PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066756

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066756

Fine Art Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

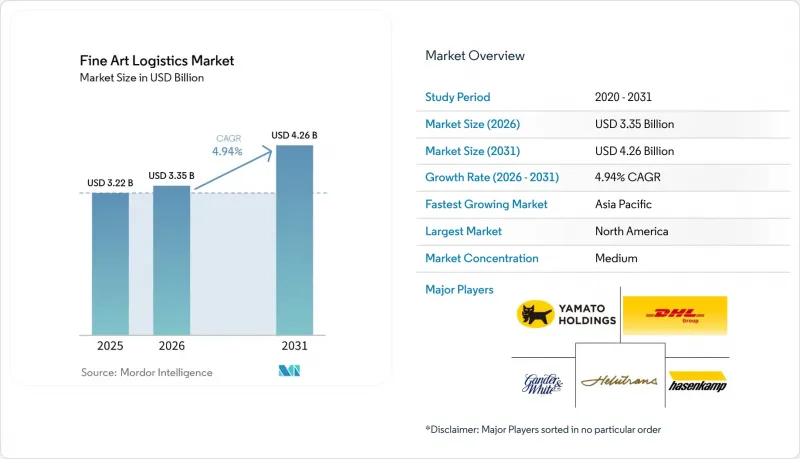

According to Mordor Intelligence, the fine art logistics market is expected to increase from USD 3.22 billion in 2025 to USD 3.35 billion in 2026 and reach USD 4.26 billion by 2031, growing at a CAGR of 4.94% over 2026-2031.

Structural change is underway as hybrid live-plus-digital auctions tighten shipment windows, while duty-free freeports in Singapore, Hong Kong, Geneva, and Dubai multiply inter-continental transfer points. This report is Segmented by Logistics Function (Transportation (Road, Air, Sea, and Rail), Warehousing & Distribution, and Value-Added Services), by End Users (Art, Dealers and Galleries, Auction Houses, Museums, Art Fairs, Private Collectors, and Others), and by Geography (North America, South America, Asia Pacific, Europe, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Fine Art Logistics Market Trends and Insights

Hybrid Live-Plus-Digital Auction Formats Intensify Just-In-Time Shipment Volumes

Auction houses now synchronize in-person previews with global online bidding. Artworks must reach preview venues ahead of streaming schedules, pass digital fingerprint checks, and depart for buyers within days, compressing the traditional three-week auction cycle into less than 10 days. Remote 3-D scanning lets bidders view high-resolution twins, yet the physical object still travels to meet pre-sale condition reporting standards. Broader bidder reach increases post-sale cross-border shipments, shifting fine art logistics market capacity toward agile, multi-modal routing. Compliance layers tied to passports, visas, and customs declarations add paperwork that specialist providers embed into turnkey auction logistics packages.

Higher Insurance Coverage Thresholds Push Stakeholders Toward Specialist Providers

Underwriters now insist on larger "nail-to-nail" limits after several high-profile loss events, driving stakeholders toward logistics firms with pre-vetted Lloyd's agreements. Enhanced due-diligence requires sanctions screening and anti-money-laundering reporting before pick-up. Premium providers offer bundled coverage that accelerates policy issuance, creating a tiered supply landscape where smaller carriers handle lower-value regional moves. The added paperwork favors firms that maintain 24-hour specialist claims desks and digital audit trails.

Volatile Jet-Fuel and Bunker Prices Inject Cost Unpredictability

Energy-price swings translate into surcharges that outpace annual logistics budgets, squeezing margins when contracts lock prices months ahead. Larger providers hedge fuel exposure through futures and pass-through clauses, widening the gap with smaller rivals. The volatility accelerates consolidation as acquisition candidates seek the balance-sheet muscle required to weather cost spikes.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Duty-Free Art Freeports in Europe and GCC Amplifies Inter-Continental Flows

- IoT-Enabled Climate-Monitoring Crates Create Pull for Smart-Logistics Vendors

- Geopolitical Sanctions Heighten Export-License and Compliance Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation captured 60.39% of fine art logistics market share in 2025. Air freight dominates high-value transfers thanks to stringent security and rapid transit times, while bio-marine-fuel sea lanes absorb cost-sensitive exhibition shipments. Road fleets, increasingly electric inside low-emission zones, handle final-mile moves, and rail corridors link European capitals on lower carbon footprints. Warehousing and distribution provide climate-controlled bridges that support multi-stop itineraries. Value-added services are projected to grow faster than the overall fine art logistics market size, reflecting client appetite for bundled regulatory, insurance, and authentication support. IoT sensors, blockchain ledgers, and bespoke risk consulting convert once-transactional shipping jobs into multi-year stewardship contracts.

Value-added services are expected to grow the fastest with 5.45% CAGR over the forecast period. Technology investment is reshaping price structures. Smart-box leasing, online booking portals, and API connectivity with auction catalogues compress manual touchpoints. Firms that can demonstrate real-time chain-of-custody data command premiums, while those limited to legacy vans and paper manifests compete on thin margins. The divergence reinforces a two-speed Fine art logistics market, where digitally enabled providers expand EBITDA and acquisition multiples, and undigitized carriers face revenue stagnation.

Geography Analysis

North America generated 42.14% of 2025 revenue, anchored by New York and Los Angeles auction ecosystems. Dense collector bases support year-round moves, while well-defined customs procedures and bonded warehouses lower regulatory friction. United States museums maintain strict conservation standards, driving premium demand for IoT-equipped crates and GPS-tracked vehicles.

Europe remains the historic crossroads of fine art trade, yet post-Brexit paperwork has lengthened UK-EU transfers, nudging some volume toward Luxembourg and Geneva freeports. Continental rail networks enable lower-carbon intra-EU routes, and strong insurer presence in London retains underwriting talent essential to the Fine art logistics market. EU regulations mandating carbon disclosure from 2027 will likely accelerate adoption of bio-fuel and electric fleets.

Asia-Pacific is the fastest-growing region, expanding at a 5.55% CAGR to 2031. Hong Kong and Singapore freeports underpin tax-efficient storage, while China's Tier-1 cities host a surging ultra-high-net-worth population. Government cultural investments in Seoul, Tokyo, and Sydney spur museum expansion, driving import flows of Western masterpieces and outbound touring shows of Asian modernists. Providers that combine Mandarin-speaking couriers with Western conservation credentials gain share.

- Yamato Transport Co., Ltd.

- Gander & White

- Sinotrans

- Helu-Trans

- Hasenkamp

- DSV A/S

- Masterpiece International

- U.S. Art

- DHL Group

- Andre Chenue

- LP Art

- Crozier Fine Arts

- Cadogan Tate

- Crown Fine Art

- Momart

- Dietl International

- Convelio

- Cargolux (CV Precious)

- Lotus Fine Arts Logistics

- Baltrans*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid Live-Plus-Digital Auction Formats Intensify Just-in-Time Shipment Volumes

- 4.2.2 Higher Insurance Coverage Thresholds Push Stakeholders Toward Specialist Providers

- 4.2.3 Expansion of Duty-Free Art Freeports in Europe and GCC Amplifies Inter-Continental Flows

- 4.2.4 IoT-Enabled Climate-Monitoring Crates Create Pull for Smart-Logistics Vendors

- 4.2.5 Demand for Bio-Marine-Fuel Shipping Lanes Spurs Sustainable Ocean Transport

- 4.2.6 Fractional-Ownership Platforms Require Rotating Custody and Micro-Fulfilment Models

- 4.3 Market Restraints

- 4.3.1 Volatile Jet-Fuel and Bunker Prices Inject Cost Unpredictability

- 4.3.2 Geopolitical Sanctions Heighten Export-License and Compliance Complexity

- 4.3.3 Shortage of Museum-Grade Sustainable Packing Substrates Slows Green Transition

- 4.3.4 Stricter Anti-Illicit-Antiquities Checks Prolong Provenance Documentation Cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Spotlight on Transport Rates

5 Market Size and Growth Forecasts (Value)

- 5.1 By Logistics Function

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea and Inland Waterways

- 5.1.1.4 Rail

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-added Services (Labelling, Kitting, Consulting)

- 5.1.1 Transportation

- 5.2 By End Users

- 5.2.1 Art Dealers and Galleries

- 5.2.2 Auction Houses

- 5.2.3 Museums

- 5.2.4 Art Fairs

- 5.2.5 Private Collectors

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Peru

- 5.3.2.3 Chile

- 5.3.2.4 Argentina

- 5.3.2.5 Rest of South America

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 Europe

- 5.3.4.1 United Kingdom

- 5.3.4.2 Germany

- 5.3.4.3 France

- 5.3.4.4 Spain

- 5.3.4.5 Italy

- 5.3.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.3.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.3.4.8 Rest of Europe

- 5.3.5 Middle East And Africa

- 5.3.5.1 United Arab of Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East And Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Yamato Transport Co., Ltd.

- 6.4.2 Gander & White

- 6.4.3 Sinotrans

- 6.4.4 Helu-Trans

- 6.4.5 Hasenkamp

- 6.4.6 DSV A/S

- 6.4.7 Masterpiece International

- 6.4.8 U.S. Art

- 6.4.9 DHL Group

- 6.4.10 Andre Chenue

- 6.4.11 LP Art

- 6.4.12 Crozier Fine Arts

- 6.4.13 Cadogan Tate

- 6.4.14 Crown Fine Art

- 6.4.15 Momart

- 6.4.16 Dietl International

- 6.4.17 Convelio

- 6.4.18 Cargolux (CV Precious)

- 6.4.19 Lotus Fine Arts Logistics

- 6.4.20 Baltrans*

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Sustainability and Carbon-Neutral Logistics

- 7.3 Digital Tracking and Provenance Solutions