PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072453

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072453

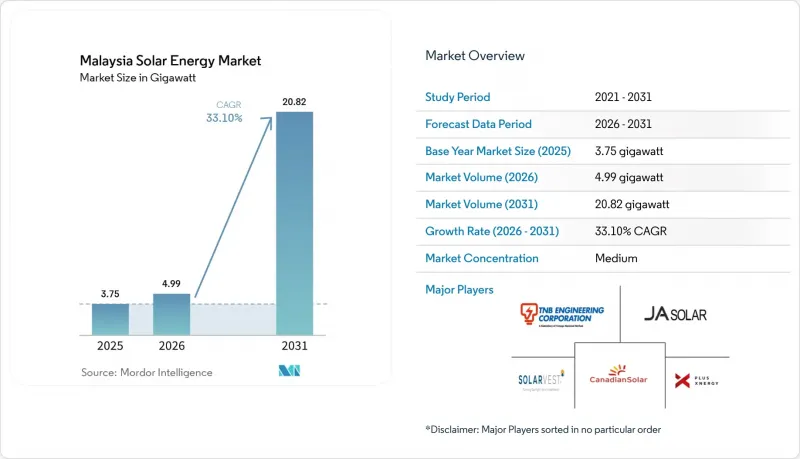

Malaysia Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the malaysia solar energy market size is expected to grow from 3.75 gigawatt in 2025 to 4.99 gigawatt in 2026 and is forecast to reach 20.82 gigawatt by 2031 at 33.1% CAGR over 2026-2031.

This report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Malaysia Solar Energy Market Trends and Insights

Government LSS Auction Expansions Drive Market Acceleration

Malaysia continues to enlarge the LSS program, providing transparent capacity pipelines and price discovery that underpin project bankability. LSS5 was awarded 2 GW in 2024 at an average tariff of RM0.1699 per kWh. LSS PETRA 5 + aims for another 2 GW in 2025, maintaining competitive pressure on cost while standardizing storage requirements. Predictable scheduling enables developers to secure supply contracts early, mitigate logistics risk, and meet stringent grid-code milestones. The policy lowers regulatory uncertainty and signals long-term commitment that attracts both domestic and foreign direct investment into the Malaysia solar energy market.

Declining PV Module Costs Accelerate Project Economics

A global supply glut led to a nearly 20% decline in module prices in 2024, enabling sub-RM 0.20 per kWh levelized costs at Malaysian utility sites. Cheaper panels shorten payback periods for rooftop adopters, thereby broadening the Malaysian solar energy market's customer base. However, U.S. anti-dumping duties on Malaysian exports disrupt manufacturing utilization, creating procurement timing risk that developers must hedge through diversified sourcing strategies. Lower hardware outlays nevertheless outweigh the volatility, reinforcing the competitiveness of new projects.

Grid Congestion in Peninsular Grid Constrains Integration Capacity

Transmission capacity has not kept pace with the rapid expansion of solar energy. Tenaga Nasional Berhad has earmarked RM 10.3 billion until 2030 for grid modernization, yet the roll-out lags behind near-term connection requests. Peak PV output coincides with mid-day industrial lulls, aggravating reverse-flow constraints that prompt curtailment. Developers increasingly add storage or clusters near load centers to mitigate bottlenecks, but systemic relief hinges on timely transmission upgrades that sustain the growth of the Malaysian solar energy market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Corporate PPA and RE100 Demand Transforms Procurement Patterns

- Data Center Power Demand Spike Creates Industrial Anchor Load

- High Financing Cost for Rooftop SME Projects Limits Market Penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar PV held 100.00% of Malaysia's solar energy market share in 2025, underscoring its entrenched position as the only commercially deployed technology. Robust irradiation of 4.5-5.5 kWh/ m2 /m2/day permits capacity factors that keep levelized costs below grid parity. The Malaysia solar energy market size for PV is projected to climb at a 33.1% CAGR through 2031, reflecting proven performance, abundant local assembly, and streamlined permitting. No concentrated solar power (CSP) ventures entered planning because direct normal irradiance falls short of economic thresholds, and higher capital intensity dampens appetite.

Local module assembly by JinkoSolar and LONGi reduces shipping lead times and hedges currency fluctuation, improving cost certainty for developers. Bankability gains further traction from the Sejingkat 60 MW / 80 MWh battery project, which validates hybrid PV-storage for frequency regulation. Energy Commission grid codes mandate IEC compliance and advanced inverter functionality, elevating quality while ensuring PV assets integrate safely into the Malaysia solar energy market.

Complete Report Scope:

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

List of Companies Covered in this Report:

- First Solar Inc.

- Canadian Solar Inc.

- Plus Xnergy Holding Sdn Bhd

- TNB Engineering Corporation Sdn Bhd

- Solarvest Holdings Berhad

- JA Solar Technology Co. Ltd.

- SunPower Corporation

- Hasilwan (M) Sdn Bhd

- TS Solartech Sdn Bhd

- Ditrolic Energy

- Cypark Resources Berhad

- Samaiden Group Berhad

- Gading Kencana Sdn Bhd

- Engie Services Malaysia

- Huawei Technologies Malaysia Sdn Bhd

- JinkoSolar Holding Co Ltd.

- LONGi Green Energy Technology Co Ltd.

- Hanwha Q CELLS

- Sunview Group Berhad

- Risen Energy Co Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government LSS auction expansions

- 4.2.2 Declining PV module costs

- 4.2.3 Rising corporate-PPA/RE100 demand

- 4.2.4 Data-centre power demand spike (Johor & Selangor)

- 4.2.5 Virtual NEM policy roll-out

- 4.2.6 Reservoir-based floating-solar push

- 4.3 Market Restraints

- 4.3.1 Grid congestion in Peninsular grid

- 4.3.2 High financing cost for rooftop SME projects

- 4.3.3 Land-use conflicts with agriculture

- 4.3.4 Import-supply volatility for PV modules

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 First Solar Inc.

- 6.4.2 Canadian Solar Inc.

- 6.4.3 Plus Xnergy Holding Sdn Bhd

- 6.4.4 TNB Engineering Corporation Sdn Bhd

- 6.4.5 Solarvest Holdings Berhad

- 6.4.6 JA Solar Technology Co. Ltd.

- 6.4.7 SunPower Corporation

- 6.4.8 Hasilwan (M) Sdn Bhd

- 6.4.9 TS Solartech Sdn Bhd

- 6.4.10 Ditrolic Energy

- 6.4.11 Cypark Resources Berhad

- 6.4.12 Samaiden Group Berhad

- 6.4.13 Gading Kencana Sdn Bhd

- 6.4.14 Engie Services Malaysia

- 6.4.15 Huawei Technologies Malaysia Sdn Bhd

- 6.4.16 JinkoSolar Holding Co Ltd.

- 6.4.17 LONGi Green Energy Technology Co Ltd.

- 6.4.18 Hanwha Q CELLS

- 6.4.19 Sunview Group Berhad

- 6.4.20 Risen Energy Co Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment