PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066629

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066629

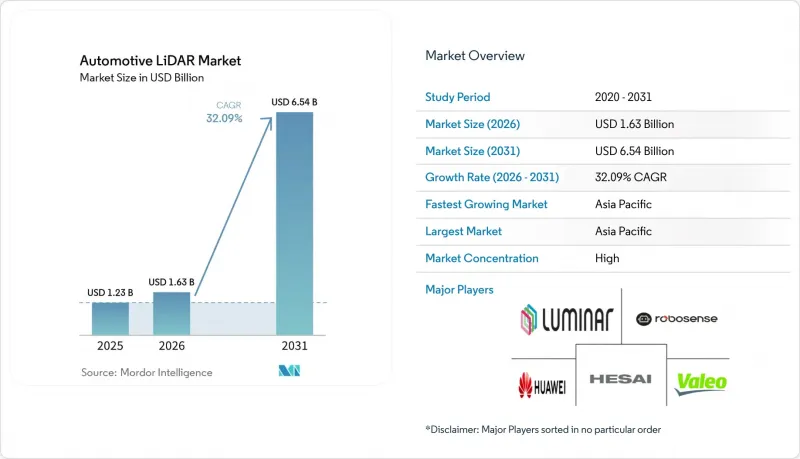

Automotive LiDAR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the automotive LiDAR market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.63 billion in 2026 to reach USD 6.54 billion by 2031, at a CAGR of 32.09% during the forecast period (2026-2031).

This report is Segmented by Application (Robotic Vehicles and ADAS [Level 2+ / 2++ and More]), Technology Type (Mechanical/Spinning and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Range (Short/Mid-Range and Long-Range), Installation Position (Roof-Mounted and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive LiDAR Market Trends and Insights

Rapid ASP Decline Unlocking Mid-Priced Vehicle Adoption

Average selling prices for solid-state units fell more than 30% between 2023 and 2025, bringing fully automotive-qualified flash sensors below USD 400. Cost reduction stems from silicon photonics integration, wafer-level optics, and back-end test automation, enabling installation on premium compact cars instead of only luxury flagships. PreAct Technologies and several Chinese fabs report six-figure monthly output volumes, illustrating economies of scale. The downward price curve broadens the total addressable automotive LiDAR market by enabling optional packages at sub-USD 1,500 price points for consumers. A greater installed base further drives learning effects that compress cost over the medium term.

Early-stage FMCW Sensor Breakthroughs

FMCW architectures emit continuous low-power light and use coherent detection to measure both distance and radial velocity. Aurora Innovation's FirstLight sensor shows reliable detection of 10% reflectivity objects at 400 meters, a critical requirement for highway speeds. Because FMCW separates each unit's frequency chirp, crosstalk is virtually eliminated in dense traffic, and immunity to solar interference improves all-weather uptime. OEM roadmaps indicate FMCW deployment on 2027-model premium vehicles in North America and China, with production tooling already underway at several OSAT partners. These advances suggest FMCW will command an outsized share of incremental revenue growth in the automotive LiDAR market through the forecast period.

Persistent Eye-Safety Limits on Peak Power

IEC 60825-1 Class 1 rules cap maximum permissible exposure, limiting optical power for long-range roof units. Vendors, therefore, rely on larger receiver apertures, avalanche photodiodes, and advanced signal processing rather than raw transmit power. While safety guarantees protect public health, design latitude narrows and drives up cost for precision optics and thermal management. These engineering trade-offs slow the rollout of ultra-long-range products and marginally dampen the automotive LiDAR market growth outlook.

Other drivers and restraints analyzed in the detailed report include:

- UNECE R157 and China NCAP 2026 Autonomy Mandates

- Mass-Production Deals Between Tier-1s and Cloud AV Stacks

- Radar/Camera Fusion Roadmaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, ADAS accounted for 85.12% of the Automotive LiDAR Market, reflecting its mainstream adoption. Additionally, ADAS is the fastest-growing segment, with a 37.88% CAGR, driven by city-level permits and ride-hailing fleet orders. ADAS Level 3 and Level 4 programs bridge the gap: German premium OEMs already ship production Level 3 highway pilots, and Chinese mobility companies operate supervised Level 4 services in over 10 metropolitan areas. Higher autonomy levels require multiple sensors, redundancy, and full-stack validation, raising average content per vehicle and powering the next wave of the market size expansion.

Scaling to full autonomy shifts value from hardware to continuous OTA upgrades. Subscription models for highway self-driving add revenue streams that justify higher sensor bills, and data collected by Level 5 fleets feeds iterative perception improvements. As these platforms mature, they reinforce a virtuous cycle: wider data coverage supports safer algorithms, in turn unlocking permits for broader operations. This flywheel underpins bullish long-range forecasts despite early-stage volumes.

In 2025, mechanical spinning units captured 62.15% of the revenue share in the Automotive LiDAR Market, due to their proven field performance, comprehensive 360-degree coverage, and established manufacturing lines. Yet their moving parts create reliability concerns for a 10-year automotive design life, and form-factor constraints complicate stylistic integration. Solid-state approaches, including MEMS beam steering, optical phased arrays, and flash topologies, step in with fully sealed modules and lower cost trajectories. Within this solid-state cohort, FMCW is the breakout sub-category, projected at 47.46% CAGR and expected to reach double-digit share before 2031.

Valeo continues to iterate its second-generation Scala hybrid scanner, while Luminar brings high-channel-count pulsed time-of-flight into series production. Huawei and Hesai invest heavily in 905-nm pulsed and 1,550-nm FMCW pipelines, seeking to hedge technology bets across different vehicle classes. This pluralistic landscape ensures that no single architecture dominates all use cases, even as FMCW captures the performance leadership narrative.

Geography Analysis

In 2025, the Automotive LiDAR Market saw Asia-Pacific commanding a dominant revenue share of 41.75%, with China as the epicenter of sensor deployment. Provincial subsidies worth up to CNY 10,000 per L3-ready vehicle, extended through 2027, increase penetration of battery electric SUVs and sedans. Domestic supply chains spanning wafer fab to final assembly compress cost and shorten lead times, reinforcing regional dominance. South Korea and Singapore add pilot zones and smart-highway projects, further expanding regional demand. The market in Asia-Pacific is forecast to grow at a 25.9% CAGR, the highest across all regions.

Autonomous trucking corridors linking Texas, Arizona, and California, and consumer appetite for hands-free highway assist, push a 23.2% CAGR. Aurora, Ouster, and Aeva operate domestic facilities that reduce import reliance, while U.S. export control on certain 1,550 nm VCSEL epitaxy encourages local alternative suppliers. Canada's winter testing grounds add niche demand for all-weather FMCW products.

Europe follows with a 20.4% CAGR, reflecting advanced regulation and conservative consumer uptake. UNECE-based rules originate in Europe, but national type-approval processes remain stringent, slowing high-volume delivery. However, German, Swedish, and French premium brands install multi-LiDAR configurations to meet L3 highway pilot requirements, making the region an influential technology trendsetter. Smaller yet notable opportunities arise in the Gulf Cooperation Council, where smart-city mega-projects embed autonomous shuttles into new urban designs. Africa and Latin America post CAGRs of 21.3% and 19.6% respectively on lower bases, driven by mining haulage automation and public-sector fleet modernization.

- Hesai Technology (Hesai Group)

- RoboSense Technology Co., Ltd.

- Huawei Technologies Co., Ltd.

- Valeo SA

- Luminar Technologies Inc.

- Continental AG

- ZF Friedrichshafen AG

- Innoviz Technologies Ltd.

- Ouster Inc.

- Velodyne LiDAR Inc.

- Aeva Inc.

- AEye Inc.

- LeddarTech Holdings Inc.

- Seyond

- LIVOX

- Blickfeld GmbH

- SiLC Technologies Inc.

- Insight LiDAR

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid ASP decline unlocking mid-priced vehicle adoption

- 4.2.2 Early-stage FMCW LiDAR sensor breakthroughs extend detection range above 400 m

- 4.2.3 UNECE R157 and China NCAP 2026 autonomy ratings mandate higher-resolution perception

- 4.2.4 Mass-production deals between tier-1s and cloud AV stacks

- 4.2.5 Chinese provincial subsidies for L3-ready sensor suites

- 4.2.6 Automaker OTA business models monetising highway LiDAR subscriptions

- 4.3 Market Restraints

- 4.3.1 Persistent eye-safety rules limit peak power on long-range, roof-mounted units

- 4.3.2 Radar/Camera sensor fusion cost-down roadmap slows LiDAR attach-rate in sub-USD25k cars

- 4.3.3 Export-control scrutiny on 1,550 nm GaAs VCSELs restricts cross-border supply chains

- 4.3.4 Reliability concerns of dynamic beam-steering MEMS mirrors in above 10-year duty cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 LiDAR Component Ecosystem

- 4.8 Integration of LiDAR in ADAS Vehicles

- 4.9 Automotive LiDAR Technology Roadmap (2020-2030)

- 4.10 Pricing Trend Analysis

- 4.11 Porter's Five Forces

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Buyers

- 4.11.3 Bargaining Power of Suppliers

- 4.11.4 Threat of Substitutes

- 4.11.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Application

- 5.1.1 Robotic Vehicles

- 5.1.2 ADAS

- 5.1.2.1 Level 2+ / 2++

- 5.1.2.2 Level 3 / 4

- 5.1.2.3 Level 5

- 5.2 By Technology Type

- 5.2.1 Mechanical/Spinning

- 5.2.2 Solid-State (MEMS, Flash)

- 5.2.3 FMCW

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Range

- 5.4.1 Short / Mid-Range (Up to 150 m)

- 5.4.2 Long-Range (Above 150 m)

- 5.5 By Installation Position

- 5.5.1 Roof-Mounted

- 5.5.2 Grille / Bumper

- 5.5.3 Headlamp-Integrated

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Hesai Technology (Hesai Group)

- 6.4.2 RoboSense Technology Co., Ltd.

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Valeo SA

- 6.4.5 Luminar Technologies Inc.

- 6.4.6 Continental AG

- 6.4.7 ZF Friedrichshafen AG

- 6.4.8 Innoviz Technologies Ltd.

- 6.4.9 Ouster Inc.

- 6.4.10 Velodyne LiDAR Inc.

- 6.4.11 Aeva Inc.

- 6.4.12 AEye Inc.

- 6.4.13 LeddarTech Holdings Inc.

- 6.4.14 Seyond

- 6.4.15 LIVOX

- 6.4.16 Blickfeld GmbH

- 6.4.17 SiLC Technologies Inc.

- 6.4.18 Insight LiDAR

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment