PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072481

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072481

France Property and Casualty Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

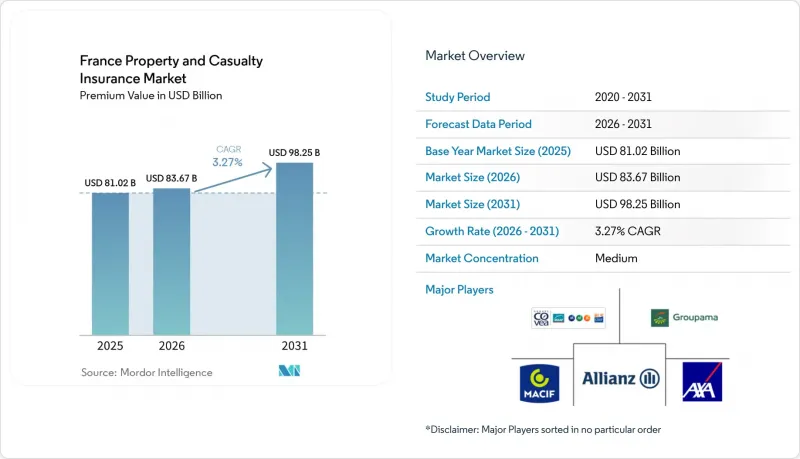

According to Mordor Intelligence, the france property and casualty insurance market size in terms of premium value is projected to expand from USD 81.02 billion in 2025 and USD 83.67 billion in 2026 to USD 98.25 billion by 2031, registering a CAGR of 3.27% between 2026 to 2031.

This report is Segmented by Line of Business (Property Insurance, Casualty Insurance), Distribution Channel (Direct, Brokers, Bancassurance, Affinity Partnerships & Embedded Platforms), End-User (Personal, Commercial), and Geography (France). The Market Forecasts are Provided in Terms of Value (USD).

France Property and Casualty Insurance Market Trends and Insights

Rising frequency & severity of climate-related catastrophes

France experienced EUR 10.6 billion (USD 11 billion) in insured losses in 2022 and EUR 6.5 billion (USD 6.7 billion) in 2023, establishing a new baseline for annual exposure. Subsidence from drought-induced soil shrinkage alone is expected to trigger EUR 43 billion in claims during 2020-2050, shifting the loss pattern from episodic flooding to chronic structural damage. The 2025 CatNat surcharge hike from 12% to 20% embeds premium inflation that lifts the France Property and Casualty Insurance market, even as volumes stabilize. ACPR's 2024 climate stress test demonstrates regulatory focus on capital adequacy under adverse weather scenarios. Insurers are therefore revising catastrophe models, increasing reinsurance cessions, and investing in satellite-based risk monitoring to refine underwriting granularity.

Persistent hard-market rate increases in commercial lines

Commercial segments have posted annual rate rises of 5-8% since 2023 as carriers recapture profitability after years of underpricing. Capacity withdrawal by global reinsurers tightens supply, reinforcing discipline across fire, cyber, and professional indemnity covers. Combined ratios have improved, with Groupama reporting 96.8% in 2024 versus triple-digit levels two years earlier. Larger accounts face higher retentions, fueling demand for parametric top-up products that pay out on predefined triggers. While rising prices buoy the France Property and Casualty Insurance market, they also entice digital insurers that promise leaner cost structures and selective underwriting on standard risks.

Intensifying motor-insurance price competition

Average motor premiums rose just 5% to EUR 545 (USD 567.6) in 2025, lagging claims inflation as digital comparison platforms push commoditization. Entrants like Lovys promote policies from EUR 3.99 (USD 4.15) a month, leveraging cloud-native operations to cut distribution costs. Regulatory constraints on risk-based pricing inhibit granular differentiation, while repair-cost inflation squeezes underwriting margins. Carriers respond by cross-selling ancillary covers and loyalty perks, yet profitability remains fragile. Smaller mutuals with mono-line motor portfolios face the greatest strain, prompting mergers or niche refocusing.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory insurance expansion into new risk classes

- Digitalization & usage-based motor insurance adoption

- Legacy low-interest-rate drag on investment returns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, property covers generated 72.35% of total premiums, underscoring their foundational role in the France Property and Casualty Insurance market. Rate hikes linked to the CatNat surcharge and higher construction-cost indices underpin revenue momentum, even as insured values plateau. Casualty lines, representing a smaller base, deliver the fastest growth at a 3.95% CAGR, propelled by cyber liability and widened professional indemnity mandates. Residential property remains buoyant due to compulsory mortgage insurance and subsidized catastrophe protection schemes. Commercial property adds breadth through supply-chain-triggered parametric clauses that pay within 72 hours of a qualifying event.

Cyber liability is the standout casualty sub-line, doubling premium volume between 2023 and 2025, yet still only 3% of commercial property and casualty totals, leaving significant headroom. Professional liability reforms in 2025 add immediate uplift, while workers' compensation sees incremental growth tied to payroll expansion. Agricultural parametric covers, distributed via farm-equipment dealers, speed payouts for drought and frost, enhancing rural resilience. Together, these dynamics reinforce the France Property and Casualty Insurance market's balanced growth profile and hedge cyclical exposure to single-line shocks.

Complete Report Scope:

- By Line of Business

- Property Insurance

- Residential Property Insurance

- Motor Insurance

- Commercial Property Insurance

- Agricultural Property Insurance

- Casualty Insurance

- General Liability

- Professional Liability

- Workers' Compensation

- Cyber Liability

- Property Insurance

- By Distribution Channel

- Direct (Online & Agency)

- Brokers

- Bancassurance

- Affinity Partnerships & Embedded Platforms

- By End-User

- Personal

- Commercial

List of Companies Covered in this Report:

- AXA France

- Covea (MAAF, MMA, GMF)

- Groupama

- Macif

- Allianz France

- Generali France

- Pacifica (Credit Agricole Assurances)

- MAIF

- MAAF

- MMA

- Abeille Assurances

- La Banque Postale Assurances IARD

- Direct Assurance

- Sogessur

- Swiss Re France

- HDI Global SE France

- Chubb France

- Tokio Marine Kiln France

- Zurich France

- Wakam

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents - France Property and Casualty Insurance Market

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Rising frequency & severity of climate-related catastrophes

- 5.2.2 Persistent hard-market rate increases in commercial lines

- 5.2.3 Mandatory insurance expansion into new risk classes

- 5.2.4 Digitalisation & usage-based motor insurance adoption

- 5.2.5 Parametric micro-insurance growth for SMEs & agriculture

- 5.2.6 Embedded insurance via e-commerce ecosystems

- 5.3 Market Restraints

- 5.3.1 Intensifying motor-insurance price competition

- 5.3.2 Legacy low-interest-rate drag on investment returns

- 5.3.3 Rising consumer litigation & claims disputes

- 5.3.4 Talent shortage in actuarial & cyber-risk underwriting

- 5.4 Value / Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces Analysis

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Buyers

- 5.7.3 Bargaining Power of Suppliers

- 5.7.4 Threat of Substitutes

- 5.7.5 Industry Rivalry

- 5.8 Pricing Analysis

6 Market Size & Growth Forecasts

- 6.1 By Line of Business

- 6.1.1 Property Insurance

- 6.1.1.1 Residential Property Insurance

- 6.1.1.2 Motor Insurance

- 6.1.1.3 Commercial Property Insurance

- 6.1.1.4 Agricultural Property Insurance

- 6.1.2 Casualty Insurance

- 6.1.2.1 General Liability

- 6.1.2.2 Professional Liability

- 6.1.2.3 Workers' Compensation

- 6.1.2.4 Cyber Liability

- 6.1.1 Property Insurance

- 6.2 By Distribution Channel

- 6.2.1 Direct (Online & Agency)

- 6.2.2 Brokers

- 6.2.3 Bancassurance

- 6.2.4 Affinity Partnerships & Embedded Platforms

- 6.3 By End-User

- 6.3.1 Personal

- 6.3.2 Commercial

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves & Deal Flow

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 AXA France

- 7.4.2 Covea (MAAF, MMA, GMF)

- 7.4.3 Groupama

- 7.4.4 Macif

- 7.4.5 Allianz France

- 7.4.6 Generali France

- 7.4.7 Pacifica (Credit Agricole Assurances)

- 7.4.8 MAIF

- 7.4.9 MAAF

- 7.4.10 MMA

- 7.4.11 Abeille Assurances

- 7.4.12 La Banque Postale Assurances IARD

- 7.4.13 Direct Assurance

- 7.4.14 Sogessur

- 7.4.15 Swiss Re France

- 7.4.16 HDI Global SE France

- 7.4.17 Chubb France

- 7.4.18 Tokio Marine Kiln France

- 7.4.19 Zurich France

- 7.4.20 Wakam

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment