PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066445

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066445

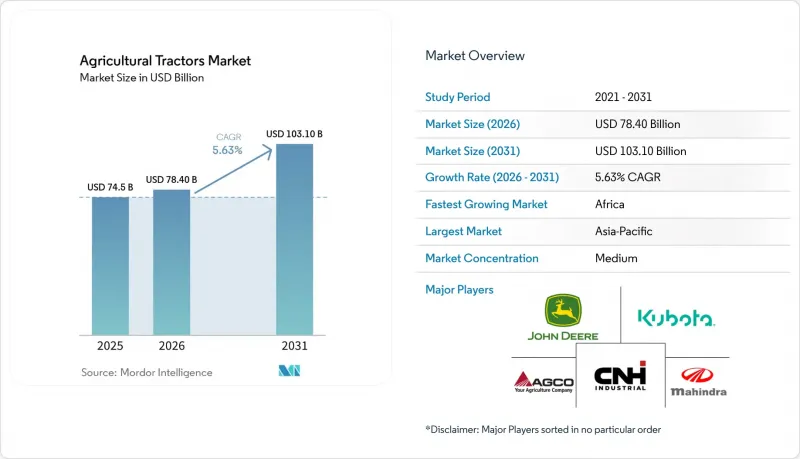

Agricultural Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the agricultural tractors market size is anticipated to increase from USD 74.5 billion in 2025 to USD 78.40 billion in 2026 and reach USD 103.10 billion by 2031, growing at a CAGR of 5.63% over 2026-2031.

This report is Segmented by Power Output (Less Than 40 HP, 40-100 HP, 101-200 HP, and More Than 200 HP), by Drive Type (2-Wheel Drive and 4-Wheel Drive), by Engine Type (Diesel, Electric, and Hybrid), by Tractor Type (Utility, Row-Crop, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Agricultural Tractors Market Trends and Insights

Government Mechanization Subsidy Continuity

Government-supported mechanization programs continue to play a significant role in sustaining demand for the agricultural tractors market in regions such as India, Sub-Saharan Africa, and Southeast Asia. In India, subsidies provided under the Sub-Mission on Agricultural Mechanization remain a key factor in ensuring tractors are accessible in districts with lower levels of mechanization. In Nigeria, a structured mechanization rollout in 2025 introduced 2,000 heavy-capacity tractors through mechanization service providers under a lease-to-own model, reflecting a more organized procurement strategy compared to direct public ownership. This shift influences how manufacturers approach the agricultural tractors market, as fleet intermediaries require large-scale financing, service planning, and parts support. Additionally, China's 75.5% mechanization rate for crop planting, harvesting, and processing by 2025 serves as a benchmark for neighboring countries aiming to accelerate agricultural modernization .

Precision Agriculture Integration Across Installed Fleets

Precision agriculture adoption is advancing more rapidly across existing equipment fleets than new tractor sales alone indicate. This trend is significant for the agricultural tractors market, as digital capabilities are increasingly being integrated through upgrades. The economic benefits are becoming more evident, with the Association of Equipment Manufacturers and Kearney estimating that current precision agriculture adoption has increased annual crop production in the United States by 5% and reduced fuel consumption by 147 million gallons annually in 2025 . This is driving demand for retrofitting, as mixed-brand farm operators seek unified guidance and data tools without waiting for a complete equipment replacement cycle. Consequently, the agricultural tractors market is favoring manufacturers and technology providers capable of supporting the existing equipment base, rather than relying solely on new equipment sales.

High Acquisition Cost and Tighter Machinery Financing

Higher borrowing costs and tighter credit conditions are delaying purchase decisions in the agricultural tractors market, particularly for high-value machinery categories in the United States. In the United States high-horsepower segment, retail values for tractors above 425 HP decreased by 3.2% year-over-year in 2025, while auction values declined by 6.7%. This reflects weaker buyer sentiment and the financial strain caused by elevated dealer carrying costs. The impact varies across farm sizes, with large-scale operators taking advantage of opportunities in the used-equipment market, while smaller farms face greater financing challenges and delayed replacement cycles. Consequently, the agricultural tractors market is becoming increasingly polarized, with stronger demand for advanced premium machinery and weaker demand for entry-level and utility tractor models in more price-sensitive farming segments.

Other drivers and restraints analyzed in the detailed report include:

- High-Horsepower and 4-Wheel Drive Adoption on Large Farms

- Retrofit-First Autonomy and Guidance Upgrades

- Emissions-Compliant Diesel Powertrain Cost Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The agricultural tractors market share for the 40-100 HP segment led with the largest 42.9% in 2025. This segment remains dominant due to its suitability for mixed farming, haulage, tillage, and utility operations in emerging agricultural economies. Mid-range tractors are widely adopted in regions such as Asia-Pacific, South America, and parts of Africa, where farms require a balance of fuel efficiency and implement compatibility. Smaller farms favor these tractors for their operational flexibility and lower ownership costs compared to high-horsepower models. The stability in demand for this segment highlights the continued reliance on versatile, utility-focused farm mechanization.

The agricultural tractors market size for the more than 200 HP segment is forecast to grow at the fastest 7.5% CAGR from 2026 to 203. This growth is driven by increasing farm consolidation and the rising need for large-scale field productivity in regions such as North America, Brazil, and Eastern Europe. Large commercial operators are adopting higher horsepower equipment to enhance field coverage and reduce seasonal operating time. Premium manufacturers are focusing on developing advanced row-crop and high-capacity tractor platforms equipped with precision farming systems. However, mid-range tractors continue to form the structural volume base in developing agricultural economies worldwide.

2-wheel drive tractors accounted for the largest 71.8% of the agricultural tractors market share in 2025. These tractors maintain their dominance due to lower upfront costs, simpler maintenance requirements, and their suitability for light tillage, transport, and row-crop farming activities. They are widely preferred in regions such as India, Southeast Asia, and parts of Africa, where small and medium-sized farms prioritize affordability and operational simplicity. Additionally, the segment benefits from extensive dealer networks and lower fuel consumption in lower-horsepower applications. This combination ensures that 2-wheel drive tractors remain the preferred choice for cost-sensitive agricultural operations in several developing economies.

The agricultural tractors market size for the 4-wheel drive tractor segment is projected to grow at the fastest CAGR of 7.6% from 2026 to 2031. The adoption of higher-traction tractor systems is increasing in regions such as North America, Brazil, and Eastern Europe, driven by expanding farm sizes and the need for wider implement usage. Large commercial farms favor 4-wheel drive configurations for their ability to enhance drawbar pull, reduce wheel slippage, and support heavy-duty field operations. Manufacturers are also broadening their premium tractor portfolios with advanced hydraulic systems and precision farming technologies tailored for large-scale farming. The growth in this segment reflects rising productivity demands rather than a complete shift away from traditional 2-wheel drive platforms in global agricultural markets.

Geography Analysis

Asia-Pacific held the largest 38.6% agricultural tractors market share in 2025, supported by strong mechanization demand across India and China. India remained one of the leading tractor-consuming countries globally, primarily due to the widespread adoption of utility tractors on small and medium-sized farms. China continued to enhance agricultural mechanization through increased adoption of advanced farming equipment and the expansion of domestic manufacturing capabilities. Japan and South Korea sustained demand for compact, precision-oriented tractors tailored for specialized agricultural operations. The region benefits from government-backed mechanization programs, improved rural equipment financing access, and growing local manufacturing capacity, which supports cost-effective tractor production and exports to neighboring agricultural economies worldwide.

Africa is projected to grow at the fastest 7.6% CAGR from 2026 to 2031 due to rising mechanization investments and expanding organized procurement programs. Governments in countries such as Nigeria, Ghana, Kenya, and Tanzania are increasing support for farm mechanization through tractor financing initiatives and public-private agricultural modernization programs. The region is transitioning from fragmented equipment purchases to structured distribution and service-provider models, enhancing long-term equipment accessibility. Global manufacturers are also strengthening dealer networks and distribution partnerships to improve market penetration in the region. Growth is particularly robust in countries with expanding commercial farming activities and a heightened policy focus on food security and agricultural productivity improvements.

North America and Europe experienced varied demand trends in 2025 and early 2026, driven by higher interest rates and fluctuating farm profitability, which impacted equipment purchasing decisions. Despite these challenges, replacement demand and the need for ongoing mechanization supported specific markets. According to the Association of Equipment Manufacturers (AEM), total Canadian agricultural tractor sales increased by 1.6% year-to-date as of June 2025, while sales of 4-wheel-drive tractors grew by 24.7%, indicating sustained investment in high-power farm machinery and large-scale agricultural operations . In contrast, several Western European markets saw weaker registrations before demand gradually stabilized.

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Limited

- CLAAS KGaA mbH

- SDF S.p.A.

- Yanmar Holdings Co., Ltd.

- Argo Tractors S.p.A. (ARGO S.p.A.)

- Weichai Lovol Intelligent Agricultural Technology Co., Ltd.

- LS Mtron Ltd. (LS Corp.)

- Daedong Corporation

- International Tractors Limited

- Tractors and Farm Equipment Limited (Amalgamations Group)

- YTO Group Corporation (China National Machinery Industry Corporation)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government mechanization subsidy continuity

- 4.2.2 Precision agriculture integration across installed fleets

- 4.2.3 Replacement demand for an aging tractor fleet

- 4.2.4 High-horsepower and 4-wheel drive adoption on large farms

- 4.2.5 Retrofit-first autonomy and guidance upgrades

- 4.2.6 Specialty-crop electrification in orchards, vineyards, and greenhouses

- 4.3 Market Restraints

- 4.3.1 High acquisition cost and tighter machinery financing

- 4.3.2 Emissions-compliant diesel powertrain cost inflation

- 4.3.3 Weak farm cash flows and seasonal credit access gaps

- 4.3.4 Dealer and service-readiness gap for electric and autonomous models

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Power Output

- 5.1.1 Less than 40 HP

- 5.1.2 40-100 HP

- 5.1.3 101-200 HP

- 5.1.4 More than 200 HP

- 5.2 By Drive Type

- 5.2.1 2-Wheel Drive

- 5.2.2 4-Wheel Drive

- 5.3 By Engine Type

- 5.3.1 Diesel

- 5.3.2 Electric

- 5.3.3 Hybrid

- 5.4 By Tractor Type

- 5.4.1 Utility

- 5.4.2 Row-Crop

- 5.4.3 Orchard and Vineyard

- 5.4.4 Autonomous

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 Russia

- 5.5.3.4 United Kingdom

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Turkey

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra Limited

- 6.4.6 CLAAS KGaA mbH

- 6.4.7 SDF S.p.A.

- 6.4.8 Yanmar Holdings Co., Ltd.

- 6.4.9 Argo Tractors S.p.A. (ARGO S.p.A.)

- 6.4.10 Weichai Lovol Intelligent Agricultural Technology Co., Ltd.

- 6.4.11 LS Mtron Ltd. (LS Corp.)

- 6.4.12 Daedong Corporation

- 6.4.13 International Tractors Limited

- 6.4.14 Tractors and Farm Equipment Limited (Amalgamations Group)

- 6.4.15 YTO Group Corporation (China National Machinery Industry Corporation)

7 Market Opportunities and Future Outlook