PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066706

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066706

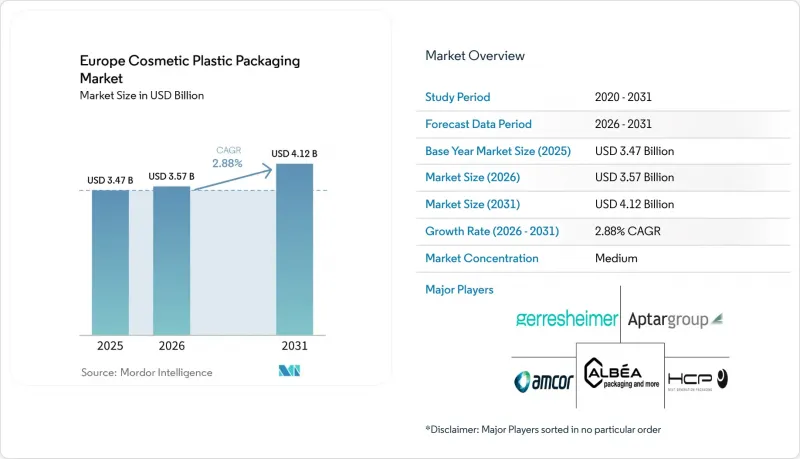

Europe Cosmetic Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, europe cosmetic plastic packaging market size in 2026 is estimated at USD 3.57 billion, growing from 2025 value of USD 3.47 billion with 2031 projections showing USD 4.12 billion, growing at 2.88% CAGR over 2026-2031.

This report is Segmented by Resin Type (PET, PE, PP, Biodegradable and Bio-Based Plastics, and More), Product Type (Bottles, Tubes and Sticks, Pumps and Dispensers, and More), Application (Skin Care, Hair Care, Make-Up Products, and More), Sustainability Profile (Conventional Packaging, Sustainable Packaging), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe Cosmetic Plastic Packaging Market Trends and Insights

Premiumisation of Skin-Care and Dermo-Cosmetics

Clinical skin-care lines require airless pumps and vacuum chambers that safeguard unstable actives, lifting packaging cost-per-unit by 25-40% yet allowing brands to preserve 40-60% margin premiums. German and French consumers display the strongest willingness to pay for dermatologically validated formats, turning those two countries into anchor markets for high-spec packaging. Leading converters such as Gerresheimer reported EUR 1.9 billion (USD 2.05 billion) revenue in 2024, citing 15% cosmetic growth linked to barrier-enhanced plastic systems. EMA guidance blurs the cosmetic-pharma boundary, compelling suppliers to document leachables and extractables, which further cements the role of precision injection-molding and specialty resins. Over the medium term, premiumization is expected to add 0.7 percentage points to the Europe cosmetic plastic packaging market CAGR as more mass manufacturers launch quasi-pharma sub-brands.

Rise of Refill/Re-Use Business Models in Prestige Beauty

Prestige houses are switching to refill pods and cartridges that slash virgin-plastic intensity by up to 85%, a shift accelerated by EPR fee rebates tied to re-use ratios. Luxury brands recover the higher capex for reverse logistics through SKU lock-in and 30-50% price premiums on initial pack purchases. Quadpack logged 25% revenue growth from refill formats in 2024, and major maisons target 60% refillable penetration by 2027. NFC-enabled authentication extends the consumer journey while furnishing regulators with auditable data on reuse cycles. Although roll-out costs slow mid-market adoption, long-term (>= 4 years) impact is pegged at +0.5 percentage points for the Europe cosmetic plastic packaging market.

Inflation-Driven Material Cost Spikes Squeezing Converters

Polyethylene price volatility of 18-25% during 2024 wiped 8-12% off converter gross margins, as outlined by European Central Bank industrial price data. Smaller firms lacking hedging programs were forced into M and A or market exit, fuelling consolidation that has lifted the Herfindahl-Hirschman Index by 11 % since 2023. Electricity-intensive recycling operations faced twin pressure from energy tariffs and feedstock scarcity, temporarily dampening PCR usage despite regulatory incentives. Until spot prices normalize, the restraint subtracts 0.4 percentage points from near-term growth in the Europe cosmetic plastic packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Owner Commitments to >=50% PCR Plastics by 2030

- Rapid Growth of Indie Brands Using Short-Run Digital Printing

- Rising EPR Fees for Non-Recyclable Packs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene continues to underpin 33.72% of 2025 volumes, reaffirming its cost-performance balance across bottles, caps and flexible films in the Europe cosmetic plastic packaging market. Yet biodegradable plastics are rising 4.55% annually, their advance linked more to EPR fee relief and corporate scorecard metrics than to absolute cost advantage. Europe cosmetic plastic packaging market size tied to biodegradable grades is forecast to reach USD 0.64 billion by 2031, propelled by PHA's superior moisture barrier relative to PLA for lotions and wipes. Production capacity, however, remains 2.4 million tonnes across all uses, a mismatch that sustains price premiums of 2-3X over PE.

The Europe cosmetic plastic packaging market pivots further as converters experiment with enzymatic depolymerization of cellulose blends to match PET-like clarity while matching compostability standards. Patent activity validates momentum: 127 biodegradable-packaging patents were granted in 2024, 35% of them cosmetic-focused. As brand owners publicize recycled-content progress, chemical compatibility tests intensify, especially for retinoid serums, where monomer migration risk remains tightly regulated. Because EPR schemes reward mono-material PE tubes and jars that incorporate PCR, polyethylene still expands in absolute tonnage even as share slips to an anticipated 30.1% by 2031.

Bottle formats keep 32.10% share through their ubiquity in shampoos, micellar waters, and body lotions, but average wall thickness is declining under light-weighting programs, trimming resin usage per unit by 8-12%. Digital print adoption transforms tubes and sticks into the fastest-growing 3.55% CAGR cohort, providing bespoke graphics for seasonal drops and influencer capsules across the Europe cosmetic plastic packaging market. The Europe cosmetic plastic packaging market size attributable to tubes will add nearly USD 0.16 billion between 2026 and 2031 as indie brands favor MOQ-friendly runs.

Airless pumps, once a luxury exclusive, migrated into mid-tier acne treatments in 2024, widening the addressable base for precision components. However, the EU tethered-cap rule is compelling a rethink of hinge geometry for flip-top dispensers under 3 liters, escalating tooling spends by 20-25%. Pouches, historically niche in hair-conditioner refills, now capture eco-trade-up consumers, given 25-35% material savings versus rigid bottles. Still, recyclability trade-offs for barrier laminates temper momentum outside high-return-rate markets such as Germany.

List of Companies Covered in this Report:

- Albea S.A.

- HCP Packaging Co., Ltd.

- Gerresheimer AG

- Amcor plc

- AptarGroup, Inc.

- Cosmopak USA LLC

- Quadpack Industries, S.A.

- Libo Cosmetics Co., Ltd.

- Mpack Poland Sp. z o.o.

- Politech Sp. z o.o.

- Huhtamaki Oyj

- Rieke Corporation (TriMas Corporation)

- Berlin Packaging LLC

- Mktg Industry S.r.l.

- Silgan Dispensing Systems Corporation

- Coveris Holdings S.A.

- Wipak Oy

- International Paper Company

- Takemoto Packaging, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumisation of skin-care and dermo-cosmetics

- 4.2.2 Rise of refill/re-use business models in prestige beauty

- 4.2.3 Brand-owner commitments to >=50% PCR plastics by 2030

- 4.2.4 Rapid growth of indie brands using short-run digital printing

- 4.2.5 EU Single-Use Plastics Directive catalysing design change

- 4.2.6 Adoption of tethered caps ahead of 2024 deadline

- 4.3 Market Restraints

- 4.3.1 Inflation-driven material cost spikes squeezing converters

- 4.3.2 Retailer "no-plastics" private-label pledges

- 4.3.3 Limited recycling streams for coloured / multilayer PET

- 4.3.4 Rising EPR fees for non-recyclable packs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 The Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Resin Type

- 5.1.1 Polyethylene Terephthalate (PET)

- 5.1.2 Polyethylene (PE)

- 5.1.2.1 High-Density Polyethylene (HDPE)

- 5.1.2.2 Low-Density and Linear-LDPE

- 5.1.2.3 Linear Low-Density Polyethylene (LLDPE)

- 5.1.3 Polypropylene (PP)

- 5.1.4 Biodegradable and Bio-based Plastics

- 5.1.5 Other Resin Types

- 5.2 By Product Type

- 5.2.1 Bottles

- 5.2.2 Tubes and Sticks

- 5.2.3 Pumps and Dispensers

- 5.2.4 Pouches

- 5.2.5 Other Product Types

- 5.3 By Application

- 5.3.1 Skin Care

- 5.3.2 Hair Care

- 5.3.3 Make-up Products

- 5.3.4 Deodorants and Fragrances

- 5.3.5 Other Applications

- 5.4 By Sustainability Profile

- 5.4.1 Conventional Packaging

- 5.4.2 Sustainable Packaging

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Albea S.A.

- 6.4.2 HCP Packaging Co., Ltd.

- 6.4.3 Gerresheimer AG

- 6.4.4 Amcor plc

- 6.4.5 AptarGroup, Inc.

- 6.4.6 Cosmopak USA LLC

- 6.4.7 Quadpack Industries, S.A.

- 6.4.8 Libo Cosmetics Co., Ltd.

- 6.4.9 Mpack Poland Sp. z o.o.

- 6.4.10 Politech Sp. z o.o.

- 6.4.11 Huhtamaki Oyj

- 6.4.12 Rieke Corporation (TriMas Corporation)

- 6.4.13 Berlin Packaging LLC

- 6.4.14 Mktg Industry S.r.l.

- 6.4.15 Silgan Dispensing Systems Corporation

- 6.4.16 Coveris Holdings S.A.

- 6.4.17 Wipak Oy

- 6.4.18 International Paper Company

- 6.4.19 Takemoto Packaging, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment