PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066742

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066742

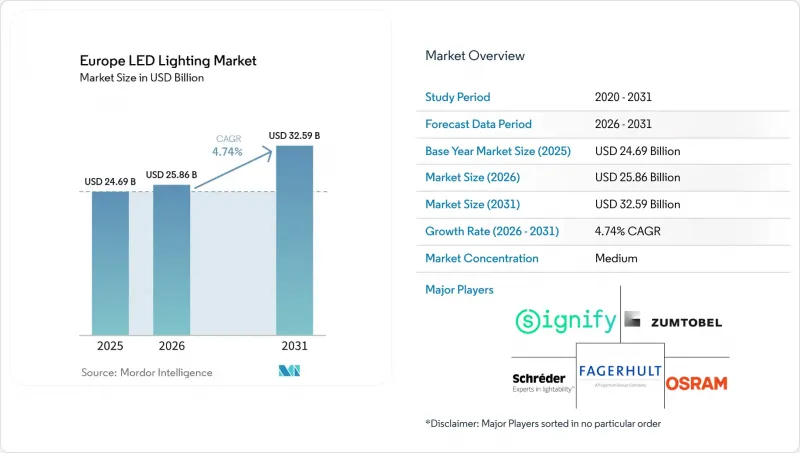

Europe LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe lED lighting market size was valued at USD 24.69 billion in 2025 and is forecasted to grow from USD 25.86 billion in 2026 to USD 32.59 billion by 2031, growing at a CAGR of 4.74% from 2026 to 2031.

This report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and More), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, Hospitality, Industrial, and More), End User (Indoor, Outdoor, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe LED Lighting Market Trends and Insights

Stringent EU Energy-Efficiency Regulations Drive Baseline Demand

The Europe LED lighting market is benefiting from a regulatory framework that now reaches beyond efficiency and into product structure, documentation, and lifecycle performance. Regulation (EU) 2019/2020 set minimum efficacy thresholds for LED lamps, and the newer Ecodesign for Sustainable Products Regulation extended the compliance burden into durability, reparability, and recycled-content disclosure. This has raised the cost of non-compliance, especially as EPREL registration and data validation have become more visible enforcement tools across the region. The European Commission also stated that the current ecodesign and energy-labelling program helped cut final EU energy consumption by 12% in 2023, while avoiding 145 million tonnes of CO2 emissions and supporting 346,000 jobs, which shows why policy support remains firm rather than temporary. The Digital Product Passport will add another layer from 2026 onward, which means the Europe LED lighting market will continue to reward manufacturers that can manage engineering, traceability, and regulatory reporting at scale. Premium brands are also gaining support in specification-led projects because requirements such as stricter flicker and stroboscopic performance have made technical quality easier to verify during procurement.

Rapid Phase-Out of Halogen and Fluorescent Lamps Creates a Structural Replacement Pipeline

The Europe LED lighting market continues to draw demand from the 2023 EU phase-out of T5 and T8 fluorescent tubes because replacement behavior typically trails regulation by several maintenance cycles. That lag matters because many offices, retail sites, hospitals, and municipal facilities are still working through old installed bases that were not replaced immediately after the sales ban. A hospital retrofit in Slovakia showed a 52% reduction in annual energy use, falling from 93,728 kWh to 45,063 kWh, while yearly cost savings exceeded EUR 23,000 (USD 25,070), which keeps the payback case visible for public and institutional buyers. The replacement cycle is also larger than a simple lamp swap because many T8 conversions require control-gear updates and commissioning work, which pushes more projects toward connected retrofits instead of basic maintenance spend. Public tenders continue to reinforce that pipeline, as seen in the Szemud Commune project in Poland, where 436 LED replacements were contracted through 2026 under a municipal modernization program. This keeps the Europe LED lighting market supported by a replacement wave that has not yet fully worked through the region's non-residential and public infrastructure stock.

Price-Sensitive Retrofit Payback Periods Constrain SME Adoption

The Europe LED lighting market still faces a clear adoption gap among smaller businesses because full connected retrofits require higher upfront spending than many SMEs can absorb in one budget cycle. In Ireland alone, 248,000 SMEs occupied 109,000 buildings, yet only 4% had undergone deep retrofitting by 2025, which illustrates how slowly smaller occupiers move even when the long-term efficiency case is positive. This constraint is more visible in Southern and Eastern Europe, where lower electricity prices and tighter capital budgets weaken the near-term return case for basic retrofits. Financing models can help, but they often require energy audits, credit screening, and contract structures that many smaller operators see as complex or time-consuming. Whitecroft Lighting's circular relight program for Currys showed what scale can achieve, refurbishing 77 stores, reusing more than 6,500 luminaires, and reducing energy use and greenhouse gas emissions by 40%. The problem is that individually owned SMEs rarely have that purchasing leverage, so the Europe LED lighting market still loses some conversion volume where investment decisions remain short-cycle and highly cash sensitive.

Other drivers and restraints analyzed in the detailed report include:

- Falling LED Cost Per Lumen Expands The Addressable Market

- Corporate Net-Zero Commitments Accelerate Commercial Retrofits Beyond Minimum Compliance

- Supply-Chain Volatility for Rare-Earth Phosphors Introduces Margin and Availability Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires and fixtures held 57.63% of the Europe LED lighting market share in 2025, which kept this category firmly ahead of lamps in value terms. This lead reflects the shift from lamp-only replacement toward integrated fixture upgrades, where compliance, controls, and service life are assessed at the full-product level rather than through a simple source swap. The Europe LED lighting market has therefore moved more of its value into complete luminaire systems, especially in commercial and public projects where specification, installation time, and documentation all matter. Zumtobel's TECTON II modular continuous-row system showed how suppliers are competing on labor efficiency as much as on output, with a stated 71% saving in installation time compared with conventional configurations.That matters in a market where contractor availability, compliance paperwork, and retrofit downtime often shape procurement decisions as much as unit cost.

The lamps segment is smaller, but it is still forecasted to grow at a 5.02% CAGR through 2031, which makes it the fastest-moving product category in the Europe LED lighting market. This growth is tied to the replacement of banned fluorescent formats and to municipal programs that continue to remove older sodium and conventional lighting points from public estates. The lamp category remains relevant where full fixture replacement is not yet necessary, or where operators want a staged conversion that limits immediate capital spend. Regulation (EU) 2019/2020 also keeps durability standards high, including lumen-maintenance requirements that screen out weaker products and support certified suppliers in public-sector buying. With more than 500,000 light-source models registered in EPREL, the Europe LED lighting industry remains deep and active, but quality verification has become easier for surveillance authorities and more visible for buyers.

Wholesale and retail held 46.12% share in 2025, which shows that distributor networks still anchor a large part of Europe LED lighting market activity. Electrical wholesalers remain important because they connect manufacturers with contractors, installers, and maintenance teams that still prefer local inventory support and technical guidance. Direct sales also remained important in the Europe LED lighting market, where large commercial, healthcare, airport, and municipal projects are specified by facility managers, consultants, or architects instead of off-the-shelf buyers. Those routes stay resilient because complex projects need design support, commissioning input, and after-sales accountability that broad online channels do not always provide. Even so, purchasing behavior is becoming more transparent and more standardized as product data has become easier to compare across brands.

E-commerce is forecasted to expand at a 5.45% CAGR through 2031, making it the fastest-growing route to market in the Europe LED lighting market size mix by channel. EPREL's QR-based product information has helped this shift because buyers can verify performance and labeling data without relying only on distributor interpretation. The downside is that online comparison makes non-connected LED products easier to commoditize, which can compress pricing for suppliers that compete mainly on basic hardware. Connected luminaires still resist full disintermediation because configuration, controls integration, and commissioning software often require dealer-backed or manufacturer-led workflows. As Digital Product Passport rules move closer, the Europe LED lighting market is likely to sort itself more clearly between simple products that sell on transparent digital comparison and system-led products that still depend on specification and support.

List of Companies Covered in this Report:

- Signify N.V.

- Zumtobel Group AG

- Osram Licht AG (ams-Osram)

- Schreder SA

- Fagerhult Group

- Acuity Brands Lighting Inc.

- Havells Sylvania Europe Ltd.

- Legrand S.A.

- Eaton Corporation plc (Cooper Lighting)

- TRILUX GmbH and Co. KG

- Thorn Lighting Ltd.

- FW Thorpe Plc

- LEDVANCE GmbH

- Helvar Oy Ab

- iGuzzini illuminazione S.p.A.

- Glamox AS

- Cree Lighting Europe S.p.A.

- ITECH LED Lighting

- Hella GmbH and Co. KGaA

- Nichia Europe GmbH

- Siteco GmbH

- Disano Illuminazione S.p.A.

- Tridonic GmbH and Co KG

- Opple Lighting Europe B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent EU Energy-Efficiency Regulations

- 4.2.2 Rapid Phase-Out of Halogen and Fluorescent Lamps

- 4.2.3 Corporate Net-Zero Commitments Accelerating Retrofits

- 4.2.4 Falling LED Cost per Lumen

- 4.2.5 Smart-City Tenders Bundling IoT Sensors

- 4.2.6 On-Site Renewable and DC Micro-Grids Adoption

- 4.3 Market Restraints

- 4.3.1 Price-Sensitive Retrofit Payback Period in SMEs

- 4.3.2 Supply-Chain Volatility for Rare-Earth Phosphors

- 4.3.3 Complexity of EU Eco-design and WEEE Compliance

- 4.3.4 Shortage of Skilled Installers for Connected Lighting

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Distribution Channel

- 5.2.1 Direct Sales

- 5.2.2 Wholesale / Retail

- 5.2.3 E-Commerce

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Commercial Offices

- 5.4.2 Retail Stores

- 5.4.3 Hospitality

- 5.4.4 Industrial

- 5.4.5 Highway and Roadway

- 5.4.6 Architectural

- 5.4.7 Public Places

- 5.4.8 Hospitals

- 5.4.9 Horticulture Gardens

- 5.4.10 Residential

- 5.4.11 Automotive

- 5.4.12 Other Applications (Chemicals, Oil and Gas, Agriculture)

- 5.5 By End User

- 5.5.1 Indoor

- 5.5.2 Outdoor

- 5.5.3 Automotive

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Sweden

- 5.6.8 Poland

- 5.6.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Zumtobel Group AG

- 6.4.3 Osram Licht AG (ams-Osram)

- 6.4.4 Schreder SA

- 6.4.5 Fagerhult Group

- 6.4.6 Acuity Brands Lighting Inc.

- 6.4.7 Havells Sylvania Europe Ltd.

- 6.4.8 Legrand S.A.

- 6.4.9 Eaton Corporation plc (Cooper Lighting)

- 6.4.10 TRILUX GmbH and Co. KG

- 6.4.11 Thorn Lighting Ltd.

- 6.4.12 FW Thorpe Plc

- 6.4.13 LEDVANCE GmbH

- 6.4.14 Helvar Oy Ab

- 6.4.15 iGuzzini illuminazione S.p.A.

- 6.4.16 Glamox AS

- 6.4.17 Cree Lighting Europe S.p.A.

- 6.4.18 ITECH LED Lighting

- 6.4.19 Hella GmbH and Co. KGaA

- 6.4.20 Nichia Europe GmbH

- 6.4.21 Siteco GmbH

- 6.4.22 Disano Illuminazione S.p.A.

- 6.4.23 Tridonic GmbH and Co KG

- 6.4.24 Opple Lighting Europe B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment