PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066594

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066594

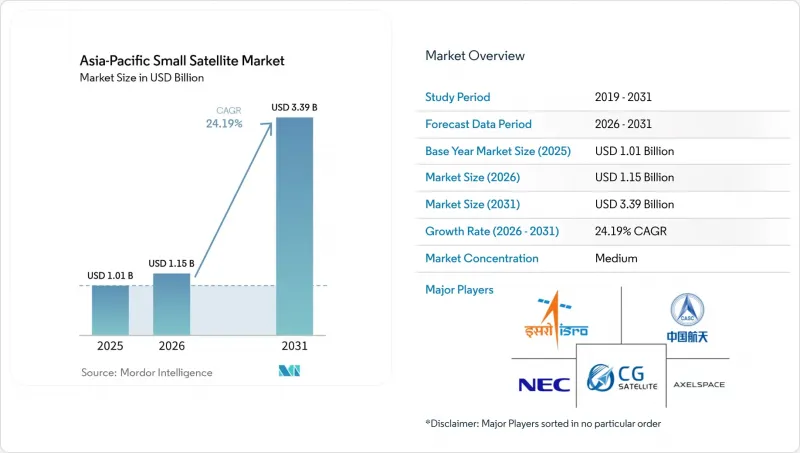

Asia-Pacific Small Satellite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific small satellite market size is projected to grow from USD 1.01 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 3.39 billion by 2031 at 24.19% CAGR over 2026-2031.

This report is Segmented by Application (Communication, Earth Observation, Navigation, Space Observation, and Others), Orbit (LEO, MEO, and GEO), End-User (Commercial, Government and Civil, and Military), Satellite Mass (Femtosatellites, Picosatellites, Nanosatellites, and More), and Geography (China, India, Japan, South Korea, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Small Satellite Market Trends and Insights

Rapid Expansion of Mega-Constellation Programs Across Asia-Pacific

China's launch cadence has entered a new scale phase, reshaping the Asia-Pacific small satellite market. The country recorded 92 orbital launches in 2025 and is targeting as many as 140 launches in 2026, with Guowang and Qianfan expected to use 70 or more of those missions. By April 2026, Guowang had 168 operational satellites against a 13,000-satellite ITU-filed target, while Qianfan had 126 satellites in orbit against a 15,000-satellite approved plan. That scale is pushing the regional supply chain toward higher output in components, integration work, and launch services. It is also lowering unit costs faster than standalone commercial demand would have, improving hardware access for buyers across the Asia-Pacific small satellite market, even when procurement policy still leans toward local sourcing.

Increasing Investments in Government-Led Space Initiatives

Government spending is rising across the region, but the more important shift is that procurement models are becoming more open to private execution in the Asia-Pacific small satellite market. India's Department of Space received INR 13,705.6 crore (USD 1.62 billion) in the FY2026-27 Union Budget, above the revised FY2025-26 level of INR 12,448.6 crore (USD 1.30 billion), and capital expenditure also moved higher. South Korea's 2026 space budget reached KRW 1.2 trillion (USD 790 million) and included satellite information utilization across 42 projects in 13 ministries. These budget decisions are supporting mixed execution models in which private firms build spacecraft, supply payloads, and deliver data services under public mandates. That improves revenue visibility, reduces early commercialization risk, and strengthens domestic manufacturing capacity across the Asia-Pacific small satellite market.

Increasing Spectrum Allocation Congestion Across LEO Bands

Spectrum access is becoming one of the clearest structural constraints on the Asia-Pacific small satellite market. In December 2025, China filed ITU paperwork for 2 additional satellite networks, each comprising 96,714 satellites, bringing potential new Chinese filings to nearly 200,000 satellites. A 2025 analysis published in ScienceDirect found that rapid expansion of LEO constellations is exposing major limitations in the ITU coordination model, with the Ku and Ka bands already facing increasing interference. Smaller operators, therefore, face longer filing cycles, more complex coordination work, and a greater risk that early movers secure high-value slots. That combination can delay deployment plans and reduce commercial flexibility across the Asia-Pacific small satellite market.

Other drivers and restraints analyzed in the detailed report include:

- Declining Launch Costs Driven by Regional Small-Lift Providers

- Growing Demand for Real-Time Earth Observation Analytics

- Rising Costs of Orbital Debris Mitigation Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Communication accounted for 42.25% of the Asia-Pacific small satellite market share in 2025, while Earth observation is projected to expand at 25.78% CAGR through 2031. Communication remains the largest application because mega-constellation deployment, IoT-focused networks, and data relay needs continue to drive the broadest current demand. Earth observation is growing faster because regional buyers now want more than periodic imagery and are shifting spending toward systems that can support faster analysis and more continuous monitoring, changing how operators design payload mixes, revisit strategies, and downstream services across the Asia-Pacific small satellite market.

The Earth observation opportunity is being reinforced by public programs that seek sovereign sensing capability rather than outsourced access alone. Pixxel's 2026 agreement with IN-SPACe combines optical, multispectral, SAR, and hyperspectral systems into a single national constellation, pointing to broader procurement goals than just imaging coverage. Navigation demand is also rising as countries look to supplement or localize positioning and timing capacity for civilian and strategic uses. Space observation and other applications remain smaller, but they still matter for scientific missions, academic programs, and early-stage technology demonstration within the Asia-Pacific small satellite industry.

LEO accounted for 51.75% of revenue in the Asia-Pacific small satellite market in 2025, making it the primary deployment layer for current communication, Earth observation, and IoT missions. Its lead reflects lower launch energy needs, shorter signal latency, and a stronger fit with constellation architectures that require frequent revisit or continuous network growth. MEO is forecast to grow at a 25.83% CAGR through 2031 as operators seek navigation augmentation and medium-latency services that sit between LEO and GEO. GEO still serves selected broadcast and VSAT use cases, but competitive pressure from higher-throughput LEO satellite systems is increasing. Japan's NICT achieved the world's first demonstration of 2 Tbit/s free-space optical communication in December 2025, using small-satellite-mountable terminals, supporting the case for multi-orbit optical relay systems that can improve data transfer across regional networks as the Asia-Pacific small satellite market matures. Even with that progress, continuous-zone coverage requirements will keep part of the demand anchored in GEO and in mixed-orbit architectures across the Asia-Pacific small satellite industry.

List of Companies Covered in this Report:

- Chang Guang Satellite Technology Co. Ltd.

- Indian Space Research Organisation

- ICEYE Oy

- Pixxel Space Technologies, Inc.

- China Aerospace Science and Technology Corporation

- NewSpace India Limited

- Planet Labs PBC

- Blue Canyon Technologies LLC (RTX Corporation)

- Spire Global, Inc.

- Axelspace Corporation

- Satrec Initiative Co., Ltd.

- Dhruva Space Private Limited

- UAB Kongsberg NanoAvionics (Kongsberg Gruppen ASA)

- Airbus SE

- GalaxySpace

- NEC Space Technologies, Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid expansion of mega-constellation programs across Asia-Pacific

- 4.2.2 Increasing investments in government-led space initiatives

- 4.2.3 Declining launch costs driven by regional small-lift providers

- 4.2.4 Growing demand for real-time Earth-observation analytics

- 4.2.5 Rising adoption of CubeSat-based IoT connectivity networks

- 4.2.6 Increasing integration of optical relay systems with 5G NTN infrastructure

- 4.3 Market Restraints

- 4.3.1 Increasing spectrum allocation congestion across LEO bands

- 4.3.2 Rising costs of orbital debris mitigation compliance

- 4.3.3 Limited availability of on-orbit servicing infrastructure in Asia-Pacific

- 4.3.4 Export control restrictions on advanced satellite technologies and components

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Communication

- 5.1.2 Earth Observation

- 5.1.3 Navigation

- 5.1.4 Space Observation

- 5.1.5 Others

- 5.2 By Orbit

- 5.2.1 Low Earth Orbit (LEO)

- 5.2.2 Medium Earth Orbit (MEO)

- 5.2.3 Geostationary Orbit (GEO)

- 5.3 By End-User

- 5.3.1 Commercial

- 5.3.2 Government and Civil

- 5.3.3 Military

- 5.4 By Satellite Mass

- 5.4.1 Femtosatellites

- 5.4.2 Picosatellites

- 5.4.3 Nanosatellites

- 5.4.4 Microsatellites

- 5.4.5 Minisatellites

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 South Korea

- 5.5.5 Australia

- 5.5.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Chang Guang Satellite Technology Co. Ltd.

- 6.4.2 Indian Space Research Organisation

- 6.4.3 ICEYE Oy

- 6.4.4 Pixxel Space Technologies, Inc.

- 6.4.5 China Aerospace Science and Technology Corporation

- 6.4.6 NewSpace India Limited

- 6.4.7 Planet Labs PBC

- 6.4.8 Blue Canyon Technologies LLC (RTX Corporation)

- 6.4.9 Spire Global, Inc.

- 6.4.10 Axelspace Corporation

- 6.4.11 Satrec Initiative Co., Ltd.

- 6.4.12 Dhruva Space Private Limited

- 6.4.13 UAB Kongsberg NanoAvionics (Kongsberg Gruppen ASA)

- 6.4.14 Airbus SE

- 6.4.15 GalaxySpace

- 6.4.16 NEC Space Technologies, Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment