PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072479

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072479

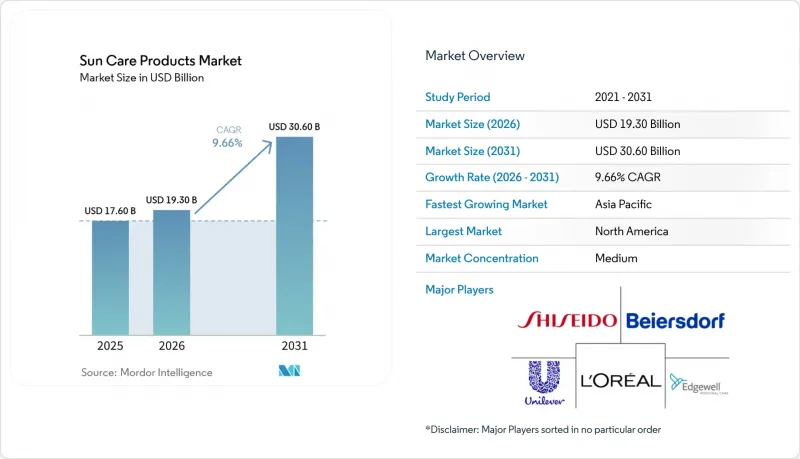

Sun Care Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the sun care products market size was valued at USD 17.60 billion in 2025 and estimated to grow from USD 19.30 billion in 2026 to reach USD 30.60 billion by 2031, at a CAGR of 9.66% during the forecast period (2026-2031).

This report is Segmented by Product Type (Self-Tanning Products, After-Sun Products, and Sun Protection Products), Category (Conventional and Natural/Organic), End-User (Adults and Kids/Children), Price Range (Mass and Premium), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Sun Care Products Market Trends and Insights

Rising Incidence of Skin Cancer and UV Awareness

Consumer awareness about skin cancers and the irreversible effects of UV rays on the skin is rising, driving demand for sun care products worldwide. According to Melanoma Foundation data from 2023, 186,680 melanoma cases were diagnosed in the United States. The shift toward prevention-focused healthcare spending amplifies the sun care market growth, particularly in aging populations where skin cancer prevention becomes economically advantageous compared to treatment costs. Regulatory bodies such as the FDA and European Medicines Agency are tightening efficacy standards, requiring in vivo testing for broad-spectrum claims and water-resistance labeling, which raises barriers to entry but also legitimizes premium pricing for compliant brands. This dynamic favors incumbents with established clinical pipelines and creates acquisition opportunities for smaller innovators holding novel UV filter patents.

Growing Popularity of Outdoor Recreational Activities

The past few years have seen an increase in participation in sports, especially in outdoor games. According to the Sports England data from 2024, 7,169,700 people in England participated in cycling . Additionally, recreational activities such as hiking, camping, and others are also growing among the young population. Due to this, the demand for sun protection products like sunscreens, moisturizers, and others is increasing across the world. According to the Outdoor Foundation data from 2024, the number of hiking participants in the United States was 63.43 million 2024 . Additionally, as a result of their light-colored skin and reduced melanin production (melanin absorbs sunlight before it damages the skin cell's DNA), Western consumers prefer to use sun care products when they are outside, especially on beaches. Those with light-colored skin are more likely to suffer damage from sunlight. Hence, the higher participation rate of Western individuals in outdoor recreational activities contributed to the rise in sales of sun care products.

Safety Concerns over Chemical Ingredients

Oxybenzone and octinoxate, two widely used chemical UV filters, have faced mounting scrutiny over potential endocrine disruption and coral reef toxicity. Hawaii enacted legislation in 2018 banning these ingredients effective January 2021, followed by similar measures in Palau and the U.S. Virgin Islands. The FDA's ongoing review of sunscreen active ingredients has placed 12 chemical filters in a "needs more data" category, leaving only zinc oxide and titanium dioxide with confirmed GRASE (Generally Recognized as Safe and Effective) status. This regulatory uncertainty has prompted reformulation efforts, with brands pivoting toward mineral-based alternatives or seeking approval for newer filters like bemotrizinol. Consumer advocacy groups amplify these concerns through social media campaigns, creating reputational risk for companies perceived as slow to adapt. The challenge is balancing safety perceptions with sensory performance, as mineral sunscreens often leave a white residue that discourages consistent use, potentially undermining public health goals.

Other drivers and restraints analyzed in the detailed report include:

- Preference for Natural and Organic Products

- Product Innovation and Diversification

- Stringent and Varying Sunscreen Regulations Across Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sun protection products captured 79.32% of market share in 2025, reflecting entrenched consumer habits around daily SPF application and beach-season stockpiling. This segment benefits from regulatory clarity: FDA and EU standards provide well-defined testing protocols for SPF and broad-spectrum claims, and from cross-category expansion, as moisturizers, foundations, and lip balms increasingly incorporate UV filters. However, after-sun products are growing at a 9.89% CAGR through 2031, driven by heightened awareness of post-exposure skin repair and the proliferation of aloe vera-infused gels and cooling lotions that address redness and peeling.

The shift toward multifunctional products is reshaping this segmentation. L'Oreal's La Roche-Posay line, for instance, combines SPF 50 with antioxidants and anti-aging peptides, blurring the boundary between sun protection and skincare treatment. This convergence appeals to consumers who prioritize efficiency and are willing to pay premium prices for products that deliver multiple benefits in a single application. Regulatory bodies have yet to issue comprehensive guidance on hybrid claims, creating a gray area that innovative brands exploit while awaiting formal standards.

Conventional formulations held a 70.03% share in 2025, anchored by mass-market brands that leverage economies of scale and established distribution networks. These products typically rely on chemical UV filters such as avobenzone and octocrylene, which offer lightweight textures and high SPF values at accessible price points. However, Organic/Natural products are expanding at a 10.47% CAGR through 2031, propelled by COSMOS certification uptake and consumer demand for clean-label ingredients. Brands such as Naos (Bioderma) and Clarins are investing in botanical extracts, green tea, chamomile, and vitamin E, which provide antioxidant benefits alongside UV protection, differentiating their offerings in crowded premium channels.

The challenge for organic players is overcoming sensory objections. Mineral-based sunscreens often leave a white cast and feel heavier on the skin, discouraging repeat use among consumers accustomed to invisible chemical formulas. Manufacturers are addressing this through micronization and tinting, creating products that blend seamlessly with diverse skin tones. Retailers are supporting the shift by dedicating shelf space to certified organic lines and training staff to educate shoppers on ingredient benefits, though price premiums, often 30-50% above conventional equivalents, remain a barrier for price-sensitive segments.

Complete Report Scope:

- Product Type

- Sun Protection Products

- After-sun Products

- Self-tanning Products

- Category

- Conventional

- Organic/Natural

- Price Range

- Mass

- Premium

- End-User

- Adults

- Kids/Children

- Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Others Distribution Channel

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Geography Analysis

North America held 33.12% of the market share in 2025, underpinned by mature consumer awareness, stringent FDA regulations, and a well-established retail infrastructure spanning supermarkets, specialty stores, and e-commerce platforms. The region's dominance reflects decades of public health campaigns by the CDC and American Academy of Dermatology, which have normalized daily SPF application and positioned sunscreen as a non-negotiable component of skincare routines. However, growth is moderating as penetration rates approach saturation, with incremental gains now tied to premiumization, consumers trading up to higher-SPF formulations, anti-aging hybrids, and dermatologist-endorsed brands. Canada and Mexico contribute to regional growth, with Mexico's beach tourism sector driving seasonal demand and Canada's focus on outdoor recreation supporting year-round sales.

Asia-Pacific is expanding at 11.21% CAGR through 2031, the fastest rate among all geographies, fuelled by rising disposable incomes, urbanization-linked pollution concerns, and aggressive digital marketing by multinational brands. China, India, Japan, South Korea, and Southeast Asian markets are experiencing a cultural shift toward preventive skincare, with UV protection increasingly viewed as essential for maintaining fair complexions and preventing premature aging. K-beauty trends, lightweight essences, cushion compacts with SPF, and multi-step routines are normalizing daily sunscreen use among younger demographics, while e-commerce platforms such as Tmall and JD.com provide direct access to international brands. Regulatory frameworks vary widely: Japan's Ministry of Health, Labour and Welfare classifies high-SPF sunscreens as quasi-drugs, requiring additional testing, while China's National Medical Products Administration mandates animal testing for imported cosmetics, complicating entry for cruelty-free brands. Local players such as Shiseido (Japan) and Kao Corporation (Japan) leverage deep distribution networks and cultural insights to compete with Western multinationals, often launching region-specific formulations that address humidity, pollution, and skin-tone preferences.

Europe captured a significant share in 2025, supported by the stringent EU Cosmetics Regulation (EC) No 1223/2009, which treats sunscreens as cosmetics and allows faster approval for new UV filters compared to the FDA's drug classification. This regulatory environment has enabled European brands such as Beiersdorf (Nivea), L'Oreal (La Roche-Posay), and Clarins to lead in formulation innovation, incorporating photostable filters like bemotrizinol and tinosorb that deliver broad-spectrum protection without the white cast associated with mineral sunscreens. Sustainability mandates are reshaping the competitive landscape: the EU's Single-Use Plastics Directive and Green Deal are pushing brands to adopt refillable packaging and biodegradable formulations, creating differentiation opportunities for eco-conscious players. Southern European markets, Spain, Italy, and Greece, drive seasonal demand tied to beach tourism, while Northern Europe exhibits year-round usage linked to outdoor sports and wellness trends. South America and the Middle East & Africa are smaller but growing, with Brazil's beach culture and the GCC's intense sun exposure creating pockets of high per-capita consumption.

- L'Oreal S.A.

- Beiersdorf AG

- Kenvue Inc.

- Edgewell Personal Care

- Shiseido Co. Ltd.

- Procter & Gamble Co.

- The Estee Lauder Companies Inc.

- Unilever PLC

- Clarins Group

- Supergoop!

- Colgate-Palmolive (EltaMD)

- Coty Inc.

- ISDIN SA

- Sun Bum LLC

- VLCC Healthcare Ltd.

- Lotus Herbals Pvt Ltd.

- Naos

- Kao Corporation

- Elixcell

- Thrive Natural Care

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Skin Cancer and UV Awareness

- 4.2.2 Growing Popularity of Outdoor Recreational Activities

- 4.2.3 Preference for Natural and Organic Products

- 4.2.4 Product Innovation and Diversification

- 4.2.5 Influence of Social Media and Celebrity Endorsements

- 4.2.6 Growing Adoption of Baby Personal Care Products

- 4.3 Market Restraints

- 4.3.1 Safety Concerns over Chemical Ingredients

- 4.3.2 Stringent and VaryingSsunscreen Regulations Across Regions

- 4.3.3 Availability of Counterfeit Products

- 4.3.4 Fluctuation Raw Material Prices

- 4.4 Consumer Demand Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Sun Protection Products

- 5.1.2 After-sun Products

- 5.1.3 Self-tanning Products

- 5.2 Category

- 5.2.1 Conventional

- 5.2.2 Organic/Natural

- 5.3 Price Range

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 End-User

- 5.4.1 Adults

- 5.4.2 Kids/Children

- 5.5 Distribution Channel

- 5.5.1 Supermarkets/Hypermarkets

- 5.5.2 Specialty Stores

- 5.5.3 Online Retail Stores

- 5.5.4 Others Distribution Channel

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 Italy

- 5.6.2.4 France

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Poland

- 5.6.2.8 Belgium

- 5.6.2.9 Sweden

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 Indonesia

- 5.6.3.6 South Korea

- 5.6.3.7 Thailand

- 5.6.3.8 Singapore

- 5.6.3.9 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Chile

- 5.6.4.5 Peru

- 5.6.4.6 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Nigeria

- 5.6.5.5 Egypt

- 5.6.5.6 Morocco

- 5.6.5.7 Turkey

- 5.6.5.8 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 L'Oreal S.A.

- 6.4.2 Beiersdorf AG

- 6.4.3 Kenvue Inc.

- 6.4.4 Edgewell Personal Care

- 6.4.5 Shiseido Co. Ltd.

- 6.4.6 Procter & Gamble Co.

- 6.4.7 The Estee Lauder Companies Inc.

- 6.4.8 Unilever PLC

- 6.4.9 Clarins Group

- 6.4.10 Supergoop!

- 6.4.11 Colgate-Palmolive (EltaMD)

- 6.4.12 Coty Inc.

- 6.4.13 ISDIN SA

- 6.4.14 Sun Bum LLC

- 6.4.15 VLCC Healthcare Ltd.

- 6.4.16 Lotus Herbals Pvt Ltd.

- 6.4.17 Naos

- 6.4.18 Kao Corporation

- 6.4.19 Elixcell

- 6.4.20 Thrive Natural Care

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK