PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066711

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066711

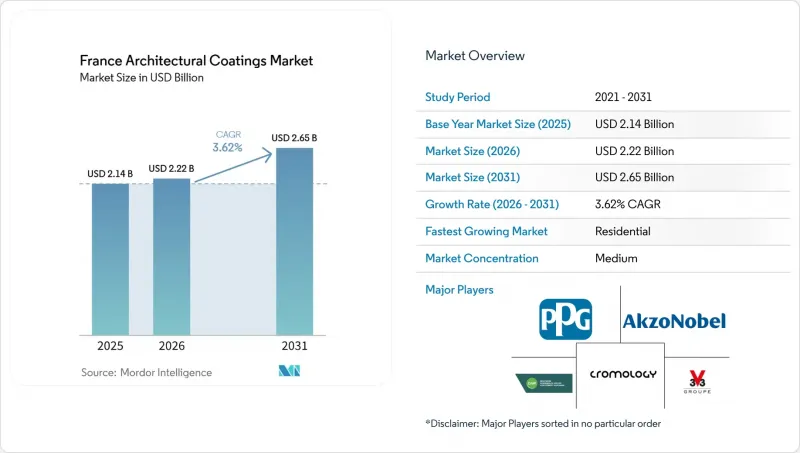

France Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the france architectural coatings market size is expected to increase from USD 2.14 billion in 2025 to USD 2.22 billion in 2026 and reach USD 2.65 billion by 2031, growing at a CAGR of 3.62% over 2026-2031.

This report is Segmented by End-User Industry (Commercial, Residential), Technology (Solvent-Borne, Water-Borne), Resin Type (Acrylic, Alkyd, Epoxy, Polyester, Polyurethane, Other Resin Types). The Market Forecasts are Provided in Terms of Value (USD).

France Architectural Coatings Market Trends and Insights

Mandatory Sustainability-Driven Renovations

France has enacted Decree 2011-321, mandating that all interior paints display an emissions label. This label's A+ class sets formaldehyde limits at 10 µg/m3 and Total Volatile Organic Compounds (TVOC) at 1,000 µg/m3, standards that are more stringent than the European Union Lowest Concentration of Interest (EU-LCI) guidelines. The zero-interest PAR+ advance, offering up to EUR 50,000 for energy renovations, faces challenges as 2026 subsidy reductions to MaPrimeRenov' and diminished Certificats d'Economies d'Energie (CEE) (Energy Savings Certificates) credits shrink the pool of eligible projects. Demand is increasingly directed towards low-emission, certified coatings because of the RGE contractor certification. However, with funding becoming tighter, manufacturers are pivoting towards self-funded premium refurbishments and commercial retrofits driven by Environmental, Social, and Governance (ESG) considerations. Builders who adjust their formulations to meet the stricter 2025 EU Ecolabel criteria stand to gain a competitive edge. These regulations are driving the growth of high-performance water-borne systems in France's architectural coatings market.

Shift to Water-Based Binders to Meet VOC Caps

Since 2010, EU Directive 2004/42/EC has capped VOC levels at 30 g/L for interior matt paints, effectively sidelining solvent-borne products from homes. The 2025 revision of the EU Ecolabel tightens the TVOC limit to 300 µg/m3 after 28 days and introduces ceilings on TiO2 process emissions. This compels a further shift towards advanced water-borne chemistries. AkzoNobel's RUBBOL WF 3350 demonstrates that bio-based acrylics, containing 20% renewable carbon, can achieve durability targets. Furthermore, self-crosslinking acrylics now provide block resistance without the need for volatile coalescents, bridging historical performance gaps. Consequently, water-borne formulas are poised to strengthen their dominance in the French architectural coatings market.

Spike in Titanium Dioxide Prices and Supply Shocks

In February 2025, Venator raised TiO2 prices by EUR 300 per tonne, citing surging energy and CO2-credit costs. This price hike translates to an additional EUR 60 per finished tonne for wall paints containing 20% TiO2, accounting for about 3 to 4% of the ex-factory value. The EU Ecolabel's new regulation caps sulfate discharge at 300 kg per TiO2 tonne, leading to heightened compliance costs for pigment manufacturers. While hiding-power extenders can reduce TiO2 usage by 20 to 30%, the need for consistent performance limits their widespread adoption. As a result, the architectural coatings market in France feels the squeeze, prompting selective price adjustments and reformulations.

Other drivers and restraints analyzed in the detailed report include:

- Pro-Contractor Loyalty-Reward Platforms by Retail Chains

- AI-Enabled Color-Matching Kiosks in DIY Stores

- Home-Improvement Spend Squeeze from High Mortgage Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, residential projects dominated the France architectural coatings market with 67.94% market share, and they are projected to achieve a CAGR of 4.05% through 2031. Younger homeowners are increasingly opting for stay-and-upgrade strategies. With trade labor in short supply, DIY projects now account for over half of the market execution. This trend has heightened the demand for user-friendly products, particularly single-coat solutions that merge primer and topcoat functionalities. While cuts to MaPrimeRenov' and CEE credits are set to diminish subsidized thermal retrofits in 2026, they concurrently invigorate a niche for aesthetic refreshes, funded by household savings. As a result, the residential segment continues to be the driving force behind the France architectural coatings market.

New non-residential output for commercial and institutional buildings is projected to rise by a modest 0.5% in 2026. The office sector is lagging, hindered by hybrid work models that delay tenant relocations. However, sectors like data centers, healthcare, and educational institutions are carving out specialized niches, emphasizing the need for hygienic and fire-retardant systems. Furthermore, as ESG finance gains traction, property owners are increasingly turning to low-VOC paints to attain coveted green-building certifications. Even with a slowdown in construction starts, retrofit mandates from the Tertiary Decree are bolstering baseline demand, highlighting the resilience of the France architectural coatings industry amidst challenging macroeconomic conditions.

List of Companies Covered in this Report:

- AkzoNobel N.V.

- CIN S.A.

- Cromology

- DAW SE (Caparol)

- Farrow & Ball Ltd.

- Group V33

- Jotun

- Meffert AG Farbwerke

- Nippon Paint Holdings Co. Ltd.

- PPG Industries Inc.

- The Sherwin Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory Sustainability-Driven Renovations

- 4.2.2 Surge in DIY Interior-Refresh Purchases Post-COVID

- 4.2.3 Shift to Water-based Binders to Meet VOC Caps

- 4.2.4 Pro-Contractor Loyalty-Reward Platforms by Retail Chains

- 4.2.5 AI-Enabled Colour-Matching Kiosks in French DIY Stores

- 4.3 Market Restraints

- 4.3.1 Spike in Titanium-Dioxide Prices and Supply Shocks

- 4.3.2 Labour Shortages in Skilled Painting Contractors

- 4.3.3 Home-Improvement Spend Squeeze from High Mortgage Rates

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Commercial

- 5.1.2 Residential

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.3 By Resin Type

- 5.3.1 Acrylic

- 5.3.2 Alkyd

- 5.3.3 Epoxy

- 5.3.4 Polyester

- 5.3.5 Polyurethane

- 5.3.6 Other Resin Types

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Products and Services, Recent Developments)

- 6.4.1 AkzoNobel N.V.

- 6.4.2 CIN S.A.

- 6.4.3 Cromology

- 6.4.4 DAW SE (Caparol)

- 6.4.5 Farrow & Ball Ltd.

- 6.4.6 Group V33

- 6.4.7 Jotun

- 6.4.8 Meffert AG Farbwerke

- 6.4.9 Nippon Paint Holdings Co. Ltd.

- 6.4.10 PPG Industries Inc.

- 6.4.11 The Sherwin Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment