PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066492

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066492

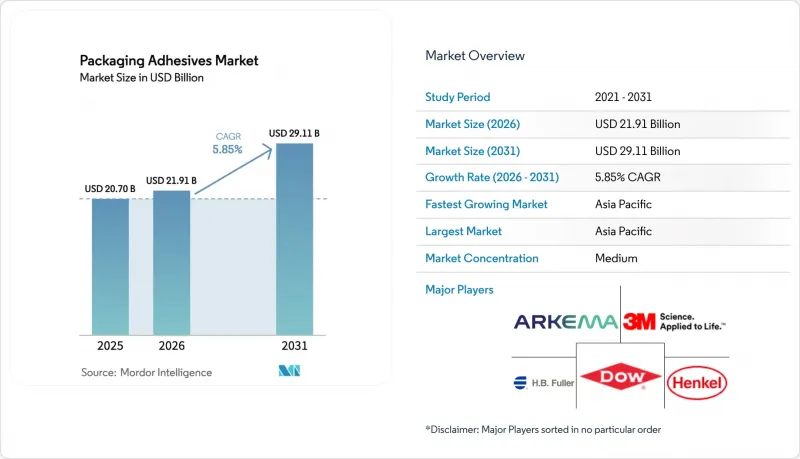

Packaging Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the packaging adhesives market size is expected to grow from USD 20.70 billion in 2025 to USD 21.91 billion in 2026 and is forecast to reach USD 29.11 billion by 2031 at 5.85% CAGR over 2026-2031.

This report is Segmented by Technology (Water-Based, Solvent-Based, and Hot-Melt), Resin Chemistry (Acrylics, Polyurethanes, EVA, Styrenic, and Bio-Based), Application (Flexible Packaging, Cartons, Labels, Sealing, and Others), End-Use Industry (Food and Beverage, Pharmaceuticals, Personal Care, and More), and Geography (Asia-Pacific, North America, and More). Market Forecasts are in Value (USD).

Global Packaging Adhesives Market Trends and Insights

Surging Demand From Food and Beverage Converters

In the food and beverage sector, converters are standardizing adhesive portfolios to meet lamination speeds and adhere to zero-migration mandates. Henkel's launch of Aquanence achieved a reduction in curing time and a decrease in oven energy consumption, leading to shorter production lines and diminished emissions. The rise of mono-material polyethylene pouches amplifies the demand for primers that can adhere to corona-treated films but easily wash off in recycling baths. Chemists are fine-tuning the windows of hydroxyl and carboxyl functionalities to ensure shelf-life integrity while facilitating wash-tank release, a skill often dominated by global suppliers with pilot-line capabilities. Additionally, rapid retort sterilization is pushing converters to favor water-based polyurethanes, which achieve full bond strength quickly. These trends are driving a surge in the adoption of high-performance water-based chemistries in the packaging adhesives market.

E-Commerce-Driven Corrugated and Mailer Growth

In 2025, global parcel volumes surged, driving up the demand for corrugated-box adhesives. Fulfillment centers are now utilizing vision-guided dispensing robots, which can adjust bead width in real-time, leading to a reduction in waste. This level of automation not only solidifies partnerships with suppliers offering digital analytics but also creates a competitive edge against commodity players. Hot-melt EVA copolymers are the go-to choice for high-speed lines, thanks to their optimal open time and green strength. As a result, e-commerce is setting new standards, influencing other segments of the packaging adhesives market.

Volatility in Petrochemical Feedstock Prices

Propylene prices are putting pressure on EVA and polyolefin hot-melt margins. Smaller converters, without access to hedging tools, resort to quarterly surcharges to pass on costs, disrupting contract stability. While an ethylene oversupply tempered prices in H1 2024, delays at Middle Eastern crackers negated those gains by late 2025. Dow's in-house ethylene production underscores the protective benefits of vertical integration. This ongoing volatility not only deters investments in additional capacity but also casts a shadow over the packaging adhesives market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Sustainable Water-Based and Solvent-Free Systems

- AI-Optimised High-Speed Dispensing Lines

- Stringent VOC and Food-Contact Migration Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-based products accounted for a 57.42% share of 2025 revenue, and their 6.19% CAGR keeps them the fastest-growing technology tier. Regulatory VOC caps and converter moves to eliminate solvent ovens anchor this trajectory. Adoption is especially strong on new European and North American lamination lines, where cold-curing polyurethanes reduce energy consumption. Solvent-based options persist in aluminum-foil blisters that demand high peel strength, while hot-melt EVA retains dominance in high-speed case sealing thanks to rapid set times. Pressure-sensitive label demand boosts acrylic emulsions that resist plasticizer migration over multiyear life cycles. Hybrid primer-plus-topcoat systems bridge adhesion gaps on corona-treated polypropylene, allowing continuous high-speed throughput. This mix positions water-based chemistries at the center of long-term value creation for the packaging adhesives market.

EVA held 30.61% of 2025 revenue, leveraging formulations designed for open times ideal for automated carton lines. Premium niches in polyurethanes demand retort or steam sterilization resistance, surpassing 121 °C. Acrylic emulsions, favored for pressure-sensitive labels, resist UV exposure and plasticizer bleed, justifying their price premium. Bio-based resins are growing 6.82% annually, fueled by multi-national brand mandates for renewable carbon by 2030. Sustainability and cryogenic stability coexist in advanced solutions. While styrenic block copolymers lose ground, bio-polyolefins, offering similar peel properties and reduced VOCs, gain traction. Natural starch systems find their niche in corrugated applications, where moisture risk remains minimal. Resin suppliers equipped with pilot lines and analytical labs stand out, customizing blends for a competitive edge in the packaging adhesives market.

Geography Analysis

Asia-Pacific held a commanding 40.35% share in 2025 and will grow 6.62% annually through 2031. In 2025, China's demand surged as automated lines were rolled out, necessitating digitally integrated hot-melt systems. Driven by rising consumption of packaged foods, India experienced growth, highlighted by the addition of water-based capacity in Gujarat. Japan and South Korea carved out high-performance niches, opting for UV-curable labels that set in under 2 seconds. Meanwhile, ASEAN countries enjoyed growth as brands began diversifying their focus beyond China.

In 2025, North America accounted for a significant portion of the global volume, bolstered by advancements in fulfillment automation and a shift towards recyclable mono-material packaging. Hot-melt demand in the U.S. climbed, spurred by the inauguration of new distribution centers. Specialty label usage in Canada's Ontario and Quebec pharma clusters is on the rise, while Mexico's near-shoring initiatives are driving expansions in Monterrey and Queretaro.

Europe, holding a notable market share, is witnessing growth despite its mature status. Germany is at the forefront of bio-based adoption, with the unveiling of a co-developed starch adhesive boasting renewable content in 2025. The U.K. grapples with post-Brexit dossier duplications, incurring added costs per formulation. Meanwhile, France and Italy are capitalizing on luxury cosmetics exports, which increasingly demand holographic pressure-sensitive labels.

Brazil led South America, driving growth in 2025, as the adoption of flexible packaging helped mitigate distribution costs across the continent's expansive geographies. Argentina's growth was largely attributed to packaging for agricultural exports. The Middle East and Africa, while still representing a modest portion of global demand, are advancing annually. This growth is buoyed by Saudi Arabia's investments in food security and a burgeoning pharmaceutical manufacturing sector in South Africa. Collectively, these regional dynamics are fostering multiple growth nodes, ensuring the continued expansion of the packaging adhesives market.

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Dow

- Dymax

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- Paramelt

- Pidilite Industries Limited

- Synthomer plc

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand from food and beverage converters

- 4.2.2 E-commerce-driven corrugated and mailer growth

- 4.2.3 Shift toward sustainable water-based and solvent-free systems

- 4.2.4 AI-optimised high-speed dispensing lines

- 4.2.5 Cold-chain direct-to-consumer packaging needs cryogenic-stable bonds

- 4.3 Market Restraints

- 4.3.1 Volatility in petrochemical feedstock prices

- 4.3.2 Stringent VOC and food-contact migration regulations

- 4.3.3 Delamination challenges in mechanical recycling streams

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Hot-Melt

- 5.2 By Resin Chemistry

- 5.2.1 Acrylics

- 5.2.2 Polyurethanes

- 5.2.3 Ethylene-Vinyl Acetate (EVA)

- 5.2.4 Styrenic Block Copolymers

- 5.2.5 Natural/Bio-based

- 5.3 By Application

- 5.3.1 Flexible Packaging

- 5.3.2 Folding Cartons and Boxes

- 5.3.3 Labels and Tapes

- 5.3.4 Sealing

- 5.3.5 Other Applications (Tissue and Towel Over-wrap, Graphics and Specialty)

- 5.4 By End-Use Industry

- 5.4.1 Food and Beverage

- 5.4.2 Pharmaceuticals and Healthcare

- 5.4.3 Personal Care and Cosmetics

- 5.4.4 Industrial and Consumer Goods

- 5.4.5 E-Commerce Retail Fulfilment

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Dow

- 6.4.6 Dymax

- 6.4.7 Franklin International

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Jowat SE

- 6.4.11 Paramelt

- 6.4.12 Pidilite Industries Limited

- 6.4.13 Synthomer plc

- 6.4.14 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment