PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066724

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066724

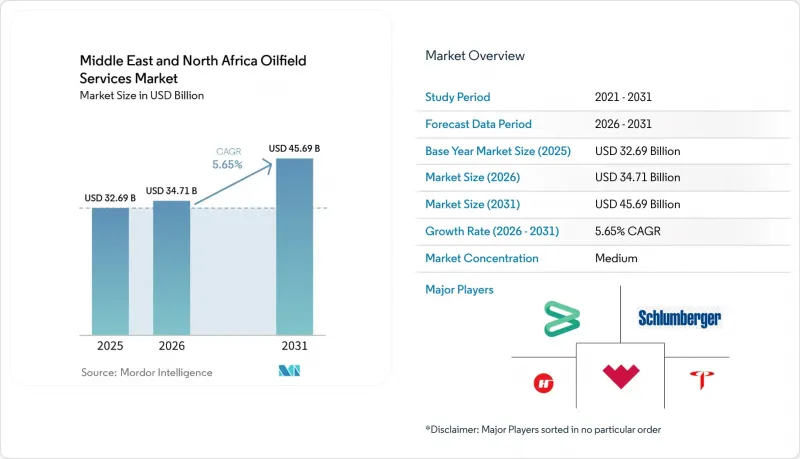

Middle East and North Africa Oilfield Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the middle east and North Africa Oilfield Services Market size was valued at USD 32.69 billion in 2025 and is estimated to grow from USD 34.71 billion in 2026 to reach USD 45.69 billion by 2031, at a CAGR of 5.65% during the forecast period (2026-2031).

This report is Segmented by Service Type (Drilling Services, Completion Services, Other Services), Location (Onshore, Offshore), Well Type (Conventional, Unconventional), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, Algeria, Egypt, Libya, Morocco, Rest of Middle East and North Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East and North Africa Oilfield Services Market Trends and Insights

Rising Drilling Activity Backed by USD 143 Billion E&P Budgets Through 2030

Regional exploration and production budgets of USD 143 billion for 2025-2030 underpin a land-rig count that the International Energy Agency expects to climb 31% over the prior five-year span. Saudi Aramco alone committed USD 7 billion in 2025 to keep 680 rigs active, accentuating the Middle East & North Africa oilfield services market's dependence on sustained drilling intensity. Algeria earmarked USD 60 billion for 1,450 wells targeting tight-gas prospects, extending service demand into North Africa. Kuwait is channeling USD 3.9 billion into offshore Phase 2 exploration to unlock 4.5 billion BOE and add 150,000 bpd by 2035. High-pressure, high-temperature zones, where a single well can cost over USD 20 million, amplify requirements for premium drillstrings, mud-logging, and managed-pressure drilling systems. These allocations reinforce a multi-year backlog across the Middle East & North Africa oilfield services market, incentivizing contractors to expand fleets and local workshops.

Accelerated Gas-Focused Megaprojects (Jafurah, North Field)

Saudi Aramco's USD 100 billion Jafurah program targets 2 bcf/d of sales gas by 2030, necessitating continuous horizontal drilling and intensive multi-stage fracturing. Schlumberger captured a multi-billion-dollar five-year stimulation contract that redefines completion-service intensity in the Middle East & North Africa oilfield services market. Qatar's North Field East and West phases will lift LNG capacity to 142 mtpa by 2030, creating long-cycle subsea-tree, pipeline, and accommodation-vessel demand. Awards to TechnipFMC, Saipem, and Chinese yards secure fabrication slots yet concentrate schedule risk: delays in gas-processing trains can idle rigs and spread cost overruns across the service chain. These megaprojects anchor the Middle East & North Africa oilfield services market size outlook, but they also heighten exposure to commissioning milestones.

Oil-Price Volatility and OPEC+ Production Quotas

OPEC+ carried 3.24 million bpd of cuts into 2026, adding only a 206,000 bpd uptick for April. Brent traded between USD 70 and USD 85 per barrel in Q1 2026, a band that supports maintenance capital but discourages ultra-deepwater or tight-oil exploration in high-cost areas. Quota discipline presses member states to prioritize value over volume, postponing marginal field final-investment decisions and dampening short-cycle rig demand. Service companies with fixed-rate fleet contracts shoulder utilization swings, whereas those with performance-linked pricing secure partial downside protection. The constraint subtracts up to 0.9 percentage points from the regional growth trajectory of the Middle East & North Africa oilfield services market.

Other drivers and restraints analyzed in the detailed report include:

- National Oil Companies' Localization Mandates Boosting Service Tenders

- Digital-Oilfield Adoption (AI Rigs, Real-Time Reservoirs)

- Geopolitical Flashpoints and Sanctions Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drilling services retained 38.9% of the Middle East and North Africa oilfield services market share in 2025, driven by Saudi Aramco's land-rig fleet expansion and Qatar's offshore appraisal campaigns. Yet production and intervention services are forecast to grow at 7.7% annually, reflecting artificial-lift retrofits, coiled-tubing jobs, and real-time surveillance across maturing assets. The Middle East & North Africa oilfield services market size for stimulation contracts is rising as Jafurah alone will require 1,000 horizontal wells by 2030, each demanding multi-stage fracturing and proppant logistics. Western majors capture high-tech completion scopes, while regional contractors compete on commodity cementing and wellhead fabrication. Other services, seismic, marine logistics, aviation, and nascent decommissioning, round out revenue, buoyed by Egypt's 101 exploration wells in 2026 and Algeria's 24-block bid round.

Parallel competitive dynamics shape pricing: performance-based completion contracts in unconventional plays fetch premiums, whereas drilling day-rates remain range-bound by OPEC+ quota uncertainty. High-pressure, high-temperature projects off the UAE and Kuwait's Mutriba field require specialized drilling fluids and downhole tools, allowing suppliers to command higher margins. In contrast, mid-depth land wells across North Africa stay cost-focused, favoring contractors with localized supply chains. Over 2026-2031, the Middle East & North Africa oilfield services market sees the fastest percentage growth in production and intervention, but drilling retains the largest absolute revenue pool, reflecting the region's sheer rig intensity.

List of Companies Covered in this Report:

- Schlumberger

- Halliburton

- Baker Hughes

- China Oilfield Services (COSL)

- Weatherford International

- Transocean

- Valaris

- Nabors Industries

- Expro Group

- National Energy Services Reunited (NESR)

- Saipem

- Petrofac

- KCA Deutag

- Arabian Drilling

- Shelf Drilling

- Maersk Drilling

- TechnipFMC

- CGG

- NOV (National Oilwell Varco)

- Halliburton Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising drilling activity backed by $143 bn E&P budgets through 2030

- 4.2.2 Accelerated gas-focused megaprojects (Jafurah, North Field)

- 4.2.3 National oil companies' localisation mandates boosting service tenders

- 4.2.4 Digital-oilfield adoption (AI rigs, real-time reservoirs)

- 4.2.5 Ultra-deep HP/HT discoveries demanding high-spec services

- 4.2.6 Early carbon-capture & hydrogen pilots creating niche service demand

- 4.3 Market Restraints

- 4.3.1 Oil-price volatility and OPEC+ production quotas

- 4.3.2 Geopolitical flashpoints & sanctions risk

- 4.3.3 Local-content rules squeezing foreign firms' margins

- 4.3.4 Critical talent shortage for next-gen digital rigs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Drilling Services

- 5.1.2 Completion Services (Cementing, Hydraulic Fracturing)

- 5.1.3 Production and Intervention Services

- 5.1.4 Other Services (OSV, seismic, decomm., aviation)

- 5.2 By Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Well Type

- 5.3.1 Conventional

- 5.3.2 Unconventional

- 5.4 By Geography

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Kuwait

- 5.4.5 Algeria

- 5.4.6 Egypt

- 5.4.7 Libya

- 5.4.8 Morocco

- 5.4.9 Rest of Middle East and North Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Schlumberger

- 6.4.2 Halliburton

- 6.4.3 Baker Hughes

- 6.4.4 China Oilfield Services (COSL)

- 6.4.5 Weatherford International

- 6.4.6 Transocean

- 6.4.7 Valaris

- 6.4.8 Nabors Industries

- 6.4.9 Expro Group

- 6.4.10 National Energy Services Reunited (NESR)

- 6.4.11 Saipem

- 6.4.12 Petrofac

- 6.4.13 KCA Deutag

- 6.4.14 Arabian Drilling

- 6.4.15 Shelf Drilling

- 6.4.16 Maersk Drilling

- 6.4.17 TechnipFMC

- 6.4.18 CGG

- 6.4.19 NOV (National Oilwell Varco)

- 6.4.20 Halliburton Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment