PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066414

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066414

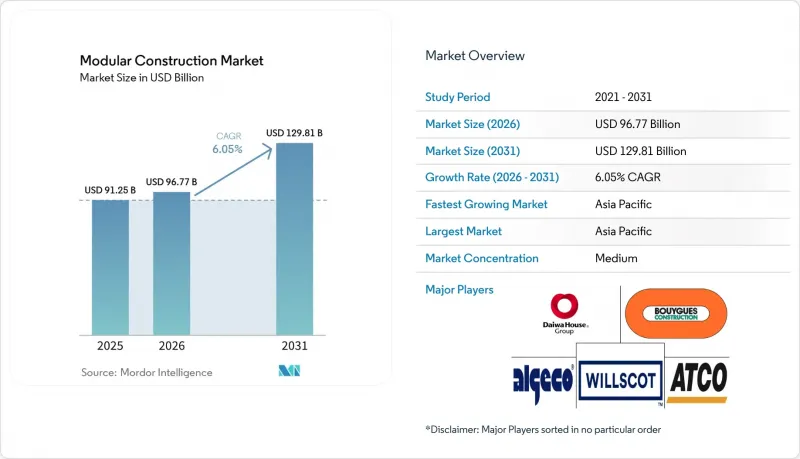

Modular Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the modular construction market size is expected to increase from USD 91.25 billion in 2025 to USD 96.77 billion in 2026 and reach USD 129.81 billion by 2031, growing at a CAGR of 6.05% over 2026-2031.

This report is Segmented by Material (Steel, Concrete, Wood, and Plastic), Construction Type (Permanent Modular and Relocatable Modular), Service Stage (New Construction and After-Sales Maintenance and Refurbishment), End-User Sector (Industrial/Institutional, Residential, and Commercial), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Global Modular Construction Market Trends and Insights

Rapid Urbanisation-Driven Housing Gap

Asia-Pacific's pace of city growth is stretching conventional building capacity. China's urbanization rate reached 65% in 2024 and is guided to 70% by 2030, a shift that adds 300 million residents and intensifies demand for faster delivery models. Shenzhen, Beijing, and Shanghai require that 30% of public projects use prefab systems, and India's Pradhan Mantri Awas Yojana has cleared 1.12 crore urban units, of which 88.62 lakh were completed by 2025. Vietnam expects 40% urban population by 2030 and is piloting industrialized building in Hanoi and Ho Chi Minh City. Even the United Kingdom faces a 4.3 million-home shortfall, which prompted a target of 15,000 modular units each year, although factory capacity constrains current output. These conditions collectively lift baseline demand for the modular construction market.

Supportive Government Incentives and Mandates

Regulators have moved from voluntary guidelines to binding quotas and direct subsidies. California's Factory-Built Housing program cut permitting cycles from 18 months to 6 months in areas that accepted USD 12 million of state technical aid in 2024. A federal bill, H.R. 10171, proposes USD 30 billion in grants and USD 3 billion in tax credits to accelerate adoption, while Europe's revised Energy Performance of Buildings Directive requires all new structures to be zero-emission by 2030. Saudi Arabia's Vision 2030 program targets 300,000 units per year and ranks modular delivery high for speed assurance. These tools improve project economics, favoring the modular construction market over conventional methods.

High Upfront Factory and Module-Handling CAPEX

Establishing a mid-scale plant that delivers 500-1,000 housing units each year demands USD 15-25 million for land, cranes, automated welders, and climate-controlled bays. Specialized trailers and escort vehicles add several million more for firms that serve multi-state corridors. Factories must operate at 60-70% utilization to meet breakeven, yet limited access to project finance in emerging markets keeps borrowing costs high. These economics funnel activity toward well-capitalized, vertically integrated players and restrain smaller contractors from entering the modular construction market.

Other drivers and restraints analyzed in the detailed report include:

- Faster Project Timelines and Lifecycle Cost Savings

- Labour-Shortage Mitigation Via Off-Site Fabrication

- Architectural and Aesthetic Design Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Steel captured 83.87% of modular construction market share in 2025 thanks to its favorable strength-to-weight profile and compatibility with automated factory tools. That dominance is expected to persist as high-strength grades such as ASTM A992 allow longer spans while staying within transport weight limits. Automated welding drops labor hours and improves joint quality, further anchoring steel in industrial and multi-story projects.

Wood-mainly cross-laminated timber-has emerged as a low-carbon alternative in Europe and North America, enjoying double-digit growth under the EU Timber Regulation. CLT stores about 0.8 tons of CO2 per cubic meter and now meets fire-safety codes up to 18 stories. Concrete modules remain niche due to heavy panel weights that raise logistics costs, while plastic composites are carving out roles in disaster relief where corrosion resistance and airlift ability outweigh structural limits. Continuous material innovation broadens supplier options, yet steel is expected to hold a clear lead in the modular construction market through 2031.

Permanent modular accounted for 67.18% of modular construction market size in 2025 and will stay ahead as airports, schools, data centers, and hospitals seek long-life assets. Integrated mechanical and electrical systems arrive pre-tested, cutting commissioning time and minimizing punch-list items.

Relocatable modular, growing at a 7.35% CAGR, appeals to mining, disaster relief, and temporary healthcare operators that value rapid deployment and reuse. WillScot Mobile Mini manages a fleet of more than 200,000 units under lease contracts that wrap in maintenance, showing how flexible asset models add depth to the modular construction market. The coexistence of long-life and relocatable designs enables suppliers to serve divergent risk profiles and funding cycles.

Geography Analysis

Asia-Pacific contributed 47.16% of global revenue in 2025 and is expected to expand at 7.21% through 2031. China's plan to raise its urbanization ratio to 70% by 2030, India's sizable housing missions, and prefab mandates across Singapore and Malaysia all steer capital toward off-site production. Japanese leaders Sekisui House and Daiwa House export factory know-how into Australia and the United States, strengthening regional value chains.

North America is characterized by labor shortages and large-scale incentives. The proposed USD 30 billion federal grant package and state-level programs shorten approval windows, while mega-projects such as Terminal F at Dallas Fort Worth showcase scale efficiencies. Regulatory fragmentation between states, however, still inflates compliance costs and slows shipment across borders, tempering the pace of modular construction market growth.

Europe's path is defined by decarbonization rules and timber uptake. The Energy Performance of Buildings Directive enforces zero-emission targets, positioning factory-made envelopes as a compliance shortcut. Labor deficits in Germany and the United Kingdom amplify the shift toward prefab methods. Emerging regions, including Saudi Arabia and Brazil, register strong demand but must overcome financing constraints and limited local plant capacity to unlock full contributions to the modular construction market.

- ACS Group

- Algeco UK Limited (Modulaire Group)

- Alta-Fab Structures Ltd.

- ATCO Ltd.

- Balfour Beatty

- Bechtel Corporation

- Bouygues Construction

- CIMC Modular Building

- DAIWA HOUSE INDUSTRY CO., LTD.

- Fluor Corporation

- Guerdon, LLC.

- Laing O'Rourke

- Larsen & Toubro Limited

- Lendlease Corporation

- Modular System Sp. z o.o.

- NRB Modular Solutions

- Red Sea International

- Sekisui House Ltd

- Skanska

- Stack Modular

- Wernick Group

- WillScot

- Zekelman Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Urbanisation-Driven Housing Gap

- 4.2.2 Supportive Government Incentives and Mandates

- 4.2.3 Faster Project Timelines and Lifecycle Cost Savings

- 4.2.4 Labour-Shortage Mitigation Via Off-Site Fabrication

- 4.2.5 ESG-Linked Financing and Carbon-Pricing Tailwinds

- 4.3 Market Restraints

- 4.3.1 High Upfront Factory and Module-Handling CAPEX

- 4.3.2 Architectural and Aesthetic Design Constraints

- 4.3.3 Fragmented Global Building Codes and Permits

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Steel

- 5.1.2 Concrete

- 5.1.3 Wood

- 5.1.4 Plastic

- 5.2 By Construction Type

- 5.2.1 Permanent Modular

- 5.2.2 Relocatable Modular

- 5.3 By Service Stage

- 5.3.1 New Construction

- 5.3.2 After-sales Maintenance and Refurbishment

- 5.4 By End-user Sector

- 5.4.1 Industrial/Institutional

- 5.4.2 Residential

- 5.4.3 Commercial

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 NORDIC Countries

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 ACS Group

- 6.4.2 Algeco UK Limited (Modulaire Group)

- 6.4.3 Alta-Fab Structures Ltd.

- 6.4.4 ATCO Ltd.

- 6.4.5 Balfour Beatty

- 6.4.6 Bechtel Corporation

- 6.4.7 Bouygues Construction

- 6.4.8 CIMC Modular Building

- 6.4.9 DAIWA HOUSE INDUSTRY CO., LTD.

- 6.4.10 Fluor Corporation

- 6.4.11 Guerdon, LLC.

- 6.4.12 Laing O'Rourke

- 6.4.13 Larsen & Toubro Limited

- 6.4.14 Lendlease Corporation

- 6.4.15 Modular System Sp. z o.o.

- 6.4.16 NRB Modular Solutions

- 6.4.17 Red Sea International

- 6.4.18 Sekisui House Ltd

- 6.4.19 Skanska

- 6.4.20 Stack Modular

- 6.4.21 Wernick Group

- 6.4.22 WillScot

- 6.4.23 Zekelman Industries

7 Market Opportunities and Future Outlook

- 7.1 Green and Sustainable Construction Demand

- 7.2 White-space and Unmet-Need Assessment