PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066611

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066611

ASEAN Energy Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

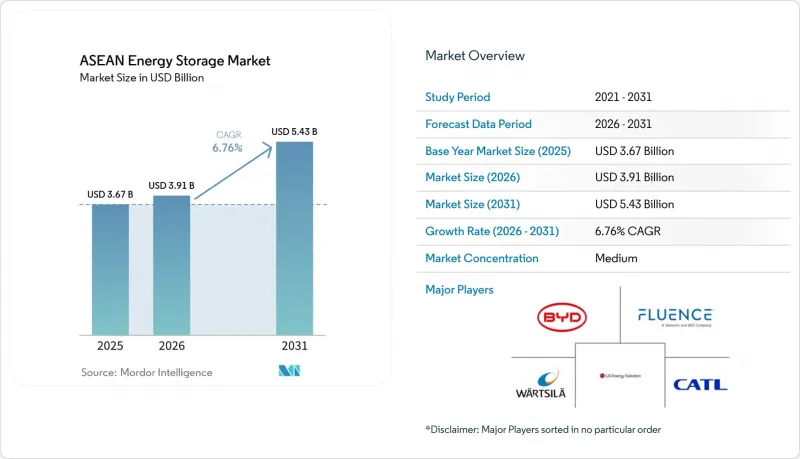

According to Mordor Intelligence, the aSEAN energy storage market size is projected to expand from USD 3.67 billion in 2025 and USD 3.91 billion in 2026 to USD 5.43 billion by 2031, registering a CAGR of 6.76% between 2026 and 2031.

This report is Segmented by Storage Technology (Batteries, Pumped-Storage Hydroelectricity, Thermal Energy Storage, and More), Connectivity (On-Grid, Off-Grid), Application (Grid-Scale Utility, Residential, C&I, Data Centers, Remote/Off-Grid, Others), and Geography (Indonesia, Vietnam, Philippines, Malaysia, Thailand, Singapore, Rest of ASEAN). The Market Forecasts are Provided in Terms of Value (USD).

ASEAN Energy Storage Market Trends and Insights

ASEAN Renewable-Portfolio Targets Accelerating Storage Deployment

The ASEAN energy storage market is being shaped by a higher regional renewable ambition under APAEC 2026-2030, which raised the 2030 target to 30% of primary energy and 45% of installed power capacity. Vietnam's adjusted Power Master Plan VIII moved this shift into project design by requiring centralised solar projects to install BESS equal to at least 10% of installed capacity for 2-hour storage. Indonesia's RUPTL 2025-2034 also gave storage a planned role by assigning 15% of new capacity additions to storage assets alongside a wider renewable build-out. These changes matter because they shift storage from a discretionary balancing tool into a utility procurement category with direct links to renewable auctions and grid planning. The IEA's integration roadmap for Southeast Asia also shows that faster solar and wind additions will need more system flexibility between 2025 and 2028, which keeps storage near the center of regional power policy.

Electricity Demand from C&I Sector Creating Behind-the-Meter Storage Markets

The ASEAN energy storage market is also gaining support from industrial users that need more stable power and better control over outages, curtailment, and operating costs. Grid-scale systems still take the largest application share, but data centres and critical facilities are the fastest-growing application block at 10.3% CAGR through 2031, which shows how strongly reliability-led demand is rising across the region. In Vietnam, storage is moving closer to factories and industrial parks as new planning rules and the formal recognition of storage in the power framework create a clearer path for deployment. This part of the ASEAN energy storage market is important because manufacturers and digital operators value continuity and power quality even when wholesale flexibility markets remain immature. That makes commercial and industrial storage demand more durable in countries where policy is still catching up with system needs.

Capital-Intensity and the Project Finance Gap

High upfront costs remain one of the clearest brakes on the ASEAN energy storage market, especially for long-duration assets and large standalone battery projects. Vietnam shows this clearly because multiple BESS projects remained stalled into early 2026 while pricing rules for standalone storage, ancillary compensation, and capacity payments were still being finalised under Circular 62/2025/TT-BCT. Large pumped hydro projects are moving forward, but many depend on concessional or multilateral funding rather than broad commercial bank participation, as seen in Bac Ai's financing structure and Indonesia's wider state-backed pipeline. This slows the conversion of announced targets into contracted and commissioned capacity across the ASEAN energy storage market. It also leaves smaller developers at a disadvantage because domestic lenders still treat many storage structures as unfamiliar risk.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Stability Issues and Outage Mitigation as an Immediate Procurement Signal

- Island-Grid Resiliency Creating a Parallel Off-Grid Storage Economy

- Ambiguous Storage Asset-Class Regulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pumped-Storage Hydroelectricity held 80.9% of the ASEAN energy storage market size in 2025, which shows how strongly the region still depends on long-established civil infrastructure for bulk storage. That position is reinforced by major project pipelines in Indonesia, Vietnam, and Thailand, where state utilities continue to treat pumped hydro as a strategic balancing asset rather than a niche technology. Vietnam's 1,200 MW Bac Ai pumped storage project entered its main construction phase in 2026 and remains central to the country's effort to absorb more renewable output from high-curtailment regions. Thailand also plans 2,472 MW of additional pumped hydro under PDP 2024 through the Chulabhorn, Vajiralongkorn, and Krathun projects, which confirms that PSH will stay important well beyond the current forecast period.

Battery technologies, however, are where most incremental diversification is taking place in the ASEAN energy storage market. Hydrogen-based storage is the fastest-growing technology segment at 11.1% CAGR from 2026 to 2031, which reflects growing interest in longer-duration flexibility and island-grid applications. Lithium-ion systems remain the main battery choice across utility and behind-the-meter projects, with LFP, NMC, and emerging sodium-ion chemistries shaping the procurement mix. Lower global battery costs are improving the case for utility-scale BESS, while thermal stability and safety are becoming more important in tropical operating conditions. Flow batteries, thermal systems, and compressed air are still early in the region, but they address storage durations that lithium-ion does not serve as efficiently. Safety certification is also becoming a stronger buying factor, which gives structured system integrators a clearer advantage in public and utility tenders.

List of Companies Covered in this Report:

- BYD Co Ltd

- Contemporary Amperex Technology Ltd (CATL)

- LG Energy Solution

- Wartsila Oyj Abp

- GS Yuasa Corporation

- NGK Insulators Ltd

- Fluence Energy Inc

- Sungrow Power Supply Co Ltd

- Tesla Inc (Megapack)

- Siemens Energy AG

- Hitachi Energy Ltd

- Toshiba Corp

- Samsung SDI Co Ltd

- Kokam Co Ltd

- Pylon Technologies Co Ltd

- AlphaESS Co Ltd

- NEC ES (portfolio legacy)

- SEC Battery Company

- Mitsubishi Power

- EnerSys

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in electricity demand from C&I sector

- 4.2.2 Grid-stability issues & outage mitigation needs

- 4.2.3 ASEAN renewable-portfolio targets acceleration

- 4.2.4 Falling Li-ion battery costs

- 4.2.5 Digital twin-enabled optimisation of storage

- 4.2.6 Island-grid resiliency & diesel-offset programmes

- 4.3 Market Restraints

- 4.3.1 Capital-intensity & limited project finance

- 4.3.2 Ambiguous storage asset-class regulation

- 4.3.3 Community push-back on pumped hydro

- 4.3.4 Nickel-manganese supply-chain volatility

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Storage Technology

- 5.1.1 Batteries (Lithium-ion, Solid-State Li, Sodium-ion, Lead-acid, Sodium-Sulfur, and Flow Batteries (Vanadium, Zinc-Bromine))

- 5.1.2 Pumped-Storage Hydroelectricity (PSH)

- 5.1.3 Thermal Energy Storage (Sensible Heat (Molten Salt, Water), Latent Heat (Phase-Change Materials), Thermochemical)

- 5.1.4 Compressed Air Energy Storage

- 5.1.5 Liquid Air/Cryogenic Storage

- 5.1.6 Hydrogen-Based Storage (Power-to-H2-to-Power)

- 5.1.7 Other Technologies (Flywheel Energy Storage, Gravity-Based Storage, Iron-Air, Zinc-Air)

- 5.2 By Connectivity

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By Application

- 5.3.1 Grid-Scale Utility (Front-of-Meter)

- 5.3.2 Residential Behind-the-Meter

- 5.3.3 Commercial and Industrial Behind-the-Meter

- 5.3.4 Data Centers and Critical Facilities

- 5.3.5 Remote and Off-Grid/Microgrids

- 5.3.6 Others (Transportation and Rail Electrification, EV-Charging Infrastructure, Transmission and Distribution Deferral)

- 5.4 By Geography

- 5.4.1 Indonesia

- 5.4.2 Vietnam

- 5.4.3 Philippines

- 5.4.4 Malaysia

- 5.4.5 Thailand

- 5.4.6 Singapore

- 5.4.7 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 BYD Co Ltd

- 6.4.2 Contemporary Amperex Technology Ltd (CATL)

- 6.4.3 LG Energy Solution

- 6.4.4 Wartsila Oyj Abp

- 6.4.5 GS Yuasa Corporation

- 6.4.6 NGK Insulators Ltd

- 6.4.7 Fluence Energy Inc

- 6.4.8 Sungrow Power Supply Co Ltd

- 6.4.9 Tesla Inc (Megapack)

- 6.4.10 Siemens Energy AG

- 6.4.11 Hitachi Energy Ltd

- 6.4.12 Toshiba Corp

- 6.4.13 Samsung SDI Co Ltd

- 6.4.14 Kokam Co Ltd

- 6.4.15 Pylon Technologies Co Ltd

- 6.4.16 AlphaESS Co Ltd

- 6.4.17 NEC ES (portfolio legacy)

- 6.4.18 SEC Battery Company

- 6.4.19 Mitsubishi Power

- 6.4.20 EnerSys

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment