inc. (Trojan)

- 6.3.7 DKT International

- 6.3.8 Evofem Biosciences, Inc.

- 6.3.9 FemCap Inc.

- 6.3.10 Futura Medical plc

- 6.3.11 HLL Lifecare Ltd.

- 6.3.12 Mayne Pharma Commercial LLC

- 6.3.13 Okamoto Industries, Inc.

- 6.3.14 Perrigo (HRA Pharma)

- 6.3.15 Pfizer Inc.

- 6.3.16 Pregna International Ltd.

- 6.3.17 Reckitt Benckiser Group plc (Durex)

- 6.3.18 Teva Pharmaceutical Industries Ltd

- 6.3.19 TherapeuticsMD Inc.

- 6.3.20 Veru Inc.

- 6.3.21 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment