PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066502

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066502

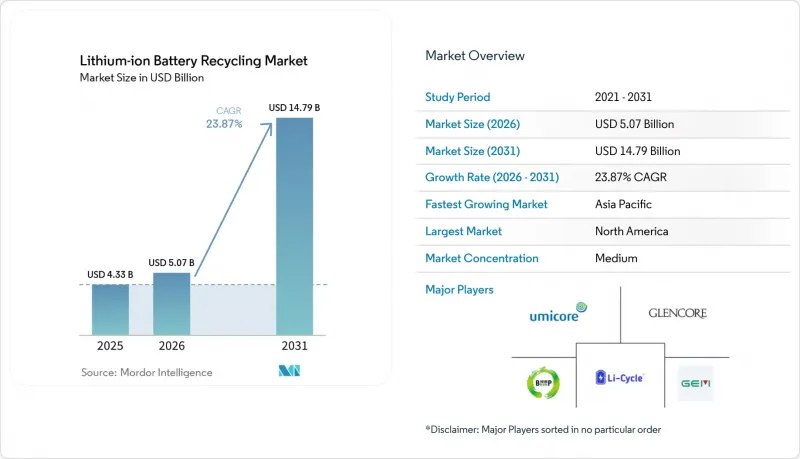

Lithium-ion Battery Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the lithium-ion battery recycling market size was valued at USD 4.33 billion in 2025 and is estimated to grow from USD 5.07 billion in 2026 to reach USD 14.79 billion by 2031, at a CAGR of 23.87% during the forecast period (2026-2031).

This report is Segmented by End-Of-Life Source (Automotive Batteries, and More), Battery Chemistry (NMC, and More), Recycling Technology (Hydrometallurgical, and More), Process Stage (Mechanical Shredding/Sorting, and More), Application of Recovered Materials (Battery-Grade Lithium Compound, and More), End-User Industry (Automotive, and More), and Geography (North America, Asia-Pacific, and More)

Global Lithium-ion Battery Recycling Market Trends and Insights

Accelerating wave of EV battery retirements

Early cohorts of mass-market EVs sold between 2015 and 2018 began hitting end-of-warranty in 2024-2025, sending an estimated 280,000 tonnes of packs into global collection systems. China's electric buses and taxis from the 2016-2018 subsidy boom are now retiring, while Europe's Nissan Leaf and Renault Zoe fleets move into recycling channels. The shift means recyclers can tap higher-value cobalt-rich packs instead of relying on lower-margin manufacturing scrap. Tesla reported that 92% of critical minerals in its 4680 cells can be recovered and looped back into new batteries, validating the economic case for closed loops. A subsequent surge in volumes is expected from 2027-2030 as vehicles sold in the 2019-2022 growth spurt reach retirement.

Tightening global EPR & EU Battery Regulation mandates

The EU Battery Regulation, effective February 2024, sets a 63% collection target by 2027 and 73% by 2030, underpinned by fines of up to 4% of annual turnover for non-compliance. China mandates 65% recycling of power batteries by 2025 through a digital traceability system, and South Korea requires 80% collection by 2028. Automakers, therefore, must finance reverse logistics networks; Volkswagen allocated EUR 200 million in March 2025 to integrate 1,200 dealerships and 350 third-party sites. Compliance costs are driving the lithium-ion battery recycling market toward scale and vertical integration.

Volatile Metal Prices & High Reverse-Logistics Costs

Lithium carbonate's 85% crash between March 2024 and December 2025 dragged black-mass prices down to USD 6,500 per tonne, forcing some recyclers into negative margins. Reverse-logistics costs range from USD 150-250 per tonne because packs are hazmat-classified under UN 3480 rules that require fire-resistant packaging and state-of-charge testing. These structural costs compress margins whenever metals fall.

Other drivers and restraints analyzed in the detailed report include:

- Raw-Material Price Inflation Spurring Closed-Loop Supply Chains

- Step-change yields from next-generation hydro & direct recycling

- Regional Over-Capacity Creating Feedstock Scarcity Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive packs accounted for 63.8% of revenue in 2025, a figure expected to rise as the 2015-2020 vehicle cohort retires. Manufacturing scrap, however, supplies immediate volume, sidestepping collection bottlenecks and enabling rapid ramp-up of hydrometallurgical plants. OEM take-back programs such as GM's Ultium warranty eliminate consumer friction, and higher targets for automotive than portable electronics further tilt flows toward vehicle batteries. The lithium-ion battery recycling market size for automotive sources is set to expand at a 25.3% CAGR, while consumer electronics lags due to fragmented collection and "drawer hoarding."

Manufacturing scrap represented only 7% of tonnage in 2025 but supplied steady, chemistry-homogeneous feedstock that supports direct recycling pilots. As the gigafactories' first-pass yields improve from 89% in 2022 to 96% in 2025, this stream will plateau; nonetheless, minimum-volume clauses in scrap contracts de-risk new capacity investments for recyclers like Umicore.

NMC held a 50.1% share in 2025 thanks to its dominance in long-range EVs and high cobalt content, which sustains favorable economics. LFP is growing fastest as Tesla and BYD deploy the chemistry in standard-range vehicles; however, its zero-cobalt composition erodes intrinsic value, lowering black-mass pricing by 65% relative to NMC. Recyclers, therefore, rely on high throughput and regulatory credits to profit from LFP streams.

LCO remains lucrative in laptops and smartphones, but shrinking device footprints cap tonnage. NCA, LMO, and LTO fill niche roles in high-performance or long-cycle applications. China's draft rule raising the required lithium recovery for LFP from 70% to 85% aims to close the value gap, potentially unlocking a broader economic case for LFP recycling.

Geography Analysis

Asia-Pacific generated 44.6% of global revenue in 2025, buoyed by China's 65% recycling mandate and Brunp's 120,000-tonne capacity. Europe held a 28% share, anchored by Northvolt's Revolt plant and strict EU Battery Regulation targets. North America posted the highest 27.1% CAGR forecast through 2031 as the IRA links tax credits to recycled content thresholds, catalyzing DOE-backed projects such as Redwood Materials' 100 GWh cathode facility.

South America's share sits at 4% but is rising as lithium-rich nations launch domestic recycling pilots. The Middle East and Africa claim 3% but may expand through regional hubs in Singapore and incentives tied to solar-plus-storage installations in Gulf states. Japan and India have announced subsidy programs and draft rules, respectively, yet commercial deployments remain early-stage.

- Umicore SA

- Glencore PLC

- Brunp Recycling (CATL)

- GEM Co., Ltd.

- Li-Cycle Holdings Corp.

- Redwood Materials Inc.

- Ascend Elements (Battery Resources)

- Ecobat

- American Battery Technology Co. (ABTC)

- RecycLiCo Battery Materials

- Retriev Technologies Inc.

- Cirba Solutions

- Duesenfeld GmbH

- TES-AMM Pte Ltd.

- Recupyl SAS

- Raw Materials Company Inc.

- Glencore-Li-Cycle Portovesme JV

- Ganfeng Lithium Co., Ltd.

- Eramet-Suez JV (Recyclage Batteries)

- InoBat-Minerals JV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating wave of EV battery retirements

- 4.2.2 Tightening global EPR & EU Battery Regulation mandates

- 4.2.3 Raw-material price inflation spurring closed-loop supply chains

- 4.2.4 Step-change yields from next-gen hydro & direct recycling

- 4.2.5 OEM design-for-recycling battery packs reducing dismantling cost

- 4.2.6 Emergence of liquid "black-mass" spot markets

- 4.3 Market Restraints

- 4.3.1 Volatile metal prices & high reverse-logistics costs

- 4.3.2 Safety & haz-mat compliance in high-voltage collection

- 4.3.3 Regional over-capacity creating feedstock scarcity risk

- 4.3.4 Low intrinsic value of LFP chemistries

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By End-of-Life Source

- 5.1.1 Automotive Batteries

- 5.1.2 Consumer Electronics Batteries

- 5.1.3 Industrial and ESS Batteries

- 5.1.4 Manufacturing Scrap

- 5.2 By Battery Chemistry

- 5.2.1 Lithium Cobalt Oxide (LCO)

- 5.2.2 Lithium Iron Phosphate (LFP)

- 5.2.3 Lithium Nickel Manganese Cobalt (NMC)

- 5.2.4 Lithium Nickel Cobalt Aluminium (NCA)

- 5.2.5 Lithium Manganese Oxide (LMO)

- 5.2.6 Lithium Titanate (LTO)

- 5.3 By Recycling Technology

- 5.3.1 Hydrometallurgical

- 5.3.2 Pyrometallurgical

- 5.3.3 Direct/Mechanical

- 5.3.4 Hybrid and Emerging (Bio/ Electro-chemical)

- 5.4 By Process Stage

- 5.4.1 Collection and Logistics

- 5.4.2 Dismantling and Discharge

- 5.4.3 Mechanical Shredding/Sorting

- 5.4.4 Black-Mass Production

- 5.4.5 Material Refining and Recovery

- 5.5 By Application of Recovered Materials

- 5.5.1 Cathode Active Materials

- 5.5.2 Anode/Graphite

- 5.5.3 Battery-grade Lithium Compounds

- 5.5.4 Cobalt and Nickel Salts

- 5.5.5 Manganese

- 5.5.6 Others (Cu, Al)

- 5.6 By End-user Industry

- 5.6.1 Automotive

- 5.6.2 Marine

- 5.6.3 Power and Energy Storage

- 5.6.4 Consumer Electronics

- 5.6.5 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Spain

- 5.7.2.5 NORDIC Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 ASEAN Countries

- 5.7.3.6 Australia and New Zealand

- 5.7.3.7 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Colombia

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Egypt

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Umicore SA

- 6.4.2 Glencore PLC

- 6.4.3 Brunp Recycling (CATL)

- 6.4.4 GEM Co., Ltd.

- 6.4.5 Li-Cycle Holdings Corp.

- 6.4.6 Redwood Materials Inc.

- 6.4.7 Ascend Elements (Battery Resources)

- 6.4.8 Ecobat

- 6.4.9 American Battery Technology Co. (ABTC)

- 6.4.10 RecycLiCo Battery Materials

- 6.4.11 Retriev Technologies Inc.

- 6.4.12 Cirba Solutions

- 6.4.13 Duesenfeld GmbH

- 6.4.14 TES-AMM Pte Ltd.

- 6.4.15 Recupyl SAS

- 6.4.16 Raw Materials Company Inc.

- 6.4.17 Glencore-Li-Cycle Portovesme JV

- 6.4.18 Ganfeng Lithium Co., Ltd.

- 6.4.19 Eramet-Suez JV (Recyclage Batteries)

- 6.4.20 InoBat-Minerals JV

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment