PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073545

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073545

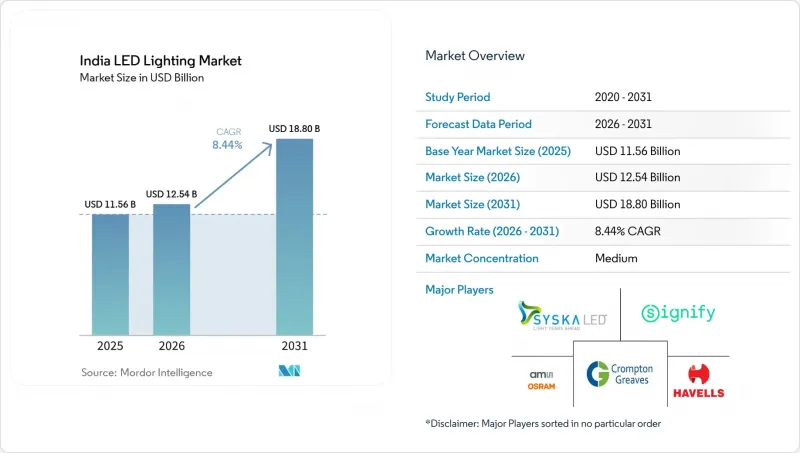

India LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india LED lighting market size in 2026 is estimated at USD 12.54 billion, growing from 2025 value of USD 11.56 billion with 2031 projections showing USD 18.8 billion, growing at 8.44% CAGR over 2026-2031.

This report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and E-Commerce), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, Hospitality, Industrial, and More), and End User (Indoor, Outdoor, and Automotive). The Market Forecasts are Provided in Terms of Value (USD).

India LED Lighting Market Trends and Insights

Surging Government Subsidy Programs for Street-Light Retrofits

Energy Efficiency Services Limited (EESL) had installed 12.7 million LED streetlights nationally by 2024, delivering municipal energy savings of 50-60% and setting a blueprint for subsequent procurement rounds. Bulk-tender models under the UJALA umbrella aggregate demand, negotiate steep supplier discounts, and incorporate performance-based service contracts that guarantee lumen output. State governments reinforce the model with dedicated budget outlays Odisha alone sanctioned INR 200 crore (USD 24 million) in 2024 creating a multiyear retrofit pipeline. Demonstration effects spur private townships and industrial parks to replicate street-lighting conversions, multiplying downstream demand. As Smart Cities Mission funds continue to prioritize adaptive roadway lighting in India, public-sector demand acts as a demand-certification mechanism, assuring suppliers of predictable order volumes.

Mandatory Energy-Efficiency Norms for New Commercial Real-Estate Projects

The Energy Conservation Building Code (ECBC) enforces lighting power-density ceilings that are practically unattainable without the use of LEDs, thereby embedding technology adoption in every major green-field commercial project. Andhra Pradesh operationalized state-specific ECBC rules in early 2025, providing a policy template that is now being replicated across multiple states. Mandatory compliance elevates LEDs from a discretionary specification to a statutory line item, thereby creating an enduring offtake channel irrespective of short-term price fluctuations. The code's alignment with LEED and IGBC green-building certifications further increases LED penetration among developers chasing premium lease rates and corporate tenants' sustainability commitments. Retrofits also benefit because landlords upgrading legacy properties to meet revised ECBC thresholds typically replace full lighting systems rather than selectively swap lamps.

High GST Slab Versus Conventional Lamps

Although LED bulbs fall under a 12% GST tier, their higher ex-factory price means the absolute tax burden remains sizable for low-income customers, diluting the headline fiscal incentive. The differential is sharper in off-grid villages where grid tariffs make lifetime savings nebulous and where retail markups inflate ticket prices. Micro-enterprises also face compliance headaches because GST filings demand digitized invoicing, a capability many informal traders lack. Combined, these factors can slow the replacement cycle in regions where subsidy programs are not fully implemented, postponing energy-efficiency gains and dampening volume growth in the Indian LED lighting market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Fall in LED Component Pricing and Domestic Manufacturing Scale-Up

- Growth of Organized Retail and E-Commerce Lighting Channels

- Fragmented After-Sales Service Network in Semi-Urban Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires and fixtures accounted for 61.25% of 2025 revenue, as large-format infrastructure upgrades and commercial interiors favored integrated solutions that offered superior optical control and ingress protection. Within the Indian LED lighting market, the size of this segment is driven by government highway projects and corporate campuses specifying IP66-rated roadway fixtures and modular office troffers, which elevates average selling prices. Manufacturers exploited the specification-heavy tender process to upsell smart drivers and aluminum housings, improving margin resilience even as chip ASPs dropped. Concurrently, the lamps segment recorded double-digit unit expansion, as 7.7 billion legacy incandescent and CFL sockets remained unaddressed, illustrating the dual-track adoption pattern that defines the Indian LED lighting market.

The lamps category's 10.32% CAGR outlook is based on household affordability and the continued rural push of Gram Ujala vouchers, which subsidize bulbs for families living below the poverty line. Economies of scale on SMD package lines are already compressing the prices of 9-watt bulbs, narrowing the payback window to under one year in grid-connected regions. Conversely, luminaire penetration in street and architectural lighting is expected to unlock higher gross profit pools, prompting suppliers to add in-house extrusion and powder-coating units. The coexistence of high-volume low-margin lamps and lower-volume high-margin fixtures requires supply-chain agility, encouraging multiproduct portfolios across most frontline brands.

Traditional wholesale channels still accounted for 53.15% of 2025 billings as electrical contractors value credit terms, on-site technical guidance, and bulk discounts that online portals rarely extend. Big-box retailers and institutional buyers also rely on wholesale master dealers to coordinate multi-vendor deliveries for turnkey projects that define the India LED lighting market. Yet the e-commerce slice is expanding at 8.88% CAGR, propelled by electronics marketplaces and manufacturer-hosted Shopify storefronts that appeal to urban DIY consumers and small builders seeking quick replenishment.

For many brands, direct-to-consumer logistics have streamlined distribution channels and revealed real-time demand signals, thereby accelerating SKU rationalization cycles. However, e-commerce returns and reverse-logistics costs dilute net margins, driving some players to hybridize by listing low-complexity SKUs online while routing professional-grade luminaires through authorized value-added resellers. Wholesale incumbents are answering back with app-based ordering, dynamic credit scoring, and omnichannel loyalty programs. As fintech-enabled working-capital solutions scale, smaller dealers will gain the liquidity needed to stock premium smart-lighting SKUs, preserving their relevance in the India LED lighting market.

Complete Report Scope:

- By Product Type

- Lamps

- Luminaires / Fixtures

- By Distribution Channel

- Direct Sales

- Wholesale Retail

- E-commerce

- By Installation Type

- New Installation

- Retrofit Installation

- By Application

- Commercial Offices

- Retail Stores

- Hospitality

- Industrial

- Highway and Roadway

- Architectural

- Public Places

- Hospitals

- Horticulture Gardens

- Residential

- Automotive

- Others (Chemicals, Oil and Gas, Agriculture)

- By End-User

- Indoor

- Outdoor

- Automotive

List of Companies Covered in this Report:

- Signify Innovations India Ltd.

- Havells India Ltd.

- Crompton Greaves Consumer Electricals Ltd.

- Bajaj Electricals Ltd.

- Syska LED Lights Pvt. Ltd.

- Wipro Lighting - Wipro Enterprises Pvt. Ltd.

- Surya Roshni Ltd.

- Orient Electric Ltd.

- Panasonic Life Solutions India Pvt. Ltd.

- Osram Lighting Pvt. Ltd. (LEDVANCE India)

- Eveready Industries India Ltd.

- NTL Lemnis India Pvt. Ltd.

- Goldmedal Electricals Pvt. Ltd.

- HPL Electric and Power Ltd.

- Fiem Industries Ltd.

- Polycab India Ltd. (Lighting division)

- IKEA India Pvt. Ltd. (Smart-home LEDs)

- Halonix Technologies Pvt. Ltd.

- Sturlite Electric Pvt. Ltd.

- Kwality Photonics Pvt. Ltd. (LED chips)

- MIC Electronics Ltd.

- Luker Electric Technologies Pvt. Ltd.

- Opple Lighting India Pvt. Ltd.

- RR Kabel Ltd. (Lighting division)

- Vihan Electric Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging government subsidy programmes for street-light retrofits

- 4.2.2 Mandatory energy-efficiency norms for new commercial real-estate projects

- 4.2.3 Rapid fall in LED component pricing and domestic manufacturing scale-up

- 4.2.4 Growth of organised retail and e-commerce lighting channels

- 4.2.5 IoT-enabled smart-lighting pilots in tier-1 Indian cities

- 4.2.6 Localization of horticulture LEDs for protected farming clusters

- 4.3 Market Restraints

- 4.3.1 High GST slab (18%) versus conventional lamps

- 4.3.2 Fragmented after-sales service network in semi-urban areas

- 4.3.3 Price-war margin squeeze among local assemblers

- 4.3.4 Delayed BIS certification timelines for innovative form-factors

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Distribution Channel

- 5.2.1 Direct Sales

- 5.2.2 Wholesale Retail

- 5.2.3 E-commerce

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Commercial Offices

- 5.4.2 Retail Stores

- 5.4.3 Hospitality

- 5.4.4 Industrial

- 5.4.5 Highway and Roadway

- 5.4.6 Architectural

- 5.4.7 Public Places

- 5.4.8 Hospitals

- 5.4.9 Horticulture Gardens

- 5.4.10 Residential

- 5.4.11 Automotive

- 5.4.12 Others (Chemicals, Oil and Gas, Agriculture)

- 5.5 By End-User

- 5.5.1 Indoor

- 5.5.2 Outdoor

- 5.5.3 Automotive

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Signify Innovations India Ltd.

- 6.4.2 Havells India Ltd.

- 6.4.3 Crompton Greaves Consumer Electricals Ltd.

- 6.4.4 Bajaj Electricals Ltd.

- 6.4.5 Syska LED Lights Pvt. Ltd.

- 6.4.6 Wipro Lighting - Wipro Enterprises Pvt. Ltd.

- 6.4.7 Surya Roshni Ltd.

- 6.4.8 Orient Electric Ltd.

- 6.4.9 Panasonic Life Solutions India Pvt. Ltd.

- 6.4.10 Osram Lighting Pvt. Ltd. (LEDVANCE India)

- 6.4.11 Eveready Industries India Ltd.

- 6.4.12 NTL Lemnis India Pvt. Ltd.

- 6.4.13 Goldmedal Electricals Pvt. Ltd.

- 6.4.14 HPL Electric and Power Ltd.

- 6.4.15 Fiem Industries Ltd.

- 6.4.16 Polycab India Ltd. (Lighting division)

- 6.4.17 IKEA India Pvt. Ltd. (Smart-home LEDs)

- 6.4.18 Halonix Technologies Pvt. Ltd.

- 6.4.19 Sturlite Electric Pvt. Ltd.

- 6.4.20 Kwality Photonics Pvt. Ltd. (LED chips)

- 6.4.21 MIC Electronics Ltd.

- 6.4.22 Luker Electric Technologies Pvt. Ltd.

- 6.4.23 Opple Lighting India Pvt. Ltd.

- 6.4.24 RR Kabel Ltd. (Lighting division)

- 6.4.25 Vihan Electric Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment