PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066695

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066695

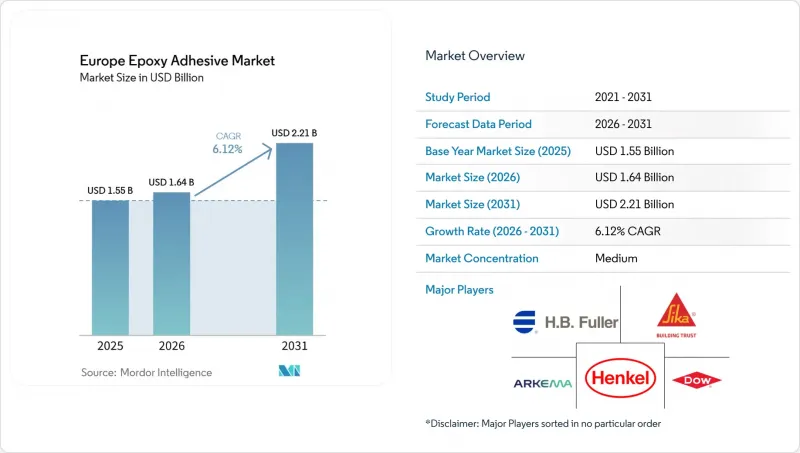

Europe Epoxy Adhesive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe epoxy adhesives market size is projected to be USD 1.55 billion in 2025, USD 1.64 billion in 2026, and reach USD 2.21 billion by 2031, growing at a CAGR of 6.12% from 2026 to 2031.

This report is Segmented by End-User Industry (Aerospace and Defense, Automotive, Marine, Electrical and Electronics, Construction, and Other End-User Industries), Technology (Reactive, Solvent-Borne, UV-Cured, and Water-Borne), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, NORDIC Countries, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Epoxy Adhesive Market Trends and Insights

Electric Vehicle and Lightweight-Vehicle Structural Bonding Boom

In battery housings, crash structures, and mixed-material body components, epoxy adhesives are increasingly supplanting traditional methods like welds, rivets, and mechanical fasteners. Modified with ceramic fillers, thermally conductive epoxies achieve a thermal conductivity of >=2 W/m*K and lap-shear strengths of up to 30 MPa. This capability facilitates module-to-cooling-plate interfaces that effectively manage heat and endure crash loads. The diversity in cell formats, such as cylindrical, pouch, and blade, drives a distinct demand for epoxies, pressure-sensitive tapes, and gap-fillers. This collective demand is expanding the footprint of the European structural adhesives market in vehicle platforms. As lightweighting trends push OEMs towards aluminum and fiber-reinforced polymer parts, the need arises for chemically compatible adhesives. These adhesives must withstand thermal cycling from -40 °C to 80 °C without delaminating. Supplier portfolios, including SikaForce and WEVO-CHEMIE, now highlight silicone grades with initial adhesion exceeding 2 MPa and thermal conductivities approaching 1.5 W/m*K, specifically for EV modules. Furthermore, pilot lines that incorporate robotic metering and in-line infrared curing are not only reducing takt times but also enhancing adoption rates in German and French gigafactories. Given these trends, the European epoxy adhesives market for battery applications is poised for double-digit volume growth from 2026 to 2028.

VOC/REACH-Driven Shift to High-Performance Systems

In April 2025, the European Commission proposed capping authorizations at 10 years and implementing an "essential use" filter, tightening the compliance window for legacy solvent-borne systems. BASF-Sika's Baxxodur EC 151an, an amine-based epoxy hardener, boasts 90% lower VOC emissions compared to traditional amine systems and reduces cure time by two-thirds, showcasing how regulation drives innovation. As OEMs chase ISO 14001 certifications, water-borne and UV-cured chemistries are winning more designs in appliances, engineered wood, and electronics. Henkel's acquisition of ATP Adhesive Systems, with a portfolio over 90% water-based, strategically boosts Henkel's foothold in Europe's epoxy adhesives market, targeting the automotive, electronics, and construction sectors. This regulatory trend suggests a sustained CAGR premium for sustainable grades throughout the forecast period.

BPA and Epichlorohydrin Feedstock Price Volatility

In 2025, European epoxy resin prices fell by 12% due to market oversupply, leading to tighter margins and heightened procurement uncertainties. Westlake shut down its Pernis facility, which produced epoxy resins, BPA, and epichlorohydrin, in June 2025. This was soon followed by Ineos's announcement in October 2025 to close its Rheinberg units for epichlorohydrin and chlorine. Meanwhile, India's imposition of anti-dumping duties shifted Asian epoxy flows towards Europe, exacerbating price fluctuations. To navigate this volatility, adhesive formulators are turning to multi-vendor contracts and are even delving into bio-based feedstocks. Despite these measures, the unpredictability of near-term costs continues to impact working-capital decisions in the European epoxy adhesives market.

Other drivers and restraints analyzed in the detailed report include:

- Offshore Wind Blade Upsizing

- Robotic Dispensing Adoption in Assembly Lines

- Toxicological/Regulatory Re-classification of BPA

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the automotive sector accounted for 23.18% of Europe's epoxy adhesives market, highlighting a consistent preference for epoxies in enhancing body stiffness and crash absorption. As the industry electrifies, there's a growing demand for thermally conductive gap-fillers, flame-retardant potting resins, and debond-on-demand solutions, all pivotal for battery recycling. With lap-shear strength requirements set between 15-23 MPa and service temperatures reaching up to 80 °C, the average value per vehicle sees a boost, allowing the European epoxy adhesives market to maintain its premium pricing. The electronics sector is on a 6.58% CAGR trajectory, driven by 5G rollouts and the miniaturization of power modules. These advancements necessitate adhesives boasting thermal conductivity of >=3 W/m*K and high elongation to counter thermal mismatches. In Germany and Poland, assembly lines for Mini-LEDs are now opting for low-viscosity silicone gels that cure at room temperature, a move that slashes energy consumption. A diverse demand spanning consumer devices, industrial automation, and photovoltaic inverters ensures steady volume growth, even amidst potential softening in consumer electronics cycles.

Construction, ranking third in volume, is buoyed by EU renovation subsidies. These subsidies promote the use of low-VOC, high-grab polyurethanes, especially for bonding facades and insulation panels. The marine, aerospace, and renewable-energy sectors each have their unique demands. For instance, they seek niche high-performance grades, such as moisture-tolerant methacrylate adhesives for composite hulls and flame-retardant epoxies. The latter must adhere to FAR 25.853 standards concerning fire, smoke, and toxicity in aircraft interiors. Energy applications, particularly in offshore wind, prioritize crack-resistant epoxies, ensuring they maintain a fracture toughness of >=25 kJ/m2 over a 30-year lifecycle. Together, these diverse segments bolster end-market resilience, shielding the European epoxy adhesives market from the cyclical fluctuations of any single sector.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF

- Beardow Adams

- DELO Industrial Adhesives

- Dow Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- Jowat SE

- MAPEI S.p.A.

- Momentive Performance Materials

- PARKER HANNIFIN CORP

- Sika AG

- Soudal Holding N.V.

- tesa Tapes (India) Private Limited

- ThreeBond Europe

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electric Vehicle and Lightweight-Vehicle Structural Bonding Boom

- 4.2.2 Construction Renovation Surge (EU Green Deal)

- 4.2.3 VOC/REACH-Driven Shift to High-Performance Systems

- 4.2.4 Offshore Wind Blade Upsizing

- 4.2.5 Robotic Dispensing Adoption in Assembly Lines

- 4.3 Market Restraints

- 4.3.1 BPA and Epichlorohydrin Feedstock Price Volatility

- 4.3.2 Toxicological/Regulatory Re-classification of BPA

- 4.3.3 Rise of Bio-based and Hybrid Alternatives

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Distribution Channel Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Aerospace and Defense

- 5.1.2 Automotive

- 5.1.3 Marine

- 5.1.4 Electrical and Electronics

- 5.1.5 Construction

- 5.1.6 Energy and Power

- 5.1.7 Other End-User Industries

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV-Cured

- 5.2.4 Water-borne

- 5.3 By Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF

- 6.4.4 Beardow Adams

- 6.4.5 DELO Industrial Adhesives

- 6.4.6 Dow Inc.

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 ITW Performance Polymers

- 6.4.11 Jowat SE

- 6.4.12 MAPEI S.p.A.

- 6.4.13 Momentive Performance Materials

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Sika AG

- 6.4.16 Soudal Holding N.V.

- 6.4.17 tesa Tapes (India) Private Limited

- 6.4.18 ThreeBond Europe

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment