PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073436

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073436

United States Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

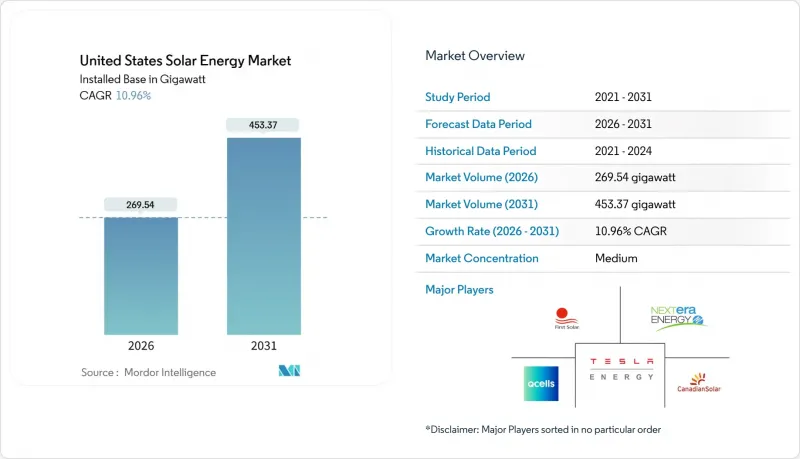

According to Mordor Intelligence, the united states solar energy market size in terms of installed base is expected to grow from 269.54 gigawatt in 2026 to 453.37 gigawatt by 2031, at a CAGR of 10.96% during the forecast period (2026-2031).

This report is Segmented by Technology (Solar Photovoltaic and Concentrated Solar Power), Grid Type (On-Grid and Off-Grid), and End-User (Utility-Scale, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

United States Solar Energy Market Trends and Insights

Inflation Reduction Act Tax Incentives Accelerating Utility-Scale PPAs

The uncapped 30% investment tax credit and USD 26 per MWh production tax credit extended through 2034 have ended boom-bust procurement cycles, enabling developers to underwrite projects in Ohio and Pennsylvania that once trailed the Southwest on economics. Stacking prevailing-wage and domestic-content adders can lift total tax benefits above 50% of project cost, a shift redirecting capital toward coal-retirement regions under EPA's Good Neighbor Plan. Corporate buyers contracted 16.6 GW of solar PPAs in 2024 and are comfortable with 15- to 20-year tenors because IRA certainty reduces revenue risk. The resulting pipeline diversification is broadening the United States solar energy market footprint beyond traditional sunbelt states. As a result, long-term capacity growth now aligns more closely with transmission-upgrade schedules than with federal policy sunsets.

Grid-Edge Storage Pairing Enhancing Project Bankability

Hybrid solar-plus-battery projects represented 63% of capacity in interconnection queues during 2024, driven by accelerated depreciation benefits and the ability to shift energy into evening hours when wholesale prices triple midday levels. California's NEM 3.0 regime lengthened standalone-solar payback periods, but adding a 10 kWh battery restores homeowner ROI and stabilizes grid demand during high-priced twilight peaks. Utility developers in Texas routinely attach 4-hour lithium-ion systems to capture ERCOT scarcity pricing, which surged to USD 5,000 per MWh during the August 2024 heatwave. Lenders now view storage-paired assets as lower risk, tightening debt spreads by up to 30 basis points. This credit advantage is accelerating market penetration of integrated systems across the United States solar energy market.

Interconnection Queue Bottlenecks Increasing Lead-Times Beyond 36 Months

More than 2,600 GW of generation and storage sat in U.S. queues by mid-2024, 95% of it solar, wind, or batteries-equal to 2.4 times existing grid capacity. Wait times average five years in MISO and PJM, lifting holding costs and eroding project IRRs by up to 12%. While Order 2023's cluster-study reforms will streamline new applications, 1,350 GW of legacy projects remain under old rules and are unlikely to clear before 2028. Developers increasingly pursue vertically integrated-utility states, such as Florida and the Carolinas, where queues are shorter and planning is coordinated. Nevertheless, prolonged delays continue to dampen the overall growth outlook for the United States solar energy market.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero Mandates Spurring C&I Power-Purchase Agreements

- Community-Solar Programs Expanding Access in High-Population States

- Section 201/301 Trade Actions Causing Module-Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar photovoltaics held 99.35% of the United States solar energy market in 2025, expanding at a 10.98% CAGR through 2031. First Solar's cadmium-telluride technology, though under 5% of capacity, grows swiftly because its lower carbon footprint and domestic-content status unlock maximum IRA adders. TOPCon cells boost module efficiencies to 23%, trimming balance-of-system costs and reinforcing crystalline silicon's lead. Bifacial modules now account for 60% of utility plants, delivering 10-20% extra yield on reflective sites, an attribute written into 60% of utility RFPs.

Concentrated solar power remains confined to legacy southwestern sites, rising only 2.1% CAGR, constrained by molten-salt storage costs three times higher than lithium-ion batteries. Perovskite-silicon tandems hit 33.9% lab efficiency in 2024 but face durability hurdles, implying commercial rollout post-2030. While crystalline silicon dominates, thin-film's rise tempers supply-chain risk, reinforcing resilience in the market. The United States solar energy market size tied to thin-film is projected to triple by 2031 as new fabs in Louisiana and Ohio come online.

Complete Report Scope:

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

List of Companies Covered in this Report:

- First Solar Inc.

- NextEra Energy Inc.

- SunPower Corporation

- Hanwha Q CELLS USA Corp.

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd.

- Tesla Energy

- Sunrun Inc.

- 8minute Solar Energy

- SOLV Energy LLC

- Mortenson Construction

- Rosendin Electric Inc.

- Renewable Energy Systems Americas

- Brookfield Renewable US

- EDF Renewables North America

- Enphase Energy Inc.

- Trina Solar Ltd.

- LONGi Solar

- REC Group (REC Solar Norway AS)

- Array Technologies Inc.

- Nextracker Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Inflation Reduction Act (IRA) Tax Incentives Accelerating Utility-Scale PPAs

- 4.2.2 Grid-Edge Storage Pairing Enhancing Project Bankability

- 4.2.3 Corporate Net-Zero Mandates Spurring C&I Power-Purchase Agreements

- 4.2.4 Community-Solar Programs Expanding Access in High-Population States

- 4.2.5 Domestic Manufacturing Credits Cutting Module Import Risk

- 4.2.6 Agrivoltaics Improving Land-Use Economics in the Midwest

- 4.3 Market Restraints

- 4.3.1 Interconnection Queue Bottlenecks Increasing Lead-Times Beyond 36 Months

- 4.3.2 Section 201/301 Trade Actions Causing Module-Price Volatility

- 4.3.3 Rising Transmission Congestion Curtailing Southwest Utility Projects

- 4.3.4 Skilled-Labor Shortage Inflating EPC Costs by >18 % YoY

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory & Policy Outlook (Federal + State)

- 4.6 Technological Outlook (TOPCon, HJT, Perovskites, Bifacial)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes (Wind, RNG, Long-Duration Storage)

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 By Grid Type

- 5.2.1 On-Grid

- 5.2.2 Off-Grid

- 5.3 By End-User

- 5.3.1 Utility-Scale

- 5.3.2 Commercial and Industrial (C&I)

- 5.3.3 Residential

- 5.4 By Component (Qualitative Analysis)

- 5.4.1 Solar Modules/Panels

- 5.4.2 Inverters (String, Central, Micro)

- 5.4.3 Mounting and Tracking Systems

- 5.4.4 Balance-of-System and Electricals

- 5.4.5 Energy Storage and Hybrid Integration

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 First Solar Inc.

- 6.4.2 NextEra Energy Inc.

- 6.4.3 SunPower Corporation

- 6.4.4 Hanwha Q CELLS USA Corp.

- 6.4.5 Canadian Solar Inc.

- 6.4.6 JinkoSolar Holding Co. Ltd.

- 6.4.7 Tesla Energy

- 6.4.8 Sunrun Inc.

- 6.4.9 8minute Solar Energy

- 6.4.10 SOLV Energy LLC

- 6.4.11 Mortenson Construction

- 6.4.12 Rosendin Electric Inc.

- 6.4.13 Renewable Energy Systems Americas

- 6.4.14 Brookfield Renewable US

- 6.4.15 EDF Renewables North America

- 6.4.16 Enphase Energy Inc.

- 6.4.17 Trina Solar Ltd.

- 6.4.18 LONGi Solar

- 6.4.19 REC Group (REC Solar Norway AS)

- 6.4.20 Array Technologies Inc.

- 6.4.21 Nextracker Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment