PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066592

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066592

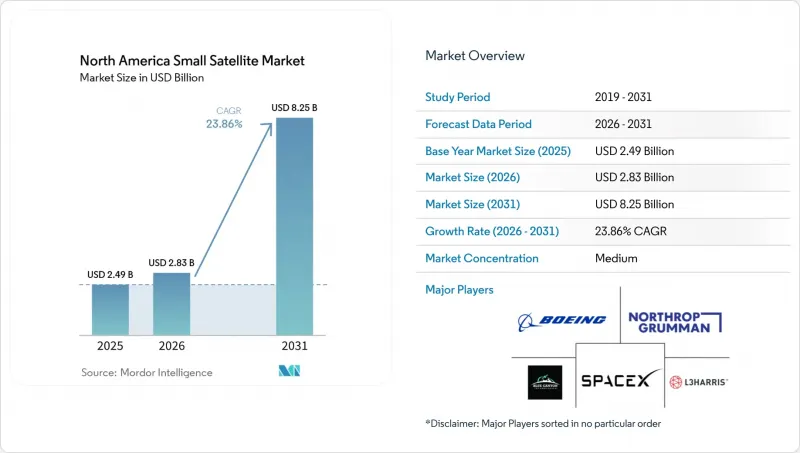

North America Small Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america small satellite market size is projected to expand from USD 2.49 billion in 2025 and USD 2.83 billion in 2026 to USD 8.25 billion by 2031, registering a 23.86% CAGR between 2026 and 2031.

This report is Segmented by Application (Communication, Earth Observation, Navigation, Space Observation, and Others), Orbit (LEO, MEO, and GEO), End-User (Commercial, Government and Civil, and Military), Satellite Mass (Femtosatellites, Picosatellites, Nanosatellites, and More), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Small Satellite Market Trends and Insights

Growing Demand for High-Resolution Earth-Observation Imagery

The growing demand for high-resolution Earth imagery is driven by its applications in agriculture, urban development, security, and disaster relief. Satellites belonging to Maxar Technologies' WorldView Legion series provide highly detailed imagery (30 cm class) and improved revisit frequency, enabling faster responses to time-sensitive incidents such as natural disasters. The upcoming Pelican series from Planet Labs features satellites with onboard computing, enabling efficient data processing and reduced latency. In addition, ICEYE continues to build its SAR constellation to deliver highly detailed (25 cm-class) all-weather imagery. All of these developments are contributing to the move toward subscription-based Earth observation services. Companies like Planet Labs and Maxar Technologies have enabled real-time analysis of high-resolution images in North America.

Declining Launch Costs Driven by Reusable Rockets

Reusable launch systems are significantly altering cost structures by not only reducing prices but also enhancing launch frequency and reliability. SpaceX has achieved over 300 booster landings with Falcon 9 rockets, making them reusable and more cost-effective than other rockets, thereby increasing the competitiveness of its rideshare missions, despite challenges such as rigid schedules and the prioritization of the primary mission. Nevertheless, satellite operators often prefer these missions as they provide better cost efficiency. Simultaneously, new launches by companies such as Rocket Lab, Firefly Aerospace, and Relativity Space have enhanced the capabilities of small launchers. The rapid turnaround of boosters enables small satellite operators to plan flexible, on-demand deployments, reducing capital risks and enhancing the scalability of satellite constellations.

Orbital-Debris Congestion and Stricter Licensing Rules

The growing congestion issue has led to stricter regulations for spacecraft operators, particularly in the US, where licensing requirements for small satellites are becoming more stringent. The Federal Communications Commission (FCC) now requires that low Earth orbit satellites be deorbited within 5 years of completing their missions. This regulation requires operators to implement mitigation measures such as propulsion systems or drag augmentation technology. Additionally, debris mitigation regulations are being updated to ensure adherence to these standards. Satellite operators have recognized benefits, such as faster compliance licensing processes. However, compliance is becoming more expensive due to the growing size of constellations, which adds complexity to design and operations.

Other drivers and restraints analyzed in the detailed report include:

- Rising Private Investment in Large Small-Sat Constellations

- Government Spending on National-Security Small-Sat Programs

- Limited Launch-Slot Availability During Peak Windows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Communication remained the largest slice of the North America small satellite market in 2025, accounting for 48.25% of revenue, chiefly because Starlink surpassed 6,000 active satellites and expanded direct-to-cell coverage. Yet Earth observation is growing faster, at a 24.78% CAGR, as enterprise customers migrate to subscription-based analytics. Planet's EUR 240 million (USD 281.35 million) German capacity deal and Tanager-1's detection of 5,500 methane events illustrate how value shifts from raw pixels to decision-ready insights. Navigation and hybrid PNT payloads such as Xona's centimeter-level Pulsar constellation add diversification, while space-observation missions use commercial buses like Satellogic's to prototype new sensors. A second-order effect is cross-fertilization: hybrid satellites combine broadband radios with optical imagers, maximizing revenue per kilogram. Regulatory hurdles diverge; communication operators benefit from streamlined FCC procedures, whereas Earth-observation missions still navigate export-control reviews that extend lead times. Analytics providers, therefore, push for policy harmonization to accelerate customer onboarding, a trend that should enlarge the North America small satellite market over the forecast period.

LEO captured 45.75% of the revenue share in 2025 because its 500-600 kilometer sweet spot balances revisit rates, launch costs, and link budgets. MEO is now growing at a 24.83% CAGR, led by Xona's planned 258-satellite Pulsar network offering 5-centimeter accuracy and anti-jam resilience. The North America small satellite market for MEO services is poised to grow as agriculture and autonomous-vehicle customers pay premiums for guaranteed integrity and redundancy. GEO missions remain sparsely populated because propulsion budgets push small spacecraft into higher mass classes. Still, Northrop Grumman's Mission Extension Pods show that even sub-500-kilogram craft can make GEO financially viable when electric propulsion is combined with life-extension services. Orbit-specific regulation also shapes demand: the FCC's five-year rule hits LEO hardest, whereas GEO operators focus on longitudinal slot coordination.

List of Companies Covered in this Report:

- Space Exploration Technologies Corp.

- Airbus SE

- The Boeing Company

- Lockheed Martin Corporartion

- ICEYE Oy

- AAC Clyde Space AB

- OHB SE

- Surrey Satellite Technology Ltd.

- Thales Alenia Space

- L3Harris Technologies, Inc.

- Sierra Space Corporation

- Planet Labs PBC

- Northrop Grumman Corporation

- Blue Canyon Technologies, LLC (RTX Corporation)

- Spire Global, Inc.

- Satellogic Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining launch costs driven by reusable rockets

- 4.2.2 Rising private investment in large small-sat constellations

- 4.2.3 Growing demand for high-resolution Earth observation imagery

- 4.2.4 Government spending on national security small-sat programs

- 4.2.5 Shift toward software-defined payloads enabling rapid re-tasking

- 4.2.6 Emergence of on-orbit servicing contracts for small satellites

- 4.3 Market Restraints

- 4.3.1 Orbital-debris congestion and stricter licensing rules

- 4.3.2 RF-spectrum crowding for small-sat communications

- 4.3.3 Limited launch-slot availability during peak windows

- 4.3.4 Insurance-premium hikes for multi-sat rideshare launches

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 By Orbit

- 5.2.1 Low Earth Orbit (LEO)

- 5.2.2 Medium Earth Orbit (MEO)

- 5.2.3 Geostationary Orbit (GEO)

- 5.3 By End-User

- 5.3.1 Commercial

- 5.3.2 Government and Civil

- 5.3.3 Military

- 5.4 By Satellite Mass

- 5.4.1 Femtosatellites

- 5.4.2 Picosatellites

- 5.4.3 Nanosatellites

- 5.4.4 Microsatellites

- 5.4.5 Minisatellites

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Space Exploration Technologies Corp.

- 6.4.2 Airbus SE

- 6.4.3 The Boeing Company

- 6.4.4 Lockheed Martin Corporartion

- 6.4.5 ICEYE Oy

- 6.4.6 AAC Clyde Space AB

- 6.4.7 OHB SE

- 6.4.8 Surrey Satellite Technology Ltd.

- 6.4.9 Thales Alenia Space

- 6.4.10 L3Harris Technologies, Inc.

- 6.4.11 Sierra Space Corporation

- 6.4.12 Planet Labs PBC

- 6.4.13 Northrop Grumman Corporation

- 6.4.14 Blue Canyon Technologies, LLC (RTX Corporation)

- 6.4.15 Spire Global, Inc.

- 6.4.16 Satellogic Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment