PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066713

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066713

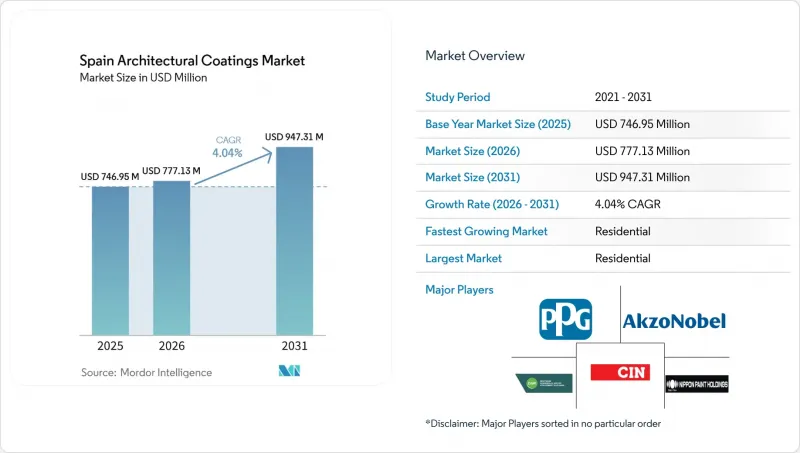

Spain Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the spain architectural coatings market size was valued at USD 0.75 billion in 2025 and is estimated to grow from USD 0.78 billion in 2026 to reach USD 0.95 billion by 2031, at a CAGR of 4.04% during the forecast period (2026-2031).

This report is Segmented by End-User Industry (Commercial, Residential), Technology (Solvent-Borne, Water-Borne), Resin Type (Acrylic, Alkyd, Epoxy, Polyester, Polyurethane, Other Resin Types), and Geography (Spain). The Market Forecasts are Provided in Terms of Value (USD).

Spain Architectural Coatings Market Trends and Insights

Residential-Renovation Stimulus Funds Boost Repaint Demand

Spain has extended its three-tier energy-renovation tax deductions until 2026. Households can now claim grants and deductions from tax, provided their primary energy consumption decreases by at least 30%. Multi-family buildings are rushing to book facade upgrades before the grant window closes in late 2026, signaling a surge in demand. Contractors are increasingly bundling coatings with external insulation composite systems, leading to a notable rise in their contract share. Thanks to the State Housing Plan 2026-2030, government grants are covering 40-80% of retrofit costs for vulnerable households, speeding up project approvals. In response, suppliers are enhancing their just-in-time logistics to align with the accelerated 12- to 18-month renovation cycle, predominantly centered in urban areas.

EU "Renovation Wave" Doubles Facade-Upgrade Rate Through 2030

By 2030, Spain mandates that every non-residential building must surpass the performance of the current bottom 16%. This push aligns Spain's deep-renovation rate with the EU's annual target of 3%. With around 14 million homes poorly insulated, there's a significant market opportunity. In Catalonia's RENOVERTY roadmap, facade packages, featuring rigid insulation boards topped with acrylics, are now standard, priced between EUR 15 and 30 per m2. Suppliers, benefiting from faster cash conversion, gain an edge as coatings are applied early in the retrofit sequence, unlike those tied to window or Heating, Ventilation, and Air Conditioning (HVAC) trades.

Volatile TiO2 and Acrylic-Resin Prices Squeeze Margins

In 2025, disruptions at the Red Sea and Panama Canal led to a re-routing of freight from China to Europe, causing a 15-20% quarter-over-quarter swing in spot prices for titanium dioxide and acrylic resin. While multinationals typically hedge against such input fluctuations, smaller Spanish enterprises often bear the brunt of these shocks. As a response, these Small and Medium-sized Enterprises (SME) are reformulating their products, opting for lower-pigment hybrid binders that prioritize cost stability over hiding power.

Other drivers and restraints analyzed in the detailed report include:

- Sharp Rise in Coastal Climate-Resilience Standards

- Smart / Photocatalytic Coatings Encouraged in Urban Air-Quality Zones

- Stricter VOC / SVHC Limits Raise Reformulation Costs for SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spain's architectural coatings market, driven predominantly by the residential end-user industry capturing 66.78% of the market, is set to grow at a projected CAGR of 4.24% through 2030. Grants covering up to 80% of retrofit costs, coupled with tax deductions linked to achieving 30% energy savings, are spurring more frequent repaint cycles in apartment blocks. Multi-family managers are opting for water-borne acrylic wall paints for interiors. For exteriors, they prefer breathable silicate or silicone-acrylic facades, which effectively prevent moisture entrapment behind newly installed insulation boards. Contractors are bundling these coatings with external insulation composite systems, priced between EUR 80 to 180 per m2, leading to a surge in order aggregation.

In the commercial segment, which includes offices, retail spaces, hotels, and public assets, growth is slower. This is due to stretched permitting cycles and fragmented procurement processes across Spain's 17 autonomous communities. Renovation efforts in non-residential spaces primarily focus on HVAC and lighting systems, with paints being addressed later. This sequence has tempered volume growth to below 4%. However, hospitals and schools are now specifying antimicrobial, low-odor coatings. Shopping centers are also showing a preference for anti-graffiti finishes. These trends present lucrative opportunities for suppliers offering certified hygienic or protective product lines.

List of Companies Covered in this Report:

- AkzoNobel N.V.

- BARBOT

- BASF

- CIN, S.A.

- DAW SE

- Jotun

- JUNO

- Nippon Paint Holdings Co., Ltd.

- Pinturas Decolor

- PPG Industries, Inc.

- Sherwin-Williams Company

- The Barpimo Group

- TITAN

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Residential-renovation stimulus funds boost repaint demand

- 4.2.2 EU "Renovation Wave" doubles facade upgrade rate through 2030

- 4.2.3 DIY e-commerce channels widen consumer access and color choice

- 4.2.4 Sharp rise in coastal climate-resilience standards needs high-durability exterior paints

- 4.2.5 Smart/photocatalytic coatings encouraged in urban air-quality zones

- 4.3 Market Restraints

- 4.3.1 Skilled-applicator shortage inflates project lead-times

- 4.3.2 Volatile TiO2 and acrylic resin prices squeeze margins

- 4.3.3 Stricter VOC/SVHC limits raise reformulation costs for SMEs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By End-User Industry

- 5.1.1 Commercial

- 5.1.2 Residential

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.3 By Resin Type

- 5.3.1 Acrylic

- 5.3.2 Alkyd

- 5.3.3 Epoxy

- 5.3.4 Polyester

- 5.3.5 Polyurethane

- 5.3.6 Other Resin Types

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 AkzoNobel N.V.

- 6.4.2 BARBOT

- 6.4.3 BASF

- 6.4.4 CIN, S.A.

- 6.4.5 DAW SE

- 6.4.6 Jotun

- 6.4.7 JUNO

- 6.4.8 Nippon Paint Holdings Co., Ltd.

- 6.4.9 Pinturas Decolor

- 6.4.10 PPG Industries, Inc.

- 6.4.11 Sherwin-Williams Company

- 6.4.12 The Barpimo Group

- 6.4.13 TITAN

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment