PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066456

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066456

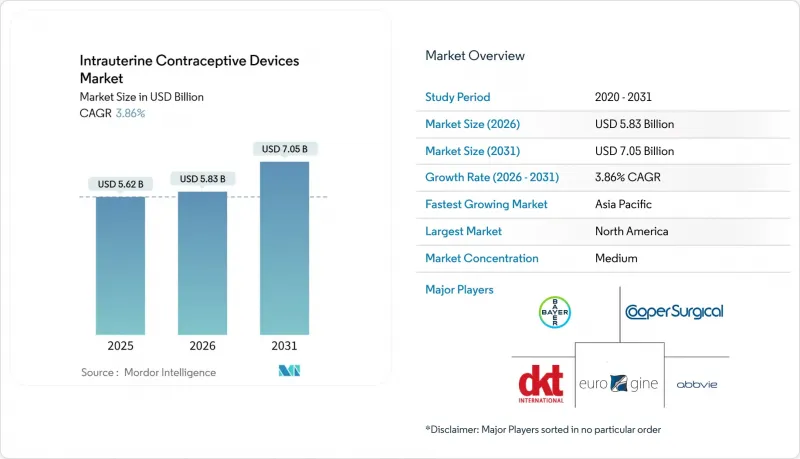

Intrauterine Contraceptive Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the intrauterine contraceptive devices market size is expected to increase from USD 5.62 billion in 2025 to USD 5.83 billion in 2026 and reach USD 7.05 billion by 2031, growing at a CAGR of 3.86% over 2026-2031.

This report is Segmented by Device Type (Hormonal LNG-IUS, Copper IUD), Indication (Contraception and More), Age Group (<20, 20-24, 25-34, and More), End-User (Hospitals, Gynecology & Obstetrics Clinics, and More), Distribution Channel (Public Procurement, Private Clinics, and More), and Geography (North America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Intrauterine Contraceptive Devices Market Trends and Insights

Technological Innovation Leading to Effective Contraceptives and Fewer Side Effects

New materials and engineering approaches are redefining copper devices. The FDA-cleared MIUDELLA uses a nitinol frame and 50% less copper yet keeps 99% efficacy, easing pain and heavy bleeding previously linked to conventional designs. Research teams are testing flexible iron-based frames that could cut inflammatory responses while safeguarding contraceptive strength. These improvements matter most in markets where fear of adverse events still deters uptake, and they give suppliers an edge with premium pricing tied to better user comfort. Bayer's Kyleena uses a 19.5 mg hormone load and a 3.8 mm inserter, cutting insertion-pain scores by 30% compared with 52 mg predecessors, which lifts 12-month continuation to 88%. These refinements make the intrauterine contraceptive devices market more attractive to first-time users and younger patients who previously favored short-acting options.

Rising Demand for Long-Acting Reversible Contraceptives (LARCs)

Healthcare providers are steering patients toward devices that require no daily action and have a <1% first-year failure rate. Women aged 25-34 already represent nearly two-thirds of IUD use, mirroring their desire for extended protection while postponing pregnancies. Updated U.S. practice guidelines in 2024 place LARCs first in counseling scripts, a move likely to ripple into other national protocols.

Global fertility fell to 2.3 births per woman in 2025, with East Asia at 1.2 and Southern Europe at 1.3. Users postponing childbirth now prize methods that remove daily adherence and equal sterilization in effectiveness, a perception that propels the intrauterine contraceptive devices market. A 2024 Guttmacher survey across 15 nations showed 62% of LARC users cited "set-and-forget" convenience as the primary reason for choosing an IUD, up from 38% for short-acting methods. Uptake closely tracks female labor-force participation above 55%, which underscores the link between economic empowerment and sustained contraceptive demand.

Risk of Side Effects and Complications

Heavy bleeding, cramping, and misplaced insertions remain the top deterrents. A 2024 study in the International Journal of Pharmaceutics links polymer formulation and curing conditions to variable LNG release, which can influence the occurrence of adverse events. Provider skill also matters; malposition rates are nearly double when generalists insert devices versus obstetric-gynecology specialists. Bleeding changes and insertion pain still lead to 22% discontinuation among copper users and 14% among levonorgestrel users within 12 months, according to a 2025 meta-analysis of 47 studies. Even low perforation rates trigger malpractice suits, raising liability premiums for clinics. These realities dampen provider enthusiasm in low-resource areas, moderating expansion of the intrauterine contraceptive devices market despite high unmet need.

Other drivers and restraints analyzed in the detailed report include:

- Government Initiatives and Support Policies

- Favorable Recommendations from Global Health Organizations

- Cultural and Religious Opposition Coupled with Lack of Awareness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Copper models captured 66.10% of the intrauterine contraceptive devices market share in 2025, driven by their hormone-free appeal and low device cost. Levonorgestrel systems are growing at a 6.25% CAGR because they treat heavy menstrual bleeding while preventing pregnancy, allowing insurers to allocate expenses across two benefit categories. This dual utility boosts willingness to fund higher device prices that nonetheless undercut the USD 15,000-25,000 cost of hysterectomy or ablation. The February 2025 approval of MIUDELLA featuring a flexible nitinol frame and reduced copper illustrates how engineering refinements address historic pain and bleeding complaints, boosting acceptance in regions where side effects once limited uptake. Academic teams pursuing iron-based frames highlight a potential next class of non-hormonal products with softer inflammatory profiles that could lure users who previously avoided copper models.

Manufacturers are also enhancing supply-chain efficiency to lower production costs, a change that supports public-sector tenders seeking bulk volumes at modest price points. Given these trends, copper units will remain volume leaders. Still, hormonal devices are set to capture incremental value share as higher reimbursement ceilings in Europe and North America favor premium pricing.

Contraception held 78.80% of the intrauterine contraceptive devices market size in 2025. Endometrial protection during hormone-replacement therapy shows the fastest growth at 9.28% CAGR since the North American Menopause Society endorsements revived systemic estrogen use for women under 60. Mirena's HRT-linked label allows gynecologists to serve both contraception and menopausal symptom management with one device, adding appeal among perimenopausal women.

Heavy-bleeding therapy is growing as primary-care physicians shift first-line management from oral drugs to IUD insertion. Manufacturers diversify revenue streams toward menopausal cohorts, hedging against shrinking fertility populations yet keeping intrauterine contraceptive devices market relevance across life stages.

Geography Analysis

North America retained 39.90% of % intrauterine contraceptive devices market share in 2025, buoyed by Medicaid expansion in 12 states and zero-copay rules under the Affordable Care Act. The United States contributed roughly three-quarters of regional volume, while Canada's provincial plans added device coverage in 2024. Between 2026 and 2031, the region is forecast to maintain mid-single-digit growth as payors tie reimbursement to continuation rates that favor IUD longevity.

Asia-Pacific is rising fastest, with a 6.45% CAGR. China's policy shift toward larger families amplifies demand for reversible contraception, and India's scaled-up free IUD program widens rural access. Indonesia, Vietnam, and the Philippines follow with middle-class uptake of levonorgestrel systems that tackle heavy bleeding. Despite price sensitivity, donor subsidies and domestic manufacturing keep the intrauterine contraceptive devices market affordable in lower-income pockets.

The Middle East and Africa are the fastest-growing regions as multilateral initiatives expand product availability and provider capacity, though cultural resistance still dampens absolute penetration. UNFPA's Supplies Partnership now covers 54 countries, with IUD availability at secondary care sites rising to 65% in 2024. Sub-Saharan Africa's average modern-method prevalence sits at 28.4%, and only 9.6% of women use long-acting methods, highlighting vast untapped potential as training and outreach progress.

- Abbvie

- Aetos Pharma Pvt Ltd

- Agile Therapeutics

- Bayer

- Contrel Europe NV

- The Cooper Companies

- DKT International

- Egemen International

- Eurim Group

- EUROGINE S.L.

- Gedeon Richter Polska

- Gynocare

- HLL Lifecare

- Melbea

- Meril Life Sciences

- Mona Lisa

- OCON Medical Ltd.

- Pregna International Ltd.

- Prosan International

- Sebela Pharmaceuticals

- SMB

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological Innovation Leading to Effective Contraceptives and Less Side Effects

- 4.2.2 Rising Demand for Long-Acting Reversible Contraceptives (LARCs)

- 4.2.3 Government Inititives and Support Policies

- 4.2.4 Favorable recommendations from Global Health Organziations

- 4.2.5 Increasing Trend of Delayed Childbirth

- 4.2.6 Expansion of NGO-led social-marketing campaigns and public private partnership distribution programs

- 4.3 Market Restraints

- 4.3.1 Risk Of Side Effects and Complications

- 4.3.2 Cultural & Religious Opposition to IUDs Coupled with Lack of Awareness

- 4.3.3 Skilled Provider Shortage for Insertions

- 4.3.4 High Up-Front Device and Insertion Cost

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Hormonal LNG-IUS

- 5.1.2 Copper IUD

- 5.2 By Indication

- 5.2.1 Contraception

- 5.2.2 Heavy Menstrual Bleeding therapy

- 5.2.3 Endometrial Protection during HRT

- 5.3 By Age Group

- 5.3.1 <20 Years

- 5.3.2 20-24 Years

- 5.3.3 25-34 Years

- 5.3.4 35-44 Years

- 5.3.5 >44 Years

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Gynecology & Obstetrics Clinics

- 5.4.3 Community Health Centers

- 5.4.4 Family-Planning / Sexual-Health Centers

- 5.4.5 Tele-health Enabled Home-Insertion Programs

- 5.5 By Distribution Channel

- 5.5.1 Public Sector Procurement

- 5.5.2 Private Clinics & Retail

- 5.5.3 NGO/Donor-Funded Programs

- 5.5.4 Online & Pharmacy E-commerce

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc (Allergan)

- 6.3.2 Aetos Pharma Pvt Ltd

- 6.3.3 Agile Therapeutics

- 6.3.4 Bayer AG

- 6.3.5 Contrel Europe NV

- 6.3.6 CooperSurgical Inc.

- 6.3.7 DKT International

- 6.3.8 Egemen International

- 6.3.9 Eurim Group

- 6.3.10 EUROGINE S.L.

- 6.3.11 Gedeon Richter Polska

- 6.3.12 Gynocare

- 6.3.13 HLL Lifecare Ltd

- 6.3.14 Melbea AG

- 6.3.15 Meril Life Sciences

- 6.3.16 Mona Lisa NV

- 6.3.17 OCON Medical Ltd.

- 6.3.18 Pregna International Ltd.

- 6.3.19 Prosan International BV

- 6.3.20 Sebela Pharmaceuticals

- 6.3.21 SMB Corporation of India

- 6.3.22 Viatris

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment